Meta (META) is still in the red for the year, with legal, regulatory, and heavy spending worries dragging on the mood around the company. In late March, the stock had its worst day in months, dropping about 8% after back-to-back jury verdicts tied to harm and child safety issues. That run also included a $375 million penalty in New Mexico and fresh concern over how much it is pouring into AI projects.

Legal pressure is growing, too, with high-profile lawmakers now pushing a bill that would pause new AI data centers across the country. All of this helps explain why the share price has struggled even while the wider AI theme keeps charging on.

There is another side to the story starting to form. The launch of the new Muse Spark model has pulled fresh attention back to the company and what it is building.

That growing interest leads to a simple question for anyone following along. Could Muse Spark be what finally shifts the mood and helps the stock start to make back its 2026 losses, or is the buzz getting ahead of what the business can deliver right now? Let's dive in.

Meta’s Surprisingly Strong Financials

Meta Platforms is based in Menlo Park, California, and runs some of the world’s biggest social, messaging, and advertising apps, along with newer AI features. The company is worth about $1.55 trillion and now pays a forward annual dividend of $2.10 per share, which works out to a 0.37% yield.

META’s share price is $627.28 as of April 10, with a year-to-date (YTD) return of -5.3% and a 52‑week gain of 14%.

META is not cheap. It trades at a forward P/E of 19.34x and a price/cash flow of 15.31x, compared with sector medians of 12.61x and 7.82x, so the market is clearly pricing in stronger growth and profits than the average peer.

Their latest earnings report for the quarter ended Dec. 25 showed EPS of $8.88 versus a consensus estimate of $8.21, an 8.16% upside surprise that came with quarterly sales of $59.89 billion, up 16.88% year-over-year (YoY).

That same period saw net income jump to $22.77 billion, a huge 740.46% increase from the prior year, helped by earlier cost cuts and better efficiency. The company also generated $115.8 billion in operating cash flow in December 2025, up 45.50%, which gives it plenty of room to keep spending on growth.

Even with net cash flow at -$6.34 billion, the 81.08% improvement suggests heavy spending is going into long‑term projects rather than signaling a problem with the core business.

Meta’s AI Comeback Story

Meta recently rolled out Muse Spark as its first big AI model from its Superintelligence Labs, and the launch has already given the stock a bounce in early April, even though it is still down for the year. This model is only one part of a bigger shift. Meta has laid out four generations of in-house MTIA chips, built with Broadcom, with MTIA 300 already running ranking and ads, and MTIA 400, 450, and 500 planned to handle heavier AI work through 2027.

That hardware push is being matched by changes on the people and org side. The company has formed a new AI engineering team that works with its Superintelligence Lab, aiming to turn research into real features more quickly across its apps and devices.

Management is also leaning on deals to move faster. Meta is buying Moltbook, an AI-focused social platform, and plans to bring that team into its superintelligence group to help build out agent-style tools and new social experiences.

On top of that, there is the buildout behind the scenes. Meta has signed a large multi-year partnership with Nvidia (NVDA), which brings in advanced chips and networking gear for its data centers so it can train and run models at scale.

The company is also working with Corning (GLW) on a cable plant in North Carolina to handle heavier AI data traffic and is spending more on data centers overall, which shows how serious the company is about making this AI push stick.

META Stock's Big Money and Street Backing

Meta’s next earnings date is coming up on April 29, 2026, and it covers the first quarter of 2026 with an average EPS estimate of $6.67 versus $6.43 a year ago. This works out to roughly 3.73% expected growth.

Big money has not stepped away either. Pershing Square Capital Management, led by Bill Ackman, said in its 2026 Annual Investor Presentation on Feb. 11 that META stock made up 10% of its capital at the end of 2025, an investment of about $2 billion. That same presentation pushed back on worries that heavy spending or rising AI rivals would permanently hurt META’s earnings power or long-term margins.

