Netflix (NFLX) has evolved into a global media powerhouse, using artificial intelligence (AI) to drive recommendations, advertising, and user engagement at scale. While it explored acquiring Warner Bros. Discovery (WBD) assets, the company ultimately stepped away from the bidding war with Paramount Skydance (PSKY), signaling confidence in its organic growth strategy. Netflix heads into its Q1 earnings on April 16 with a focus sharper than ever on scaling its advertising business toward a $3 billion opportunity this year.

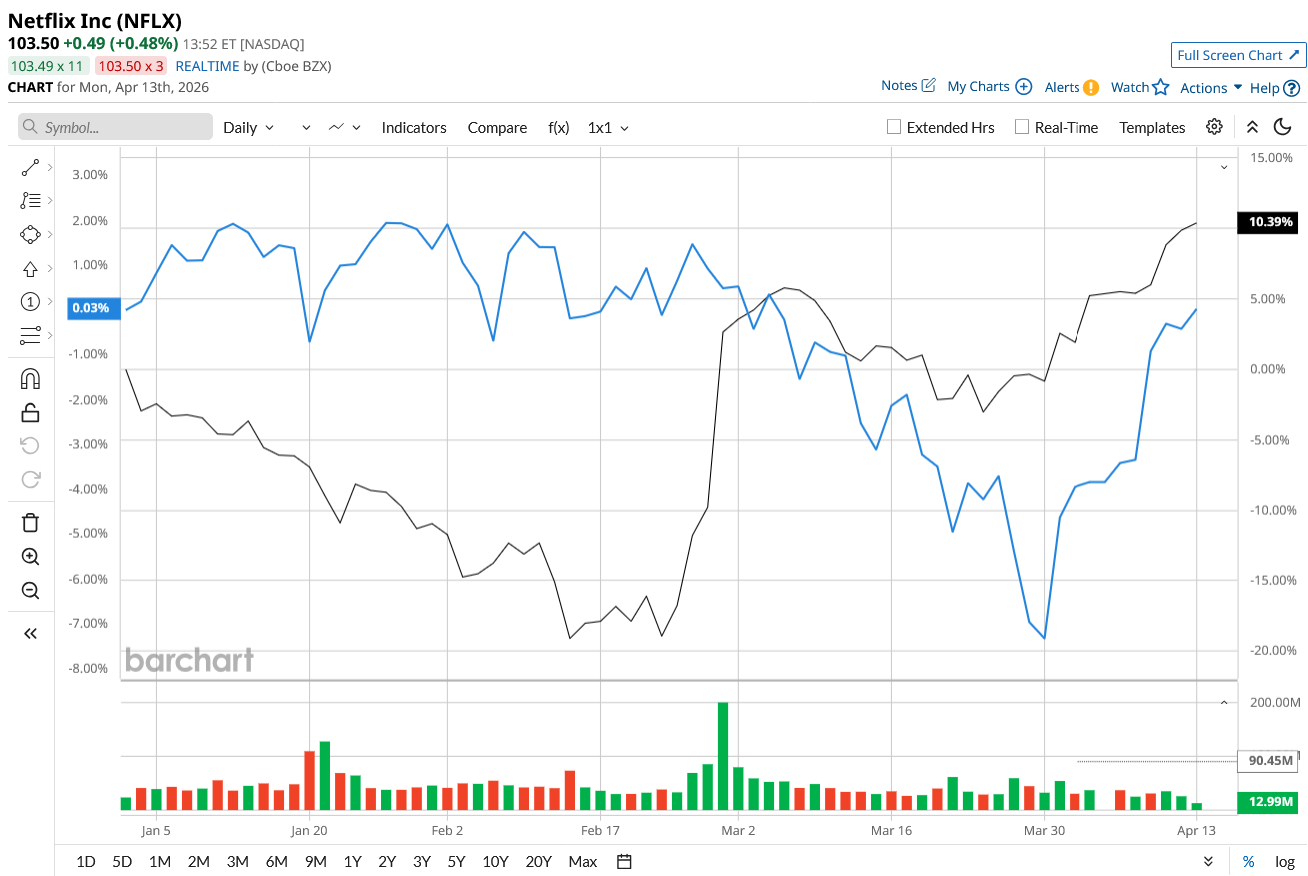

The bidding war took a toll on the stock, although its earnings growth remained robust. NFLX stock is up 10% YTD but has dipped sharply by 23% from its 52-week high of $134.12. Will Netflix’s growth strategy push the stock toward an ambitious target like $150?

