/Micron%20Technology%20Inc_logo%20and%20website-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)

After a stellar run over the past year, fueled by the artificial intelligence (AI) boom, leading semiconductor giant Micron Technology (MU) is leaning even further into the trend, and investors are paying close attention. On Apr. 8, Micron shares jumped 7.72% after the company announced a strategic investment in SiMa.ai, a fast-growing player in Physical AI.

The goal is to boost the production of advanced AI solutions designed for real-world use cases such as robotics, autonomous systems, and industrial automation. This partnership combines SiMa.ai’s powerful Modalix MLSoC architecture with Micron’s LPDDR5X memory, delivering faster performance, higher bandwidth, and lower power consumption. These advantages are critical for efficiently running complex workloads such as Large Language Models (LLMs) and Vision Language Models (VLMs) at the edge.

SiMa.ai has already launched System-on-Modules powered by Micron memory, signaling early commercialization and real traction in the market. With this investment, Micron is expanding beyond its traditional memory business and strengthening its position in the rapidly evolving Physical AI space, opening up a new avenue for long-term growth. Given this latest development, is MU stock a buy now?

About Micron Stock

Headquartered in Idaho, Micron Technology stands as a key force in the global semiconductor industry and is known for its advanced memory and storage solutions. As one of the world’s largest chipmakers, the company focuses on DRAM and NAND technologies that underpin modern computing systems. In recent years, Micron has sharpened its strategic focus on enterprise and data center markets, stepping away from its consumer-facing Crucial brand to concentrate on higher-growth opportunities tied to AI infrastructure.

With cutting-edge High Bandwidth Memory (HBM) and energy-efficient server solutions, Micron is effectively supplying the critical backbone for large language models (LLMs), positioning itself to capitalize on the accelerating wave of global generative AI investment. Currently boasting a market capitalization of roughly $474.3 billion, Micron is enjoying a powerful run on Wall Street, with its shares delivering impressive gains. And it’s not just the recent SiMa.ai investment driving the momentum.

A wave of bullish analyst calls has reinforced confidence in Micron’s AI-driven growth story, while improving macro sentiment, particularly with the ceasefire in the Middle East. It has sparked a broader “risk-on” rally across the semiconductor sector. Together, these tailwinds are amplifying investor optimism and helping fuel Micron’s continued surge.