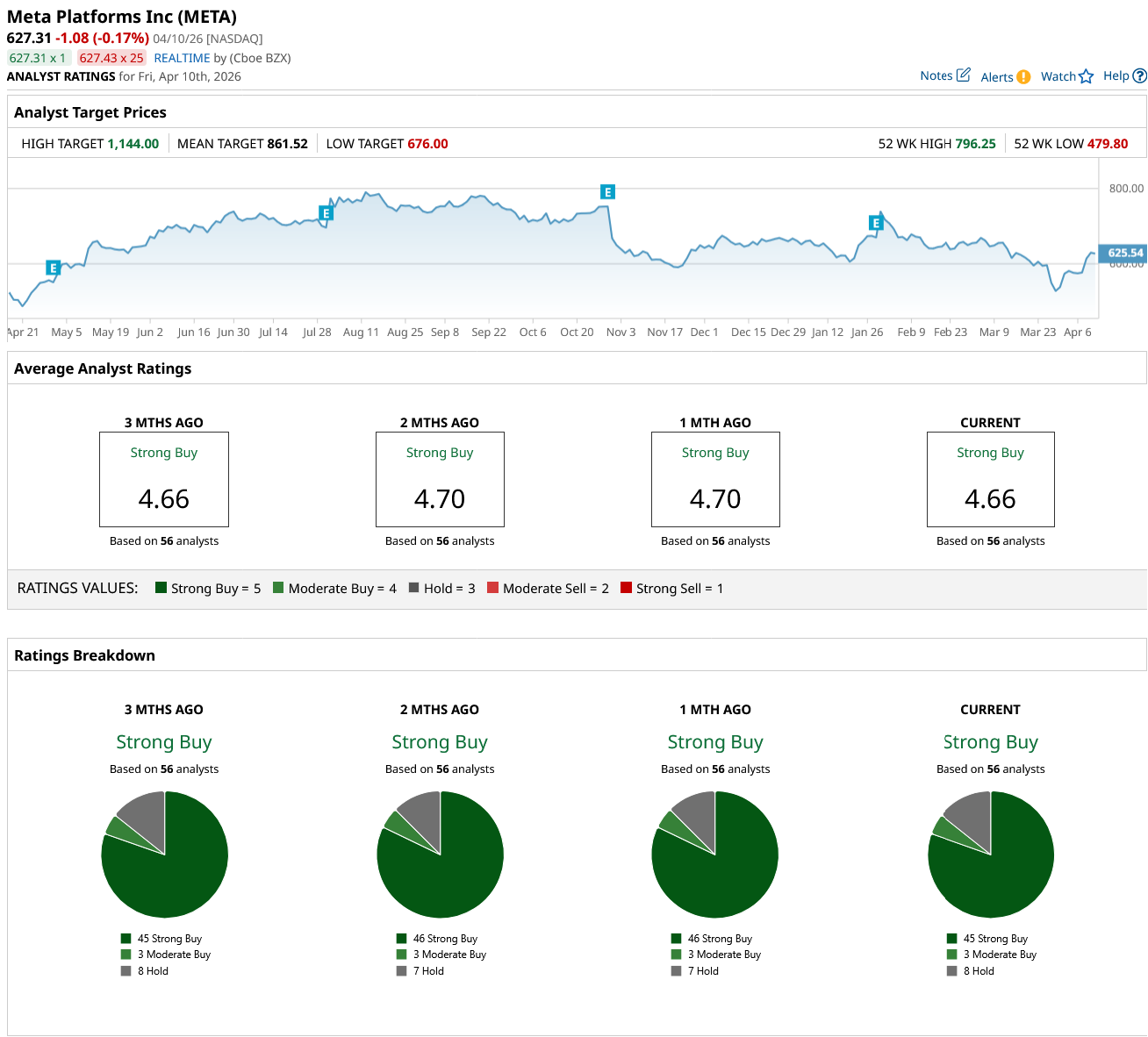

Support like that lines up with what Wall Street is signaling. The consensus view from 56 analysts is a “Strong Buy” rating on META stock, with an average price target of $861.52, which points to about 37% upside from current levels.

Conclusion

Muse Spark on its own will not suddenly wipe away META’s YTD losses. It does make the story around the company stronger by adding to solid earnings, big spending on growth, and clear backing from large funds.

The setup looks more like a slow grind higher than a fast rebound, especially if the next few quarters land close to or above expectations. With upbeat price targets and all the money going into AI, the odds still lean toward the stock pushing higher over the medium term, even if the ride is bumpy.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)