/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

The race to build smarter technology is moving fast. This week, Anthropic said it will spend over $100 billion on Amazon (AMZN) Web Services (AWS) over the next ten years. Amazon, in turn, is putting $5 billion into Anthropic right away, with the option to add up to $20 billion more later.

All of this is happening as the biggest tech companies prepare to invest around $650 billion in AI‑related projects in 2026, with Amazon planning about $200 billion in spending, much of it aimed at AWS data centers and its own chips. AWS has already reached roughly $15 billion in yearly revenue from AI‑related services, giving an extra boost to its cloud business.

The key issue for investors is simple. Could this be the point where it still makes sense to buy Amazon stock before the full impact of these AI deals shows up in the numbers? Let's dive in.

Amazon’s Premium Price Tag

Amazon runs a huge global business built around online shopping, cloud services, digital ads and subscriptions, earning money from both regular shoppers and large companies.

Amazon is up 10.63% so far this year and 47.45% over the past 12 months.

This strong interest shows up in the valuation. The company is worth about $2.69 trillion with a trailing P/E of 34.05 times and a price‑to‑cash‑flow forward ratio of 16.15 times, compared with sector medians of 16.08 times and 10.13 times. That tells us investors are willing to pay a clear premium even though Amazon does not pay a dividend.

Their latest earnings give more context. The report for the quarter ending December 2025 showed earnings per share of $1.95, just under the $1.98 Wall Street was expecting, which works out to a small ‑1.52% miss.

This same quarter brought in $213.39 billion in sales, up 18.44% from the previous quarter, proving revenue is still growing at a strong double‑digit pace despite the company’s size. The period also delivered net income of $21.19 billion, with net income growth basically flat at 0.02%, suggesting profits are being held in check by heavy spending.

That picture improves when cash generation is in focus. AMZN reported operating cash flow of $139.51 billion for the quarter, a big 64.03% jump that shows how much cash the business can throw off even while it invests. Also, Amazon logged net cash flow of $7.79 billion, up 165.78% from the prior year’s quarter, meaning more of its earnings are turning into cash that can be reused for growth, debt, or buybacks.

Amazon’s Anthropic Deal and Expanding Moat

The clearest long‑term driver here is Anthropic. The startup has agreed to spend more than $100 billion on AWS over the next 10 years to train and run its Claude chatbot. In addition to Amazon investing $5 billion into Anthropic upfront, with $20 billion more to come later, it has already invested about $8 billion. That money effectively circles back into AWS, as Anthropic gets access to as much as five gigawatts of Amazon’s Trainium chips to power its models at scale.

And, cloud contracts are expanding. Amazon plans to buy Globalstar (GSAT) in an $11.6 billion deal to bulk up its low‑Earth‑orbit satellite network and offer direct‑to‑device connections that can rival services like Starlink. Once the deal closes, Amazon will own Globalstar’s satellites, ground infrastructure, and globally authorized spectrum.

That network is expected to support Amazon Leo. The plan is to add direct‑to‑device services, extend coverage beyond normal cell networks and start rolling out Amazon’s own D2D system in 2028, assuming the deal closes around 2027.

Back on the ground, Amazon is leaning further into robotics. It recently bought Fauna Robotics, shortly after the startup showed off Sprout, a 3.5‑foot humanoid robot with a rectangular head built for friendly interaction in homes and schools. This sits on top of a warehouse network that already uses more than one million robots in its warehouses and pushes Amazon deeper into consumer‑facing robots as it tests new ways to mix hardware and everyday life.

On the device side, Amazon is building a new smartphone, code‑named “Transformer.” The project sits inside a newer group called ZeroOne and is expected to ship with Amazon Shopping, Prime Video, and Prime Music already installed. A big focus will be Alexa, which has been rebuilt with more advanced features and relaunched as Alexa+ in February 2026. Amazon sees this phone as another way to attract more people into Amazon’s growing set of AI‑powered services.

Street Is Leaning Into Amazon’s AI Upside

Amazon’s next big checkpoint is just ahead. The company reports earnings after the close on April 29, and analysts are looking for $1.61 per share for the March quarter, up from $1.59 a year earlier.

