/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

Battery storage player Eos Energy Enterprises (EOSE) grabbed investor attention as its shares jumped more than 12% following the announcement of a new joint development agreement with TURBINE-X Energy on Apr. 15. The collaboration will focus on building behind-the-meter power systems for artificial intelligence (AI) data centers and other mission-critical sites, where an uninterrupted and reliable energy supply is essential.

As part of the agreement, TURBINE-X is targeting up to 2 GWh of Eos battery storage over a 36-month project pipeline, with initial deployments expected in 2027. This positions Eos to tap into a growing customer base that prioritizes speed, resilience, and dependable on-site power, while also benefiting from lower upfront costs. At its core, Eos provides large-scale battery storage systems that store electricity and act as backup when needed, while TURBINE-X builds gas turbine-based systems that generate power directly at customer sites.

By combining storage with on-site generation, the partnership aims to offer a more controlled and dependable energy solution. Together, the two companies aim to provide a private, on-site power solution for large operations like AI data centers, environments where even brief disruptions or delays from the traditional grid can have serious consequences. So, with this new development in place, should you buy EOSE stock now?

About Eos Energy Stock

Founded in 2008, Eos Energy Enterprises is an American energy storage company that develops battery systems for the electric grid. Its zinc-based technology is designed for long-duration energy storage, allowing utilities, independent power producers, and commercial users to store electricity and access backup power when needed. The company’s battery energy storage system (BESS) is built on its Znyth technology, which uses non-precious, widely available materials.

This chemistry is designed to be non-flammable and stable, offering an alternative to conventional battery systems. Eos’ solutions are used across utility-scale, microgrid, commercial, and industrial settings, typically supporting storage durations ranging from four to 16+ hours. These systems are intended to help manage increasing grid demand and complexity while enabling more consistent use of stored energy.

Currently valued at $2.4 billion by market capitalization, Eos Energy has had a rough run this year. The stock came under pressure following a disappointing Q4 update in late February, and sentiment worsened further after a securities fraud class action lawsuit filed in April accused the company of misrepresenting its manufacturing timelines.

As a result, shares have struggled to find a footing, falling roughly 38% in 2026 so far, a sharp contrast to the broader S&P 500 Index ($SPX), which has managed a modest 2.7% gain year-to-date (YTD). Nevertheless, there are early signs of a rebound. The stock has climbed 19.24% over the past five days, supported by optimism around its new AI data center partnership and preliminary Q1 2026 guidance pointing to record shipments and improving manufacturing consistency.

Inside Eos Energy’s Financial Performance

Eos Energy delivered its Q4 and full-year 2025 results on Feb. 26, and the reaction was swift and harsh. The report came in as a mixed bag, with major misses on both revenue and earnings, triggering a steep 39.44% sell-off in a single session. While the company posted record quarterly revenue of $58 million, up nearly 700% year-over-year (YOY) thanks to efficiency gains, quality improvements, and increased automation, it still fell well short of the roughly $93.69 million analysts had expected.

Profitability remained under pressure. Eos reported a gross loss of $54.4 million, though this marked a 230-point margin improvement from the prior year, reflecting better product margins. However, the bottom line weighed heavily on sentiment. The company posted a net loss of $0.84 per share, missing estimates of a $0.20 loss, even though it improved from the prior year’s $2.20 loss per share. This earnings miss was a key factor behind the sharp double-digit drop in the stock.

Despite these setbacks, Eos exited the year with a much stronger balance sheet. The company held $624.6 million in cash, supported by a $600 million senior convertible notes issuance. It also entered 2026 with a backlog of $701.5 million and a large commercial opportunity pipeline valued at over $23.6 billion, suggesting that while execution has been uneven, demand for its zinc-based storage systems remains strong. For the full-year 2026, management expects revenue to land between $300 million and $400 million.

Momentum began to shift in earlier this month. On Apr. 9, the company released a preliminary Q1 fiscal 2026 outlook that helped restore some investor confidence. Eos projected revenue between $56 million and $57 million, sparking a nearly 29.6% rally in the stock. The update pointed to improving manufacturing consistency, with record shipments rising 17% quarter-over-quarter. Additionally, the company reported record quarterly battery output (up 10.4%) and record bipolar output (up 10.6%), signaling operational progress.

