GitLab (GTLB) has been on a mission to prove it's more than just a code repository. And its latest moves suggest it's serious about becoming the backbone of enterprise artificial intelligence-powered software development. The company recently announced a deeper integration with Amazon (AMZN) Web Services (AWS), and it's paired with a wave of product launches that expand what its platform can do.

GTLB stock is down roughly 44% year-to-date (YTD) heading into spring 2026. But the bigger question is whether these partnership moves change the longer-term story.

GitLab's AWS Deal Removes Friction for Big Customers

Enterprise software deals often stall not because of price but because of processes such as new-vendor reviews, separate billing, and security approvals. That's the problem GitLab's new AWS integration is designed to solve, according to a company statement.

Customers can now run GitLab's Duo Agent Platform, an artificial intelligence-powered DevSecOps engine, directly through Amazon Bedrock. These customers use approved AI models and AWS Identity and Access Management (IAM) controls already in place. It removes friction and accelerates the deal closure process for companies that have standardized on AWS.

GitLab also extended its Bring Your Own Model support, allowing self-managed customers to route AI inference through their own AWS environment. Source code and AI traffic remain within the customer's network, a feature that matters enormously to regulated industries such as finance and healthcare.

Another deal with Alphabet's (GOOG) (GOOGL) Google Cloud follows the same logic. Customers using Vertex AI can now power Duo Agent Platform with Google's Gemini models, with usage counting toward existing Google Cloud contracts. Basically, GitLab wants to sit inside enterprise cloud stacks and not compete with them.

Financial Picture Is Getting Stronger

In fiscal 2026, GitLab reported revenue of $955 million, an increase of 26% year-over-year (YoY). Its free cash flow rose 83% to $220 million, indicating a margin of almost 25%.

- Customers spending more than $1 million annually grew 26% YoY.

- GitLab's premium tier, called Ultimate, now accounts for 56% of annual recurring revenue.

- Notably, Ultimate customers are its most engaged and highest-value accounts.

- The company also launched its first-ever $400 million share repurchase program, signaling management's confidence in the business and helping mitigate share dilution.

That said, bookings growth has not kept pace with revenue growth over the past three years. Most of GitLab's revenue is recognized over time, so current numbers reflect deals signed two or three years ago.

GitLab's version 18.11 release introduced several new AI-powered features. The most meaningful for enterprise buyers is probably the Agentic Static Application Security Testing (SAST) Vulnerability Resolution tool, which reached general availability.

GitLab's own research found that developers spend about 11 hours per month fixing security vulnerabilities after code ships to production. The new agent analyzes confirmed issues, writes a fix, and opens a ready-to-review merge request without the developer having to switch tools or manually dig through findings.

Two additional agents were launched in 2026: a CI Expert Agent that builds pipeline configurations from scratch using plain-language instructions and a Data Analyst Agent that answers questions about code review cycles, deployment frequency, and pipeline health in natural language.

GitLab also introduced spending caps for its AI credits system, giving enterprise administrators control over monthly AI costs across their organizations. It addresses one of the most common objections enterprises raise before scaling AI usage: unpredictable spend.

Should You Buy GTLB Stock Right Now?

The AWS and Google Cloud integrations, combined with the new AI agent capabilities, give GitLab a credible path to expanding inside accounts that already trust it.

CI/CD pipeline usage is up 35% to 45% YoY. Security projects inside Ultimate grew 60% YoY. Customers are doing more inside the platform, even if GitLab hasn't yet figured out how to fully monetize that activity.

Valued at a market cap of $3.5 billion, GTLB stock is forecast to expand free cash flow from $220 million in fiscal 2026 to $515 million in fiscal 2031. If GitLab stock is priced at 20x forward FCF, it could almost triple over the next four years.

