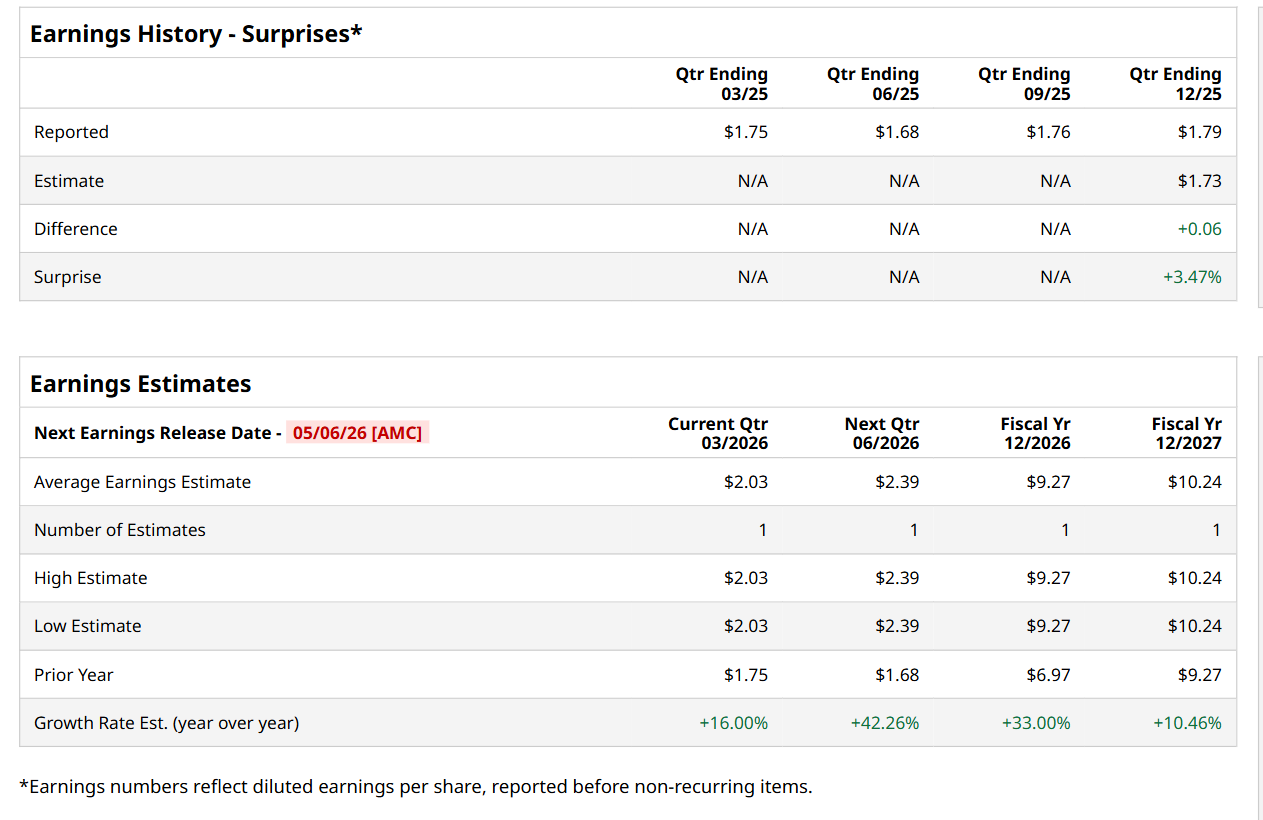

Valued at a market cap of $28.8 billion, Texas Pacific Land Corporation (TPL) is a major landholding company that generates revenue from a diverse range of activities, including oil and gas royalties, the sale of construction materials, comprehensive water sourcing and disposal services, and the management of pipeline and utility easements. This Dallas, Texas-based company is scheduled to announce its fiscal Q1 earnings for 2026 after the market closes on Wednesday, May 6.

Before this event, analysts expect this energy company to report a profit of $2.03 per share, up 16% from $1.75 per share in the year-ago quarter. Its earnings of $1.79 per share in the previous quarter outpaced the forecasted figure by 3.5%.

For the current fiscal year, ending in December, analysts expect TPL to report a profit of $9.27 per share, representing a 33% increase from $6.97 per share in fiscal 2025. Its EPS is expected to further grow 10.5% year-over-year to $10.24 in fiscal 2027.

