/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)

Trillion-dollar tech giant Apple (AAPL) built its reputation by turning simple ideas into category-defining products – from the iPhone to the Mac – while creating an ecosystem people rarely leave. And, over time, Apple events became more than launches.

Every year, when Apple Worldwide Developers Conference rolls around, it’s not just developers who tune in. Wall Street watches just as closely. Apple’s events have a habit of dropping hints about what’s coming next – sometimes subtle, sometimes headline-grabbing – and investors have learned to read between those lines.

This time, the spotlight seems to be shifting toward Siri, Apple’s voice assistant. For years, Siri has been reliable, but some would say it's a bit behind the curve in the artificial intelligence (AI) race. Now, chatter around a “new Siri” is picking up, according to Bloomberg News reporter Mark Gurman, with expectations of a more conversational, chatbot-like experience, deeper personalization, and tighter integration across Apple’s ecosystem.

The idea is not just about answering questions anymore. It is about handling layered requests, understanding context on-screen, and possibly even working with external AI tools. If that plays out, this could mark one of Siri’s biggest leaps since its debut. Beyond the flash, Apple is expected to fine-tune performance, battery life, and usability, and these are small changes that tend to matter more over time.

And with AAPL stock not too far from its recent highs, does this Siri upgrade have enough bite to drive the stock higher, or is it just another neat feature without real market impact?

About Apple Stock

Apple, the Cupertino-based tech giant, has spent decades shaping the ways in which people live, work, and stay connected. From the iPhone that transformed communication to the Mac and iPad that made computing more personal, Apple built its name on simple yet powerful products.

Today, the story goes beyond devices. Its services segment has quietly become a strong growth engine, supported by over a billion paid subscriptions. Platforms like iCloud, Apple Music, and the App Store bring in steady, high-margin revenue, helping the company stay resilient even in uncertain times while keeping users deeply tied to its ecosystem. Its market capitalization currently stands at a whopping $4 trillion.