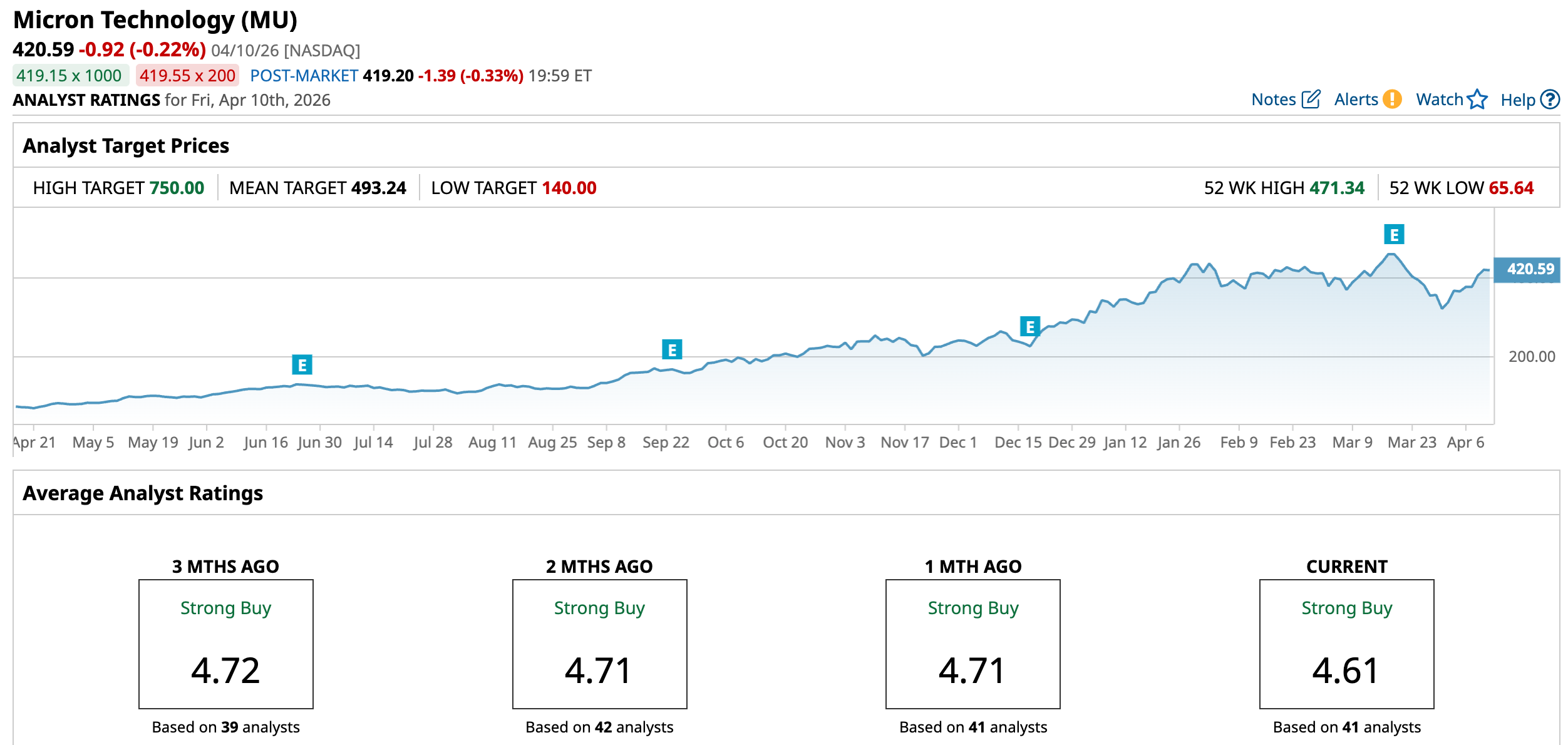

After delivering a staggering 500.4% rally over the past year, Micron has carried that momentum into 2026, with the stock climbing another 47.36% year-to-date (YTD). In comparison, the broader S&P 500 Index ($SPX) rose 29.4% last year and has edged marginally lower so far this year, making Micron’s outperformance even more striking. Micron hit a record high of $471.34 on March 18, and even after a modest pullback, the stock is still hovering just 10.8% below its peak, highlighting the strength of its ongoing AI-driven rally.

Inside Micron’s Q2 Earnings Report

Micron’s fiscal 2026 second-quarter earnings report, released on March 18, was nothing short of historic, characterized by triple-digit growth that effectively shattered Wall Street’s expectations. The company smashed records across revenue, gross margin, EPS, and free cash flow, fueled by surging demand, tight industry supply, and flawless execution. During the quarter, Micron reported a record-breaking revenue of $23.86 billion, a staggering 196.4% increase year-over-year (YOY) and a 75% jump from the previous quarter.

Of course, that remarkable top line figure blew past Wall Street’s expectation of $19.61 billion. The strength was broad-based. Quarterly revenue nearly tripled from a year ago, with DRAM, NAND, HBM, and every business unit hitting record highs. DRAM led the charge with $18.8 billion in revenue, soaring an eye-popping 207% YOY and accounting for 79% of total sales. NAND wasn’t far behind, generating roughly $5 billion, up 169% annually.

This powerful top line growth translated into even stronger profitability, as Micron’s shift toward high-margin AI products paid off in a big way. On the bottom line, Micron posted adjusted EPS of $12.20, an explosive 682% YOY jump, crushing expectations of $8.80. Gross margins more than doubled to 74.4%, compared to 36.8% a year ago, highlighting tight supply conditions and the company’s ability to command premium pricing for its advanced memory products.

Cash generation remained equally impressive. During the quarter, Micron invested about $5 billion in capital expenditures while still delivering $6.9 billion in adjusted free cash flow. The company exited the quarter with $16.7 billion in cash, marketable investments, and restricted cash, alongside total liquidity of $20.2 billion, underscoring its strong financial position. Looking ahead, the momentum shows no signs of slowing.

For fiscal Q3 2026, Micron expects revenue of $33.5 billion, plus or minus $750 million, with gross margins projected to climb further to 81%. Non-GAAP EPS is forecast in the range of $18.75 to $19.55. To meet surging demand, the company now plans to ramp fiscal 2026 capital spending above $25 billion, including approximately $7 billion in Q3 alone, while still generating significantly higher free cash flow on the back of stronger operating cash flow.

How Are Analysts Viewing Micron Stock?

Wall Street’s confidence in Micron is only getting stronger. On Apr. 8, UBS raised its price target to $535 from $510 while maintaining a “Buy” rating, citing improving pricing trends across both DRAM and NAND, especially in HBM, where demand remains red-hot. Industry checks point to active negotiations with hyperscalers and OEMs, involving long-term deals, volume commitments, pre-payments, and structured pricing.

