The price action in technology stocks has been mixed, with the industry making some big investments on the back of global artificial intelligence (AI) demand. One McKinsey report from 2025 indicates that a “$5.2 trillion investment in data centers will be needed by 2030," per Reuters. As tech giants undertake these investments, there is an element of skepticism in the markets.

This, however, provides invesotrs with an opportunity for a good entry point into innovation-driven tech companies like Meta Platforms (META). META stock is currently up 8% for the past 52 weeks but down roughly 1% year-to-date (YTD).

Recently, Meta Platforms announced the establishment of an AI engineering organization to boost superintelligence efforts. The organization will partner with Meta's Superintelligence Lab to build the data engine that helps improve the company's models. It’s worth noting that Meta has already been working on AI models, with plans to start shipping in the coming months.

With Meta moving beyond 2D screens, the focus on AI-driven innovation is likely to unlock value. Potential game changers include the company's Meta Quest devices, its AI glasses and its broad focus on entertainment, gaming, fitness, and learning. Accordingly, it might be a good time for investors to consider exposure to META stock.

About Meta Platforms Stock

Headquartered in Menlo Park, California, Meta Platforms develops products that enable people to connect and share through devices like smartphones, computers, and virtual reality (VR) headsets. This objective is served through the company's apps, which include Facebook, Messenger, Instagram, and WhatsApp. Meta has a strong global presence and reported 3.58 billion daily active users on its apps as of December 2025.

For fiscal 2025, Meta reported total revenue of $201 billion. Of this figure, advertising revenue was $196.2 billion, remaining the growth driver. The company's Reality Labs revenue was $2.2 billion for the full year while Family of Apps accounted for $198.7 billion.

Backed by steady growth in daily active users and revenue per person, Meta reported sales growth of 22% year-over-year (YOY) for fiscal 2025. However, amidst the volatility in tech stocks, META stock has declined by 13% for the past six months and 1% YTD. This correction seems like a good accumulation opportunity, as Meta’s cash flows swell and the company boosts its investment in AI-driven growth.

Meta's Positive Financial Metrics

Meta continues to invest significantly in innovation that’s likely to drive growth in the coming years. One factor that supports aggressive investment is high financial flexibility. As of fiscal 2025, Meta reported a cash buffer of $81.6 billion. Further, operating cash flow for fiscal 2025 was $115.8 billion. It’s likely that cash flows will continue to swell as revenue per user increases.

For Q4 2025, the family average revenue per person was $16.56 as compared to $14.25 in Q4 2024 and $12.33 in Q4 2023. Clearly, there is a steady uptrend, and revenue should continue to swell even if active users remain stagnant.

Another point to note is that, for Q4 2025, Meta reported that about 68% of total revenue came from the U.S., Canada and Europe. Accordingly, there is ample scope for growth in emerging markets where the active user base is considerable.

What Do Analysts Say About META Stock?

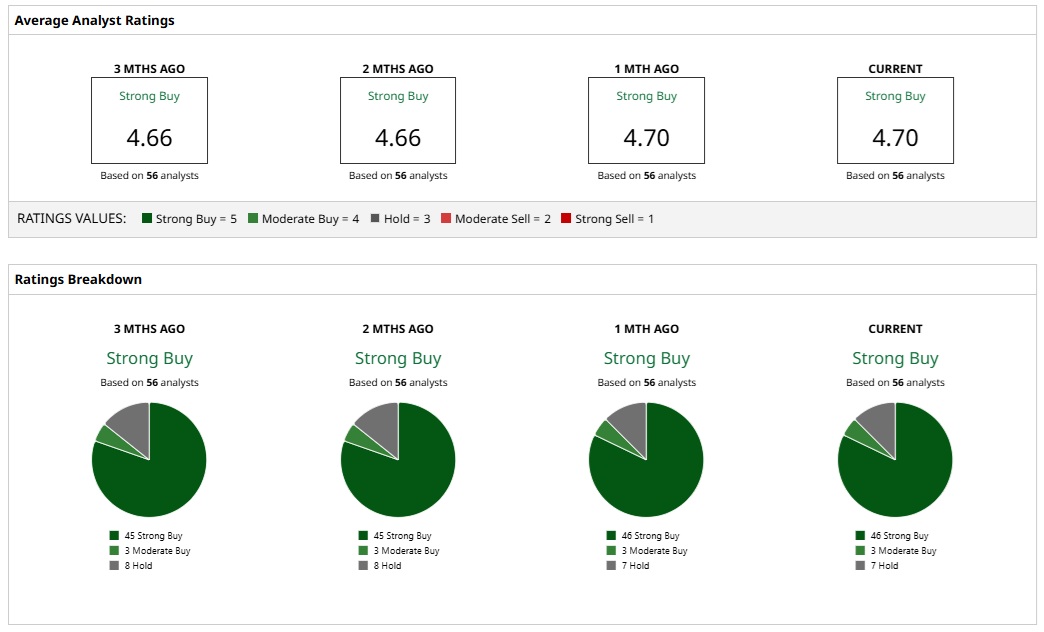

Based on 56 analysts with coverage, META stock is a consensus “Strong Buy.” While 46 analysts assign a “Strong Buy” rating, three analysts have a “Moderate Buy" rating, and seven analysts have a “Hold.” The mean price target of $864.04 implies about 32% potential upside from here. Further, the most bullish price target of $1,144 suggests that META stock could rise as much as 75% from current levels.

Valuation is one factor that supports the overwhelmingly bullish analyst rating. META stock trades at a forward price-to-earnings (P/E) ratio of roughly 21.8 times. This is attractive, considering the multiple growth engines for the company. With companies like Meta, Alphabet (GOOGL), and Amazon (AMZN) also all trading close to 20 times earnings based on 2027 estimates — per Evercore ISI head of internet research Mark Mahaney — the volatility in the tech sector appears to be a good opportunity to buy one of these mega-cap names.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)