GitLab (GTLB), an all-remote pioneer, is the leading platform for intelligent software orchestration. Originally a source code management tool, GitLab has evolved into a comprehensive DevSecOps powerhouse that integrates planning, security, and deployment into a single application. Under CEO Bill Staples, the company is spearheading agentic AI with its GitLab Duo Agent Platform, which automates complex engineering tasks with built-in governance.

Headquartered in San Francisco, California, GitLab started as an open-source project in 2011 and was later incorporated in 2014.

GitLab’s Rough Patch

GTLB stock has faced a challenging period, currently trading near its 52-week low after a 49% decline over the past year. This "falling star" status reflects investor anxiety regarding potential AI disruption to traditional developer tool seats and a cautious 2027 fiscal outlook.

In comparison to the Nasdaq Composite ($NASX), GitLab has significantly underperformed, trailing the tech-heavy benchmark during the last 12 months. While the broader Nasdaq has been buoyed by massive gains in semiconductor and large-cap AI infrastructure names, GitLab has struggled with "beta" compression as the SaaS sector faces valuation reratings.

GitLab Posts Strong Results

GitLab concluded fiscal 2026 with a powerful fourth quarter, reporting revenue of $260.4 million, a 23% year-over-year (YOY) increase. The company achieved non-GAAP diluted EPS of $0.30, smashing the $0.23 consensus estimate. This performance was driven by a 26% surge in customers with annual recurring revenue (ARR) of more than $1 million, highlighting GitLab's success in moving upmarket into the enterprise sector.

For the full fiscal year, GitLab generated $955.2 million in total revenue and crossed the landmark $1 billion ARR threshold. The firm also delivered $220 million in adjusted free cash flow, representing an 83% annual increase and a major leap in operational efficiency.

GitLab provided a conservative outlook for Q1 fiscal 2027, guiding revenue between $253 million and $255 million. While the company anticipates a slight dip in operating margins in the coming year as it ramps up go-to-market investments, management is focused on reaccelerating "first orders" to fuel long-term expansion. The general availability of the GitLab Duo Agent Platform and the introduction of GitLab Credits for AI usage are expected to be key growth drivers. With a 118% dollar-based net retention rate and total remaining performance obligations (RPO) of $1.1 billion, GitLab enters fiscal 2027 with a massive, high-quality backlog and a clear path toward becoming the enforcement layer for AI-driven software development.

GitLab Extends Google Partnership

GTLB stock has surged 7% following the announcement of an expanded strategic partnership with Alphabet's (GOOGL) Google Cloud. This deeper collaboration allows Google Cloud customers to integrate the GitLab Duo Agent Platform directly with Google’s powerful Vertex AI models. Critically, the usage of these AI tools will count toward customers' existing Google Cloud spending commitments, lowering the barrier for enterprise adoption.

According to GitLab Chief Product and Marketing Officer Manav Khurana, the value of AI agents depends entirely on the context and governance surrounding them. By linking GitLab’s deep repository of code, security findings, and pipelines with Vertex AI, the partnership provides the essential control layer needed for AI to manage more of the software lifecycle.

As developers increasingly rely on autonomous agents, GitLab is positioning itself as the "critical layer" that ensures these tools operate with the necessary context and security. This move not only strengthens GitLab’s AI capabilities but also solidifies its role within the massive Google Cloud ecosystem.

Should You Buy GTLB Stock?

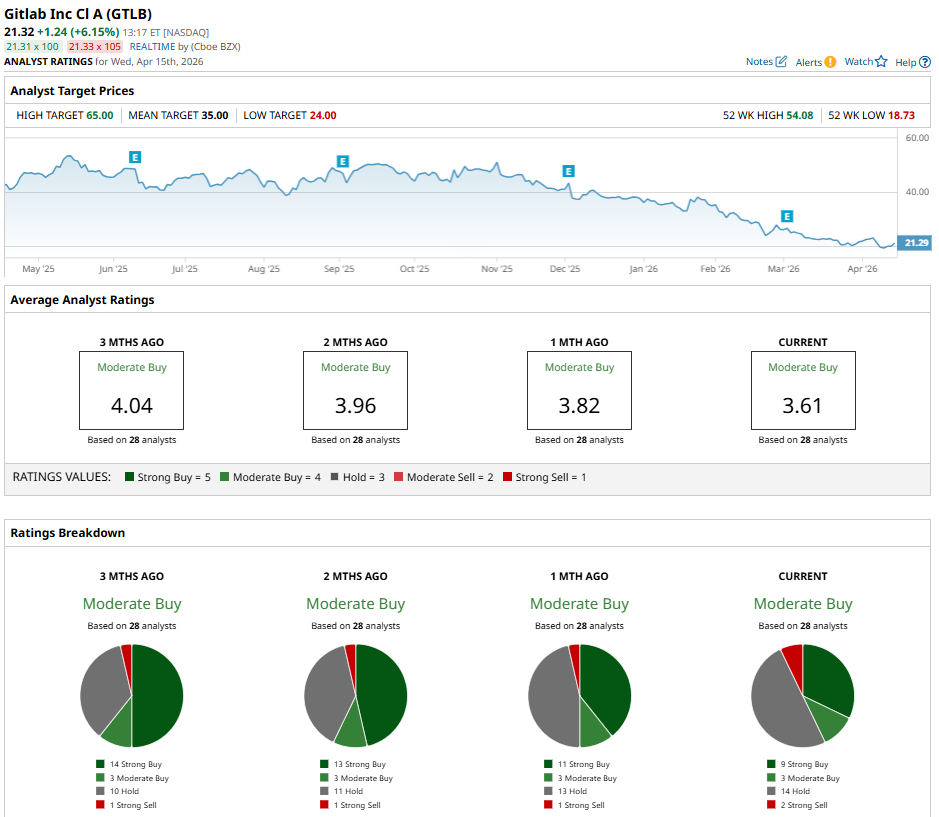

The recent expansion of the Google Cloud partnership serves as major validation for GitLab, directly addressing fears of AI disintermediation. Despite the technical downturn, GTLB stock holds a consensus "Moderate Buy" rating with a mean price target of $35, representing staggering potential upside of 72% from current price levels.

Out of 28 analysts with coverage, eight have a "Strong Buy" rating and three have a “Moderate Buy,” while 15 analysts have a “Hold” rating and just one has a “Strong Sell.” The consensus of these views suggests that, for long-term investors, GitLab’s rock-bottom valuation and high-margin DevSecOps dominance offer a rare, high-reward entry point.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)