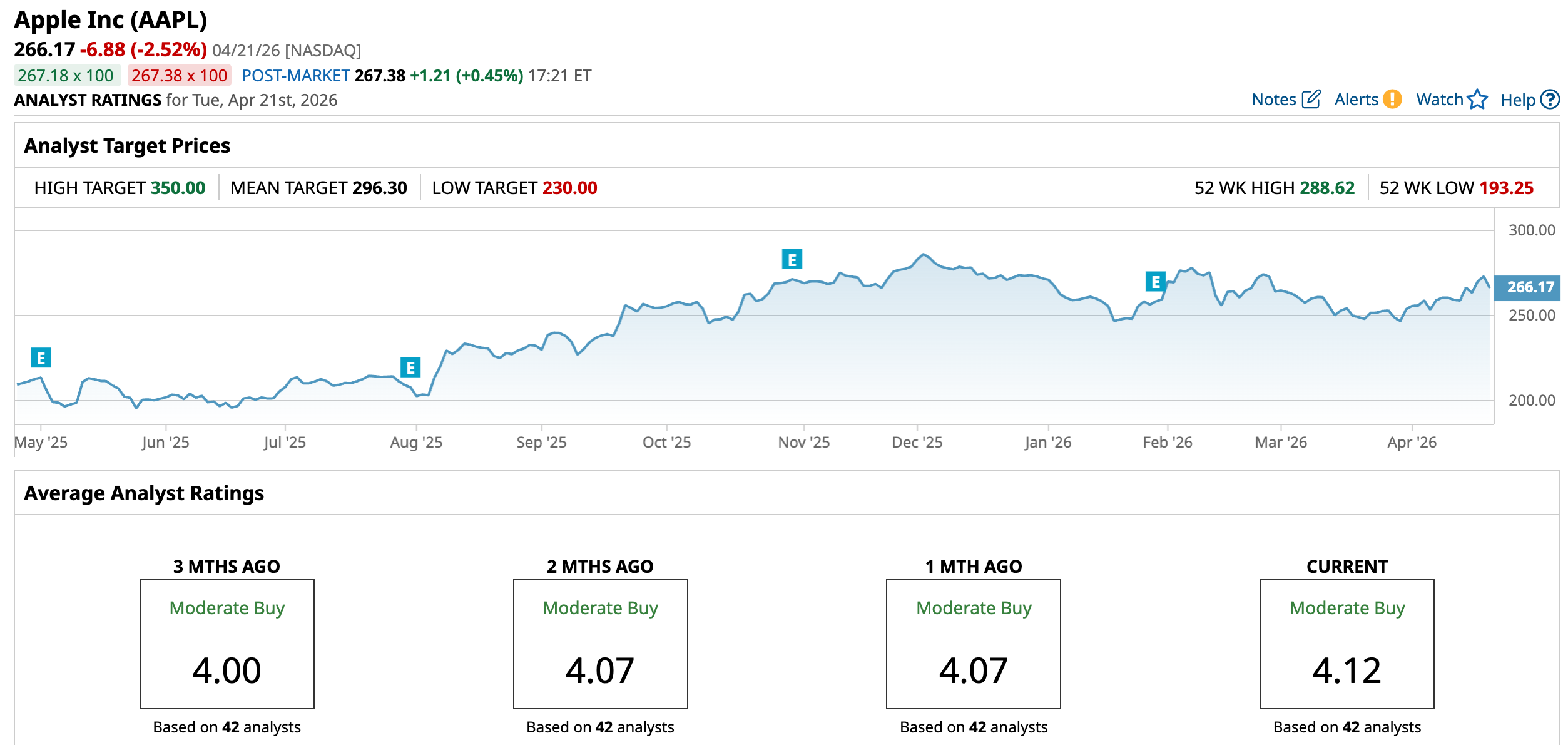

Apple may still wear the innovation crown, but its stock chart this year tells a more layered story. It has not been a straight climb. A mix of global tensions and shifting sentiment around tech, especially concerns about an AI bubble, have kept investors cautious, and Apple hasn’t been immune to that pressure.

Yet, the mood is beginning to change. When I last wrote about AAPL stock back in March, it was still in the red for 2026. Since then, it has inched back into positive territory on a year-to-date (YTD) basis, including a 2.84% gain over just the past five days.

The price action has been fairly disciplined. After slipping into the $200 range in early August, Apple steadily climbed, hitting a peak of $288.62 in early December. Profit-taking followed, pulling it back toward the $250 zone, and it’s now trading around the $270 level. That leaves it roughly 7.8% below its 52-week high and about 5.24% under its YTD high of $280.90. Still, zooming out, Apple’s share are up 37.8% over the past 52 weeks.

Technically, AAPL looks to be gaining some strength again. Trading volumes have picked up, which usually means more investors are stepping in. The 14-day RSI is 56.72, showing the stock is moving higher but not overheated yet.

Plus, MACD oscillator shows a steady bullish setup. The MACD line is above the signal line, typically a sign that the upward trend is holding. Histogram is staying in positive territory, suggesting that the buying pressure is still stronger, keeping momentum tilted in favor of the bulls for now.

AAPL is not exactly a bargain buy currently. The stock is priced at about 31.83 times forward adjusted earnings and 8.59 times sales, sitting above the sector peers and its own historical averages. But investors seem comfortable paying that price because Apple delivers steady performance, strong cash flows, and a loyal customer base that keeps coming back.

The dividend story adds another layer. The company has raised its dividend for 13 consecutive years, while using only about 13% of its earnings to fund it. That leaves enough cushion to keep increasing payouts over time, which is a big reason investors stay comfortable holding the stock.

A Snapshot of Apple’s Q1 Results

Apple released its fiscal first-quarter results on Jan. 29, generating a record revenue of $143.8 billion, up 16% year-over-year (YOY), while EPS amounted to $2.84, rising 19% annually and comfortably beating Wall Street’s expectations.