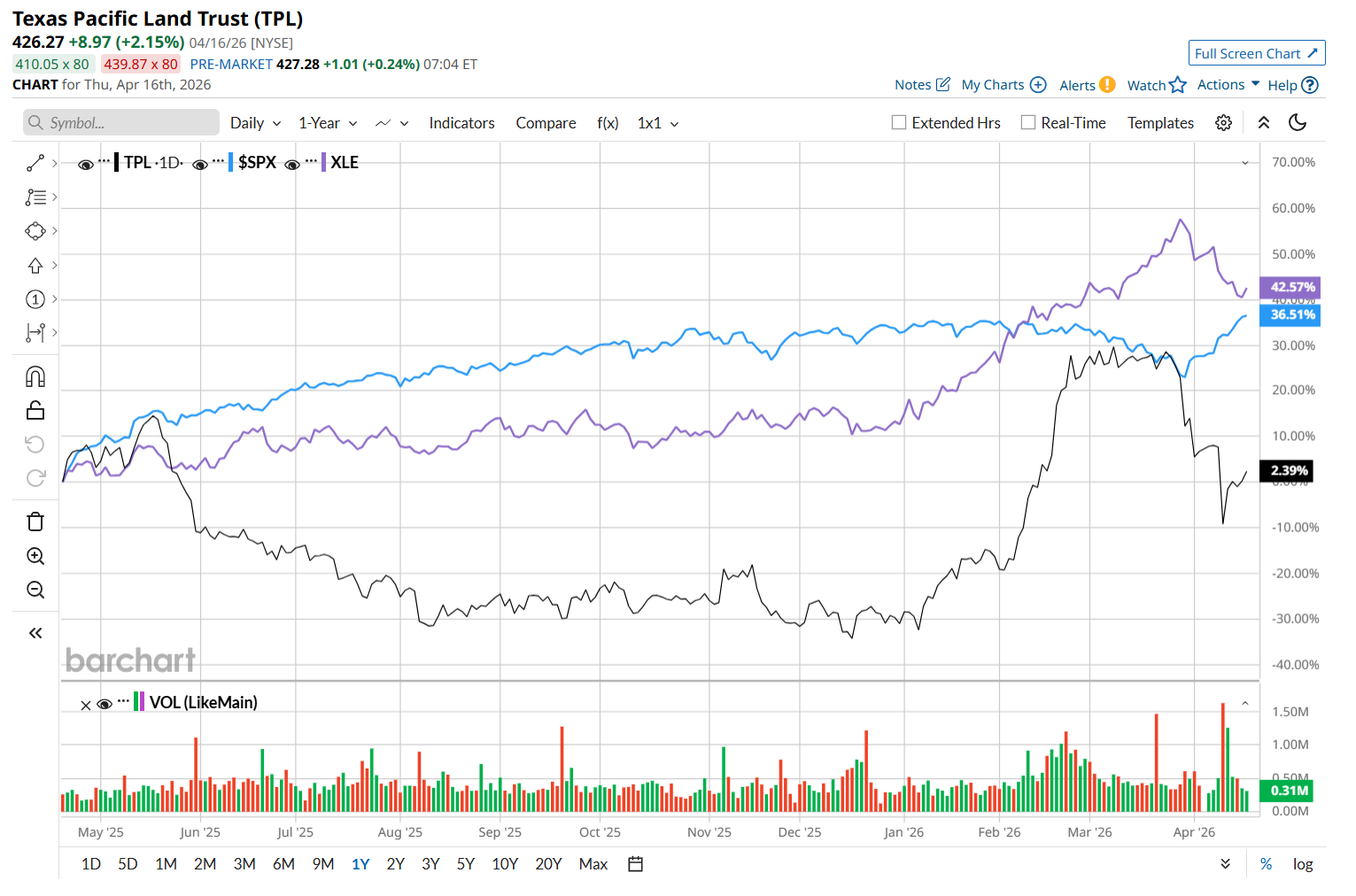

TPL has gained marginally over the past 52 weeks, considerably underperforming both the S&P 500 Index's ($SPX) 33.5% return and the State Street Energy Select Sector SPDR ETF’s (XLE) 42% uptick over the same time period.

However, on a YTD basis, TPL has surged an impressive 48.4%, fueled by a combination of favorable macro trends and strong strategic positioning. Rising geopolitical tensions in the Middle East have reignited the focus on U.S. energy independence, driving oil and gas prices higher and lifting sentiment around energy-linked assets such as TPL.

However, the investment narrative extends well beyond geopolitics. The company is increasingly being recognized for its potential role in enabling next-generation data infrastructure. With Texas rapidly emerging as a hub for AI-driven development, TPL is strategically leveraging its extensive land holdings to capitalize on this shift. In its most recent earnings release, the company announced a $50 million investment in Bolt Data & Energy, Inc., signaling a clear push into large-scale data center development and supporting infrastructure across its properties. This is another key factor drawing heightened investor interest in the stock in 2026.

Wall Street analysts are moderately optimistic about TPL’s stock, with a "Moderate Buy" rating overall. Among three analysts covering the stock, two recommend "Strong Buy," and one suggests a "Hold" rating. The mean price target for TPL is $487, indicating a 14.2% potential upside from the current levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)