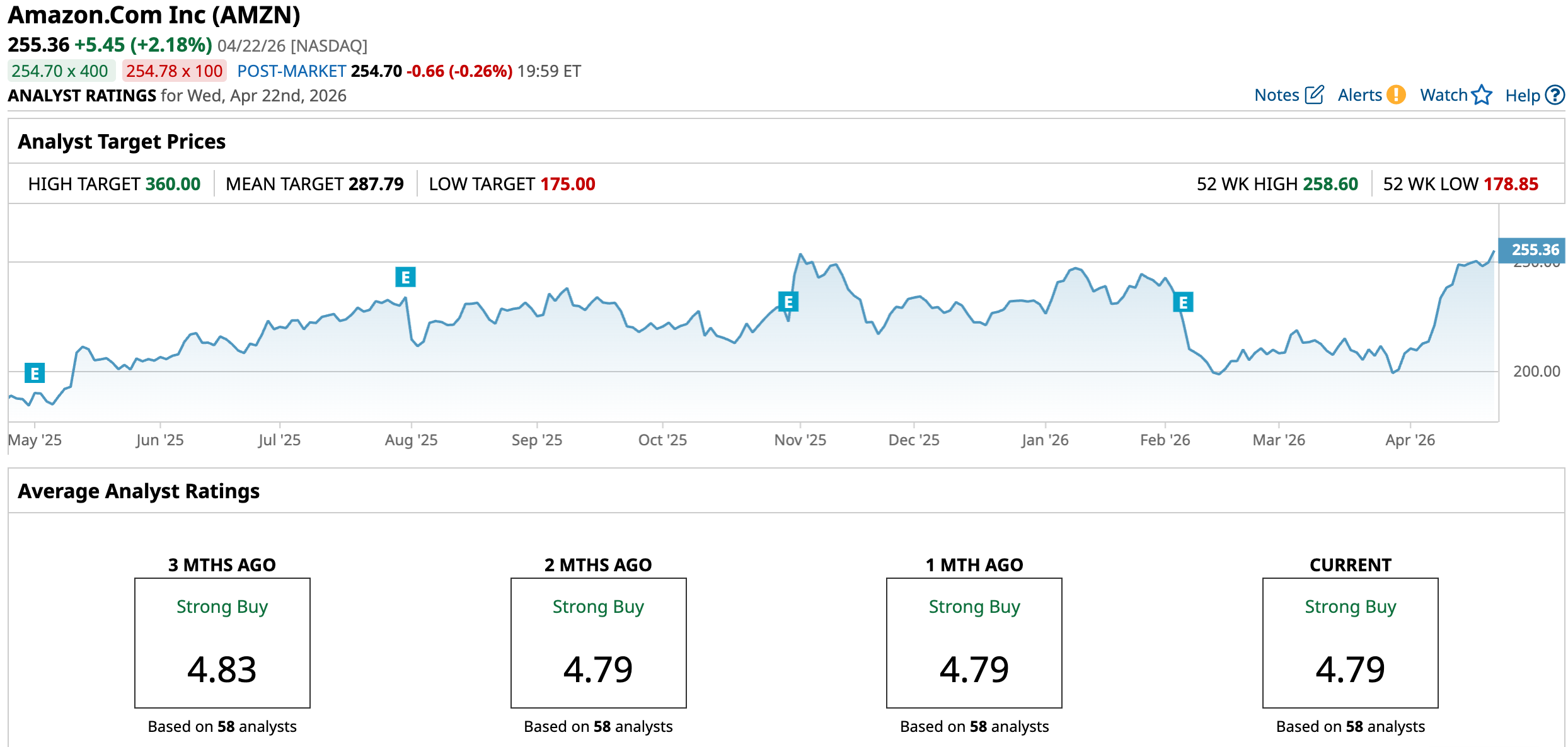

This outlook helps explain why bigger firms are still backing the stock. Wells Fargo recently inched its price target up from $304 to $305 and kept an “Overweight” rating, calling Amazon a “Top Internet Pick” for 2026. The firm is leaning on faster AWS revenue and a clear improvement in free cash flow as its main reasons.