The biggest driver was the iPhone business, which generated $85.3 billion in revenue, up 23.3% from last year, as demand stayed strong globally. Apple’s services segment continued to deliver steady growth, bringing in a record $30 billion, up 14% YOY. With higher margins, this segment is quietly becoming a key pillar of the business.

But not every segment kept pace. iPad revenue rose modestly to $8.6 billion, while Mac revenue slipped to $8.4 billion, reflecting softer demand in the PC market. Wearables, Home, and Accessories brought in $11.5 billion, slightly lower than last year.

Despite the strong numbers, the stock reaction was muted. The focus quickly shifted to potential challenges. Strong iPhone demand left Apple with tighter inventory, which could limit near-term sales. At the same time, rising memory costs are expected to have a bigger impact ahead, potentially putting pressure on margins.

Looking ahead, Apple is now getting ready to report its fiscal second-quarter results on Thursday, April 30, and there’s optimism building around it. The management has already guided for revenue growth of 13% to 16% for the March quarter, which suggests the momentum is not slowing down just yet.

Also, margins are anticipated to stay stable, thanks to a better product mix. And even though short-term concerns are still in play, Apple’s strong ecosystem and its high-margin services business continue to provide a solid foundation for steady growth.

Meanwhile, analysts monitoring the company remain optimistic, predicting Q2 revenue around $109.6 billion, while EPS is anticipated to rise by 15.8% YOY to $1.91. Looking further ahead to fiscal 2026, profit is anticipated to be around $8.49 per share, up 13.8% YOY, before surging another 9.7% annually to $9.31 per share in fiscal 2027.

What Do Analysts Expect for Apple Stock?

As anticipation builds around a potential Siri upgrade and Apple Worldwide Developers Conference draws closer, the recent leadership transition adds a new twist to the Apple story. Daniel Ives of Wedbush Securities maintained an “Outperform” rating and a $350 price target, but described the shift as a mixed signal.

While he acknowledged Tim Cook’s lasting legacy, he pointed out that the sudden move to Executive Chairman raises questions, especially with Apple entering a key phase in its AI strategy. Ives noted that incoming CEO John Ternus will face immediate pressure to deliver, particularly as investors look for clarity on Apple’s AI direction in the months ahead.

Plus, ahead of Apple’s upcoming quarterly results, Goldman Sachs is asking investors to take a closer look at the tech giant. After a slow start to 2026, analyst Michael Ng thinks it could be buy opportunity now. He reiterated a “Buy” rating with a $330 price target and expects EPS of $2.00 for the quarter, slightly above consensus. His confidence is driven by solid iPhone and Mac demand, healthier margins, and supportive currency trends.

He also pointed to Apple’s efforts to secure DRAM supply as a smart move to manage rising costs. Ng believes Apple remains well-positioned, backed by strong premium demand and continued gains in China, with services like iCloud+ and AppleCare+ adding steady growth.

Meanwhile, Bank of America raised AAPL’s price target to $325, highlighting strong iPhone momentum and Apple’s 21% global smartphone market share in early 2026. The bank views the leadership shift as a move made from strength, not stress. It also sees Apple entering a new device cycle, potentially led by AI-driven wearables and smart home products, with 2027 shaping up as a major milestone year.