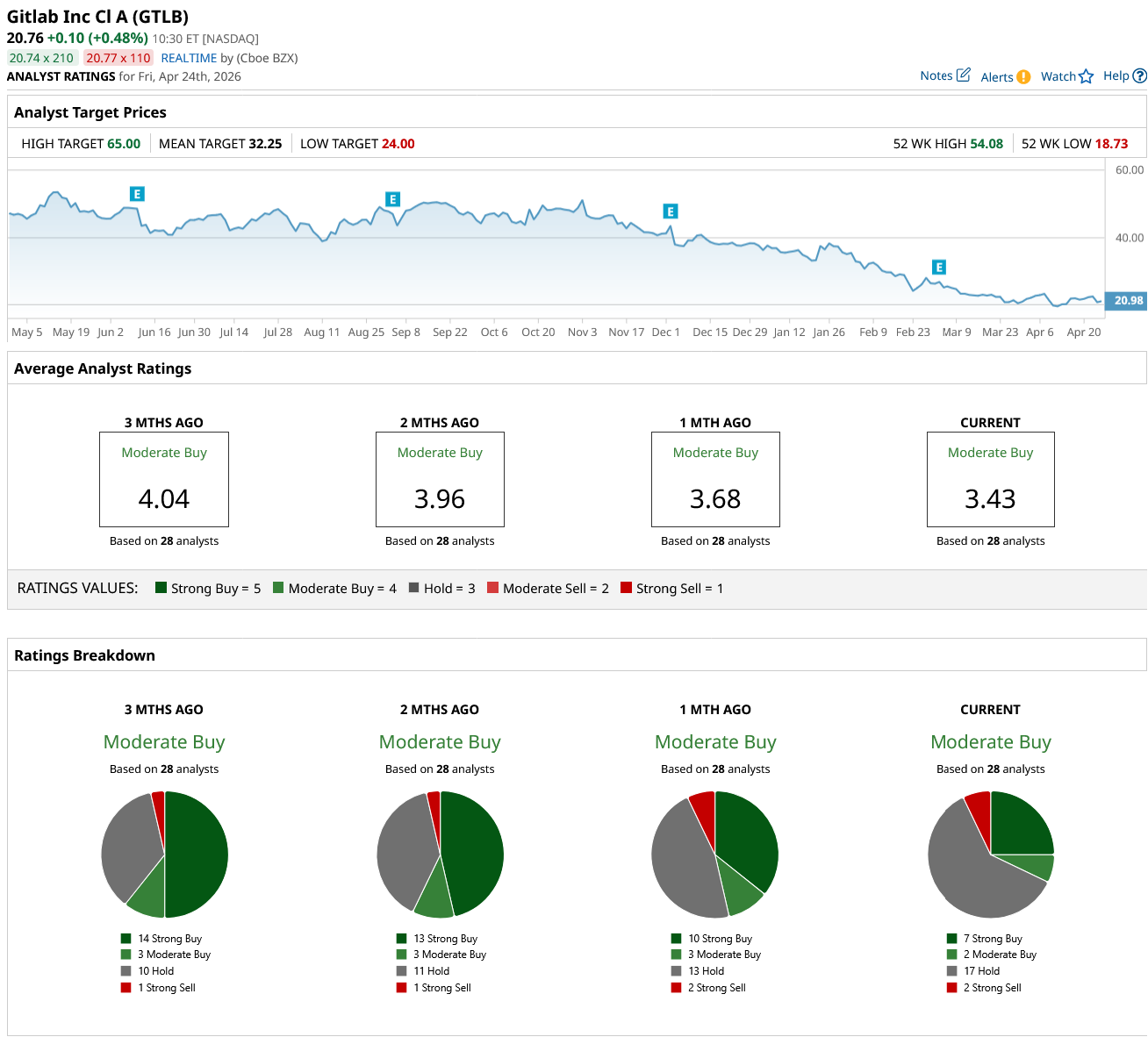

Out of the 28 analysts covering GTLB stock, seven recommend “Strong Buy,” two recommend “Moderate Buy,” 17 recommend “Hold,” and two recommend “Strong Sell.” The average GitLab stock price target is $32.25, indicating 60% upside from current levels.

Alternatively, growth in bookings has been soft, and the company is investing heavily in AI. It estimates margins to compress about 400 basis points in fiscal year 2027. GitLab CEO Bill Staples framed it plainly at the Morgan Stanley conference: AI coding tools are generating more code, and that code still has to be reviewed, secured, and deployed.

For long-term investors comfortable with a growth name still finding its monetization footing, GTLB looks compelling, with the AWS deal as the clearest sign yet that enterprise adoption is accelerating.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Zoetis%20sign%20at%20their%20Canadian%20By%20JHVEPhoto.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Space/Rocket%20takes%20off%20by%20Alones%20via%20Shutterstock.jpg)