/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

The man who called the 2008 housing collapse just doubled down on his bet against Nvidia (NVDA). When Michael Burry makes a move, Wall Street pays attention. And his latest call, a fresh bet against Nvidia, is one of the more provocative contrarian stances in recent memory.

Burry, best known for predicting the 2008 financial crisis, just revealed that he has increased his bearish position in NVDA stock. He's loading up on long-dated put options and standing firmly against what has become the most crowded trade in markets today.

Alternatively, just weeks ago, Nvidia CEO Jensen Huang stood on the GTC 2026 stage and told analysts he had over $1 trillion in demand visibility for Blackwell and Rubin chips, a number he called conservative. The bull and bear cases could not be further apart.

Burry Bets Against Nvidia

In a recent Substack post, Burry laid out his reasoning clearly, according to a report from TheStreet.

- He purchased January 2027 put options at the $115 strike price for $3.30 while continuing to hold $100-strike puts acquired earlier. Burry described the trade as representing roughly three percent of notional value.

- The core argument is that Nvidia's valuation has been stretched to the point where there is almost no room for disappointment.

- He also raised concerns about whether the massive wave of data-center spending can sustain itself at current levels.

- Perhaps most dramatically, he drew a direct comparison between Nvidia and Cisco (CSCO) during the dot-com boom.

- Cisco was the must-own infrastructure stock of that era. Then it collapsed by roughly 90% and took about 25 years to regain its 2000 peak.

Burry's implication is hard to miss, and his new position takes that broader institutional caution and sharpens it into a pointed directional bet.

The Bull Case for Nvidia

At GTC 2026, Huang told analysts the company now has strong demand visibility exceeding $1 trillion for Blackwell and Rubin products through the end of 2027. He was explicit that this figure excludes newer products such as Rubin Ultra, Groq, and standalone CPUs, suggesting that the total addressable opportunity is larger.

Huang also made the case that, in addition to selling chips, Nvidia is selling manufacturing infrastructure for artificial intelligence tokens, the output that every AI company needs to generate revenue. In that framing, the price of the hardware matters far less than the tokens it produces.

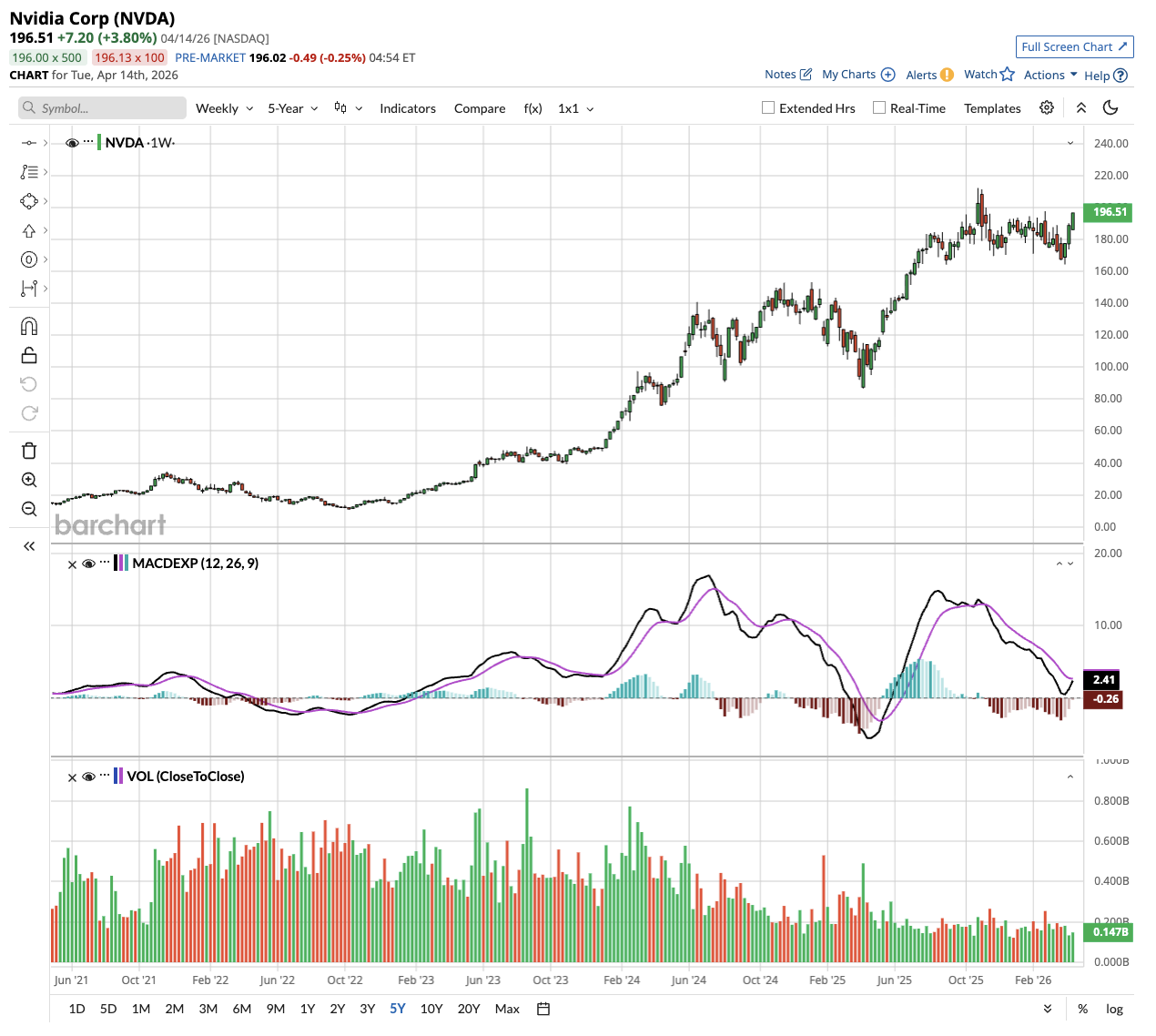

Fiscal year 2026 revenue grew 65% year-over-year (YoY), with the fourth quarter up 73%. The chipmaker also reported more than $95 billion in supply obligations, reflecting the scale of demand it is managing.