Notably, major players like Micron, SK Hynix, and Samsung are looking to rebuild premium HBM pricing through 2027, signaling confidence in sustained demand and stronger margins ahead. Also, UBS is far more bullish than the broader Street, forecasting Micron’s EPS to hit around $135 in 2027 and $120 in 2028, well above consensus estimates. The firm believes memory companies are prioritizing long-term visibility over short-term gains, reinforcing the durability of the current upcycle.

With potential supply shortages, particularly in DRAM, extending into 2028, the setup remains favorable for continued pricing power. Meanwhile, analysts at BofA Securities see the AI infrastructure boom entering a more stable and scalable phase, with global investment expected to nearly triple to $1.4 trillion by 2030. They highlight a steady capital spending intensity of 25% to 30% as hyperscalers and governments upgrade systems for AI workloads. In this environment, Micron stands out as a key beneficiary, especially in HBM, which is critical for AI chips.

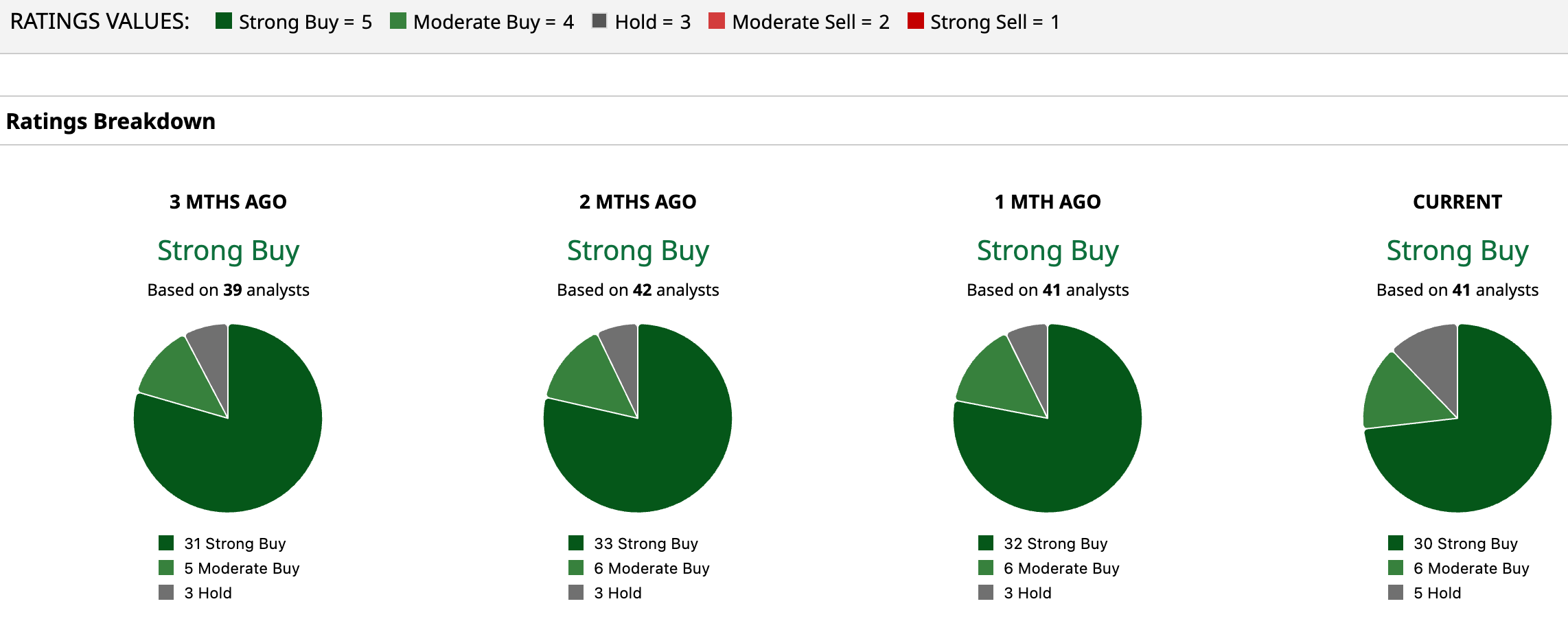

Overall, Wall Street’s confidence in Micron remains overwhelmingly strong, with the stock commanding a consensus “Strong Buy” rating. Out of 41 analysts, a dominant 30 are firmly bullish with “Strong Buy” calls, while six more lean positive with “Moderate Buy,” and just five remain cautious with “Hold” ratings, highlighting how decisively sentiment tilts in Micron’s favor. The upside case is just as compelling.

The average price target of $493.24 implies a healthy 17.27% gain from here, while the Street-high target of $750 points to a massive 78.3% upside. For investors, it signals that despite its impressive run, Micron may still have plenty of fuel left in the tank.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)