Advertising: The Next Billion-Dollar Growth Engine

While Netflix intended the acquisition to deepen its content moat, walking away from the bidding war might have been the best decision from a financial standpoint. It could now preserve balance sheet strength and protect margins from integration costs. It also confirms to investors that Netflix's core business, which is driven by subscriptions, unique content, pricing power, and advertising, will continue to be its major growth engine.

In 2025, Netflix’s revenue grew 16% year-over-year (YoY) to $45.2 billion, followed by an earnings per share (EPS) increase of 27.7% to $2.53 per share. Netflix has been working on improving its core business by enhancing content quality and variety, along with newer initiatives like live programming, video podcasts, and cloud-based gaming. These formats could boost user engagement and retention, resulting in pricing power and long-term revenue growth.

Heading into Q1 earnings, Netflix's advertising business is the core theme investors need to watch out for. Management made it clear during the Q4 earnings call that ads remain central to its long-term strategy. The ad business generated $1.5 billion in revenue in 2025. The company now expects it to double to $3 billion in 2026. Management believes ad monetization is still in the early stages. In Q1 earnings, investors should watch out for updates on features such as ad pricing, engagement metrics, and the introduction of new formats such as AI-powered interactive ads, which might help Netflix reach its $3 billion target.

From just a subscription-only platform, Netflix is now evolving to a hybrid model that combines subscription revenue with high-margin advertising income. The company is planning to invest heavily in content, to around $20 billion in 2026. Content quality and variety have allowed the company to retain pricing power. This is probably why, despite multiple price increases, Netflix remains a “must-have” platform for most subscribers.

Financially, the company remains in a healthy position. It ended Q4 with $14.5 billion in gross debt and $9 billion in cash and equivalents. A robust free cash flow balance of $9.5 billion will enable it to reduce its debt levels. For the first quarter, revenue is expected to increase by 15.3% to $12.1 billion, with EPS of $0.76. For the full year, Netflix expects 14% YoY growth in revenue to $51 billion. Any upgrade in full-year guidance could help boost the stock.

Even with its massive global reach, Netflix still accounts for under 10% of total TV viewing time in key markets and captures only around 7% of the overall consumer and advertising spending opportunity, according to company estimates. This implies its platform is still in the early stages of capturing a much larger opportunity.

What Does Wall Street Say About NFLX Stock Now?