Another key milestone was the progress on “Line 2,” the company’s second highly automated production line, which successfully completed Factory Acceptance Testing. Expected to go live by the end of Q2 2026, this new line features a more efficient single-piece flow design, reducing raw material travel distance by 86%, a step that could further improve efficiency and scalability going forward.

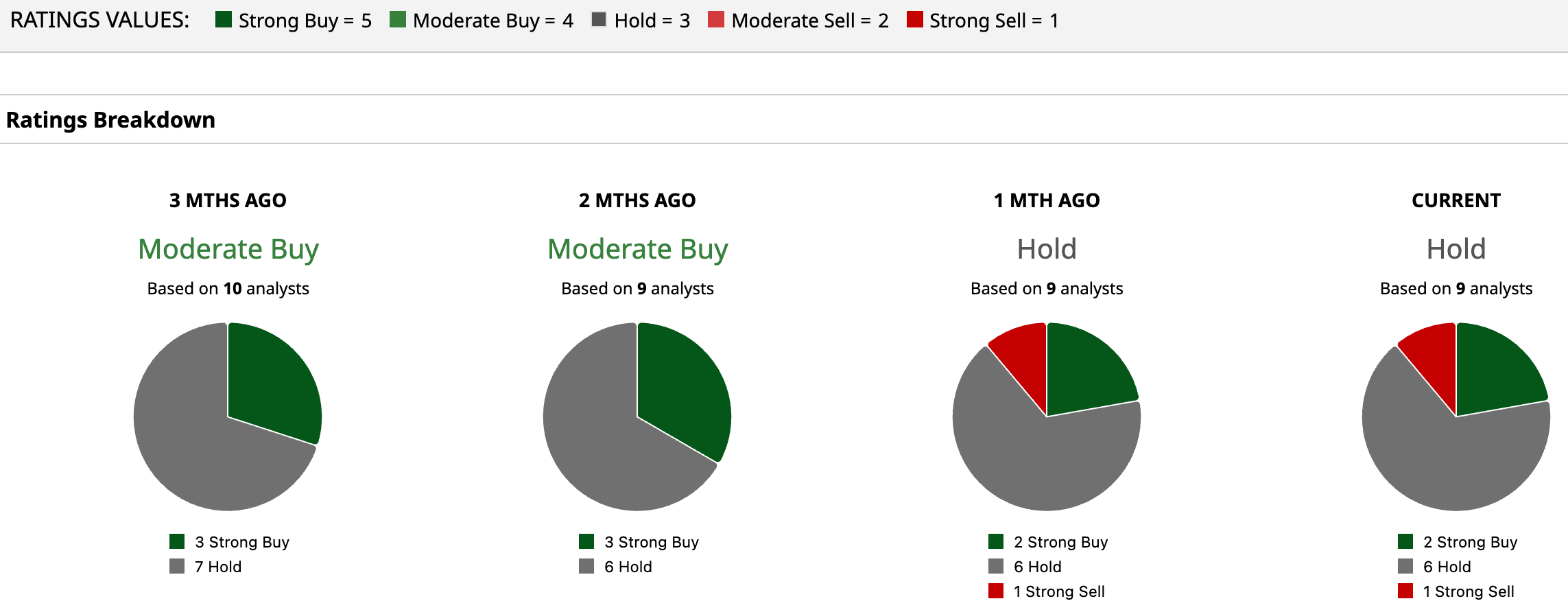

How Are Analysts Viewing Eos Energy Stock?

Despite the recent bounce in shares, Wall Street isn’t fully convinced on Eos Energy, with the stock currently carrying a consensus “Hold” rating overall. Among the nine analysts covering the name, two are bullish with “Strong Buy” calls, six prefer to stay on the sidelines with “Hold,” and one remains firmly bearish with a “Strong Sell.”

The upside case still looks meaningful. The average price target of $9.29 points to potential gains of 30.3%, while the Street-high target of $18 suggests the stock could rally as much as 152.5% from current levels.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)

/Sign%20of%20Intel%20at%20entrance%20%20by%20michaelmond.jpeg)

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)