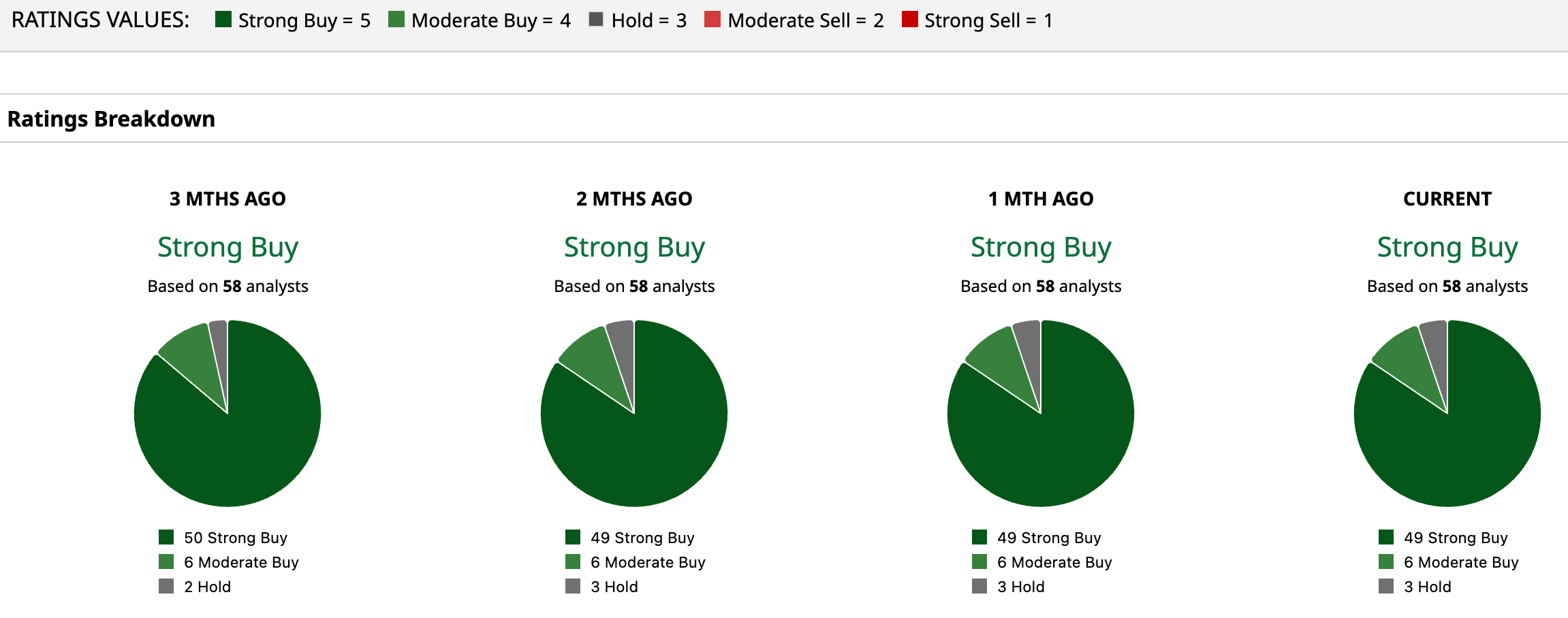

That bullishness is not isolated to one desk, as consensus from 58 covering analysts lands squarely in “Strong Buy” territory. The average 12‑month price target across this group stands at $287.79, roughly 12.7% upside from here. Even after a solid run, the Street still sees room for double‑digit gains if AWS keeps cashing in on AI demand and those stronger cash flows continue to build.

Conclusion

Right now, that $100 billion Anthropic deal, combined with improving AWS trends and a supportive analyst view, gives Amazon a solid case as a long‑term compounder rather than a trade to chase and drop. The outlook leans more toward steady gains than a sharp pullback, especially if AWS growth and free cash flow keep moving in the same direction. Taken together, those pieces make Amazon look more like a stock to hold through the cycle than one to flip on short‑term moves.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/The%20logo%20for%20ASML%20on%20a%20corporate%20office%20by%20Skorzewiak%20via%20Shutterstock.jpg)