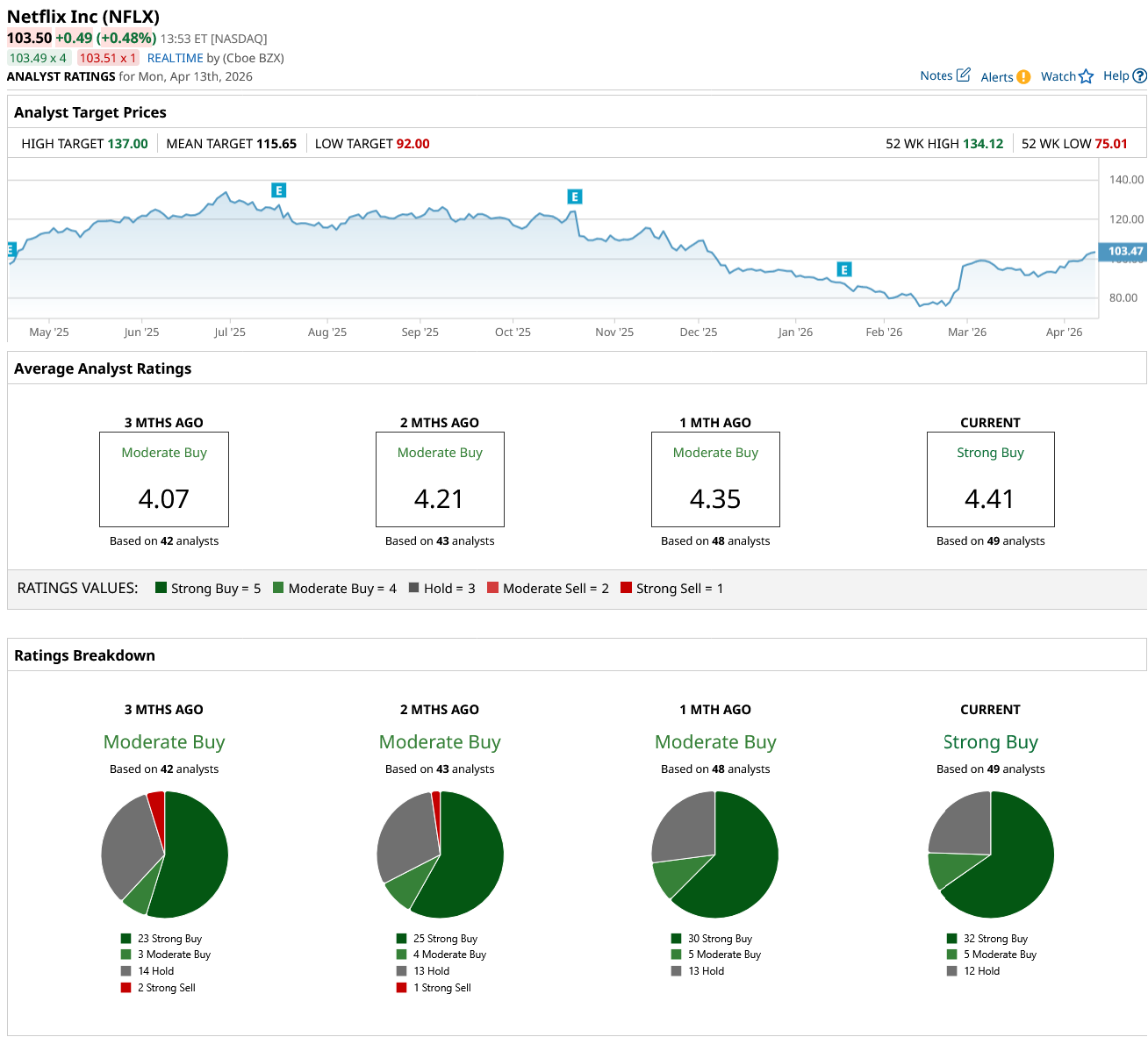

Heading into Q1 earnings, analysts at UBS, Jefferies, BMO Capital, and Goldman Sachs reaffirmed their “Buy” ratings on Netflix. Overall, Wall Street remains highly optimistic and now rates NFLX stock a “Strong Buy” over a “Moderate Buy” rating a month ago. Of the 49 analysts covering the stock, 32 recommend a “Strong Buy,” five rate it as a “Moderate Buy,” and 12 suggest holding. Based on an average price target of $115.65, Wall Street anticipates a potential upside of around 12% over the next 12 months.

Robert W. Baird has a high price estimate of $150, which indicates NFLX stock could gain as much as 45.6% this year. Analysts believe the company will deliver exceptional growth in 2026, with revenue projected to increase by 13.6% to $51.3 billion and EPS to rise by 24.6% to $3.15 per share. Revenue and earnings are further expected to increase by 11.7% and 22.8% in 2027. If Netflix delivers this level of growth, hitting a high price target of $150 doesn’t seem far-fetched.

Netflix’s shares are trading at a premium of 32 times forward earnings and eight times forward sales. However, given its strong subscriber growth, pricing, and rapid expansion of advertising, the premium seems justified.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)