/Advanced%20Micro%20Devices%20Inc_%20logo%20and%20chart%20data-by%20Poetra_%20RH%20via%20Shutterstock.jpg)

Advanced Micro Devices (AMD) is on its third rally in the past five years, but this one is more special — or at least that's what analysts are saying. Investors are seeing a slew of price target upgrades before the company's earnings day on May 5, and it's worth investigating what the rush is about.

AMD remains unremarkable compared to Nvidia (NVDA), which still dominates in the AI graphics processing unit (GPU) space. But that may not matter anymore, as analysts are flagging a central processing unit (CPU) supply shortage. That's where AMD looks a lot better.

GPUs aren't the only component that goes into a data center. AI GPU companies have surged significantly in the past few years as GPUs were the least plentiful and the most in demand, but the demand is now so strong that most other data-center components are beginning to see rising pricing power akin to that of GPUs.

Why Are Analysts Suddenly More Bullish?

Nvidia is untouchable when it comes to AI GPUs, but AMD is the leading company for CPUs. The company has a broad established CPU franchise in servers and PCs with EPYC and Ryzen, and CEO Lisa Su herself pointed out strong demand. On the fourth-quarter earnings call, Su said, "EPYC has become the processor of choice for the modern data center," and pointed to high demand for the next-generation Venice CPU.

The CPU business is not some side hustle anymore. It is one of the reasons analysts have been warming up ahead of earnings. On the last call, AMD said that server CPU orders had strengthened over the prior 60 days, and that server CPU revenue should grow even from Q4 into Q1, which is usually a seasonally weaker setup.

What Should Investors Expect on AMD's Earnings Day?

Most analysts expect to see CPU sales well above estimates. This has been the general trend across multiple other data-center components, where the mere rumor of a shortage tends to spark panic buying. Half of all U.S. data centers are already facing delays or cancellations due to tight supply.

AMD's Q1 revenue is expected to be $9.8 billion at the midpoint, but the guidance range goes up to $10.1 billion. For AMD stock to truly surge, I'd want to see something closer to $10.7 billion in sales.

Management tends to lowball estimates, and Q4 came in at revenue of $10.27 billion despite estimates for $9.67 billion. With that in mind, I wouldn't be surprised to see more than $11 billion in sales.

AMD said that Client, Gaming, and Embedded should all decline seasonally in Q1, with Gaming and Embedded following the normal post-holiday step-down. The fourth quarter included about $390 million of MI308 sales to China and a release of prior MI308 inventory reserves that lifted reported margin, while Q1 guidance includes only about $100 million of MI308 China sales and assumes no additional China revenue beyond that because the situation is "very dynamic."

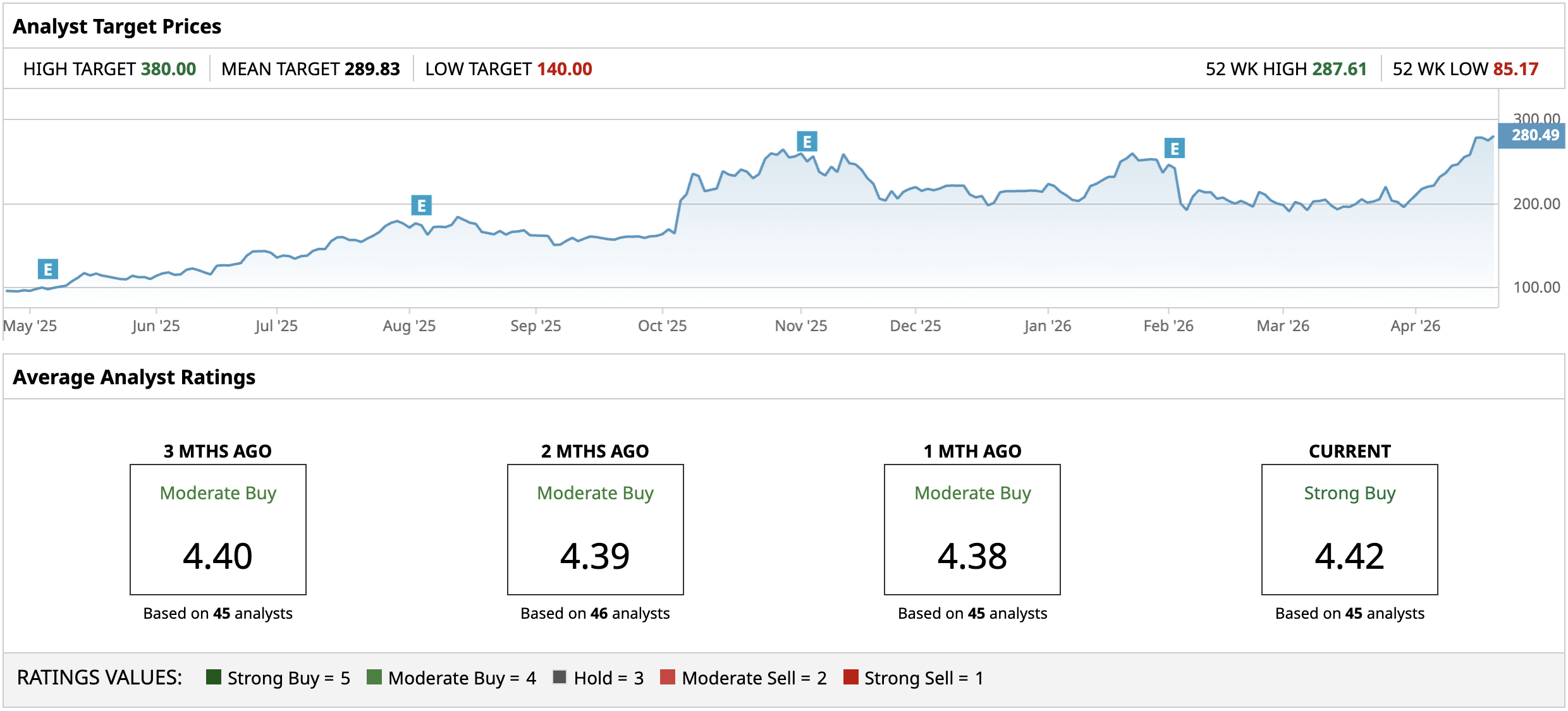

Analysts Are Hiking Price Targets

Analyst Jeff Pu at GF Securities recently kept a “Buy” rating on AMD stock and set a $311 price target. Pu argues that GPU and CPU demand are running ahead of supply, and his view is a classic semiconductor squeeze narrative. Pu pointed to positive signs of re-acceleration for Helios racks and tied that to demand that is outpacing supply. AMD holds about 41% value share in the server segment.

The $311 price target was recently outdone by Stifel analyst Ruben Roy, who boosted his price target from $280 to $320. Bernstein analyst Stacy Rasgon also boosted his target from $235 to $265.

These analysts are hiking their price targets not just because AMD's earnings are expected to be good. AMD stock itself has surged more than 50% in the past month, and analysts are trying to keep up.

AMD is trading at 47 times forward earnings for near-hypergrowth, which I believe is still fair value with more room to run.

On the date of publication, Omor Ibne Ehsan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)