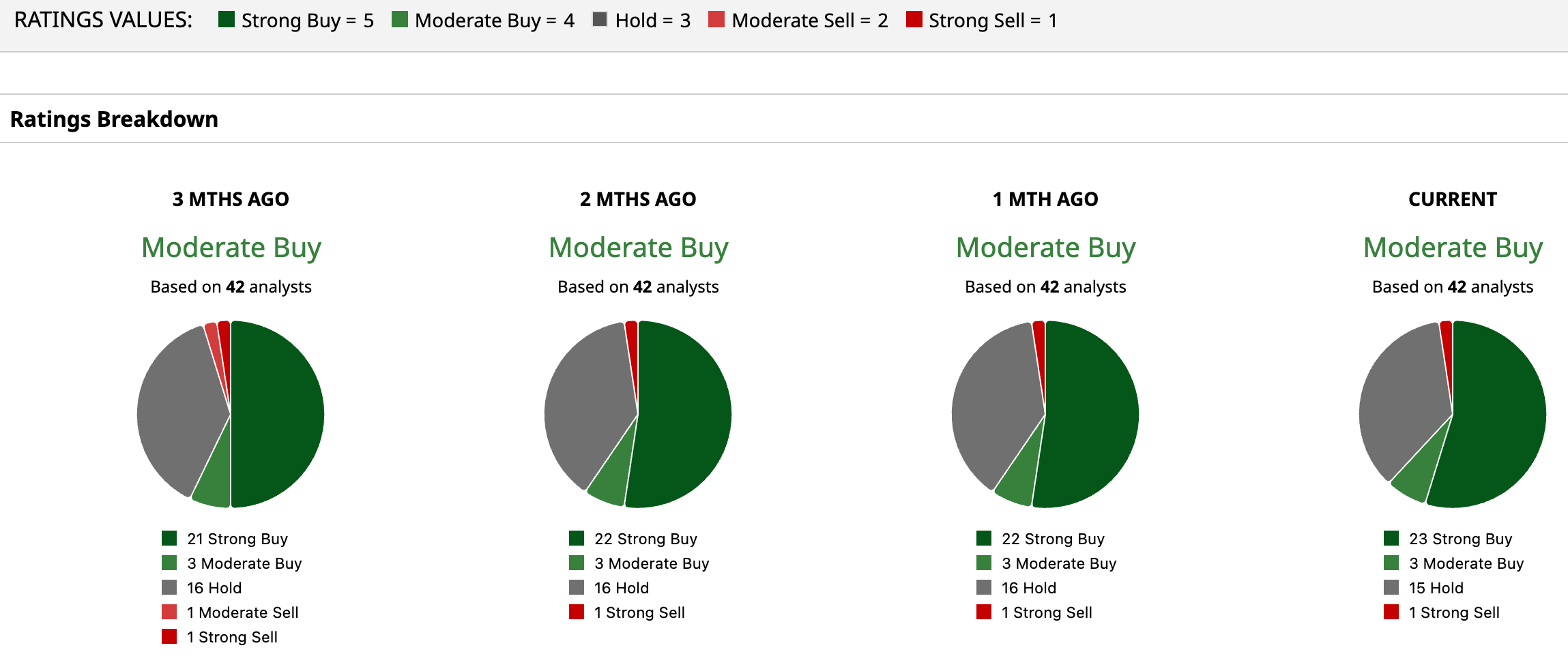

AAPL stock has a consensus “Moderate Buy” rating overall. Out of 42 analysts covering the tech stock, 23 recommend a “Strong Buy,” three give a “Moderate Buy,” 15 analysts stay cautious with a “Hold” rating, and the remaining one analyst has a “Strong Sell” rating.

The average analyst price target for AAPL is $296.30, indicating potential upside of 11.32% from here. However, the Street-high target price of $350 suggests that the stock could rally as much as 31.5%.

Final Thoughts on AAPL Stock

Bringing it all together, the real test for Siri is not just how impressive it looks at launch, but also how useful it feels in everyday life. If it can actually manage multiple tasks, understand what’s on your screen, and work smoothly across apps and devices, it could quietly change how people interact with Apple's ecosystem.

But this upgrade is coming at a time when a lot is already in motion – leadership changes, an upcoming earnings report, and high expectations from the market. That means the pressure is not just to innovate, but to deliver consistently.

The overall picture still looks resilient, with analysts staying positive and the core business holding up well. Meanwhile, challenges like rising costs and supply issues are still there in the background.

So, while an upgraded Siri version could definitely add a new spark to the story, whether it truly moves the needle for the stock, or just adds to the hype, remains to be seen.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)