Should NVDA Stock Investors Buy, Sell, or Hold?

Burry's Cisco comparison is not outlandish, given that infrastructure stocks during tech booms can get very expensive, very fast. But Nvidia’s growth story is far from over. Analysts tracking NVDA stock forecast revenue to increase from $215.6 billion in fiscal 2026 to $757.6 billion in fiscal 2031.

In this period, adjusted earnings per share are forecast to expand from $4.77 to $16.70. If NVDA stock is priced at 20x forward earnings, which is lower than its current multiple of 23x, it could be priced at $334 in early 2030, above the current price of $196.

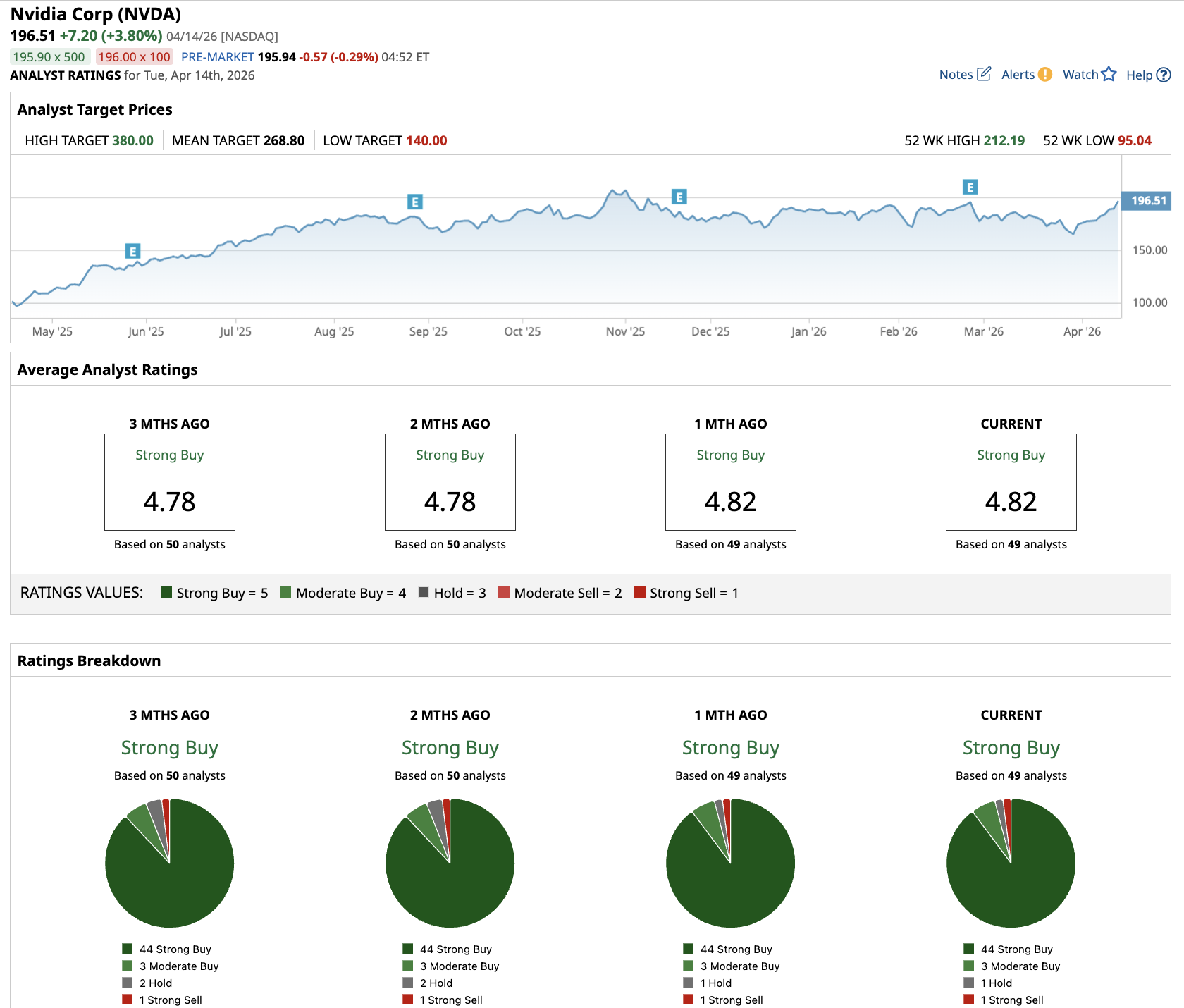

Out of the 49 analysts covering NVDA stock, 44 recommend “Strong Buy,” three recommend “Moderate Buy,” one recommends “Hold,” and one recommends “Strong Sell.” The average Nvidia stock price target is $268.80, indicating almost 40% upside from current levels.

Every company in the world will need an AI strategy, and Nvidia's platform sits at the foundation of that buildout. The $1 trillion demand figure is not a forecast but is also backed by firm purchase orders.

For long-term investors, the question is not whether Burry's bearish thesis is clever. It is whether the AI buildout has more runway than the market is currently pricing in. Holding NVDA stock through volatility has rewarded patient investors before. Whether that continues depends on whether the AI infrastructure boom proves more durable than Burry is betting.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)