/Henry%20Schein%20Inc_%20logo%20on%20phone-by%20Piotr%20Swat%20via%20Shuttestock.jpg)

New York-based Henry Schein, Inc. (HSIC) is a global healthcare solutions provider that primarily serves office-based practitioners such as dentists and physicians. With a market cap of $8.7 billion, the company distributes a broad range of products, including medical supplies, dental equipment, pharmaceuticals, and vaccines, while also offering value-added services and practice management software.

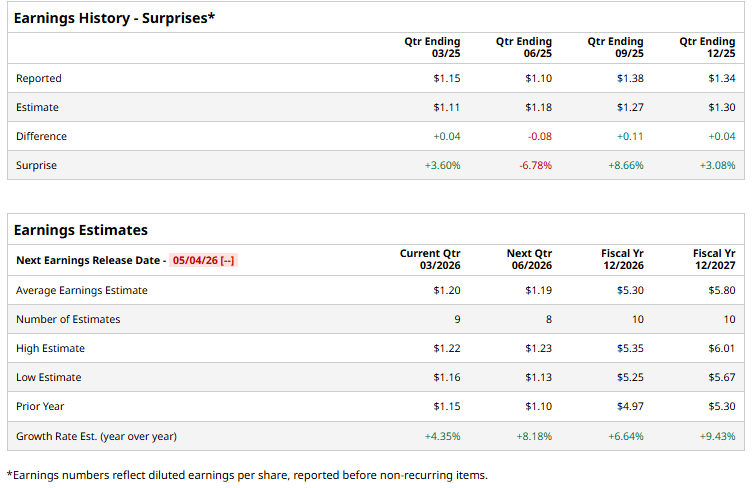

The health care solutions giant is expected to announce its fiscal first-quarter earnings for 2026 soon. Ahead of the event, analysts expect HSIC to report a profit of $1.20 per share on a diluted basis, up 4.4% from $1.15 per share in the year-ago quarter. The company beat the consensus estimates in three of the last four quarters while missing the forecast on another occasion.

For the current year, analysts expect HSIC to report EPS of $5.30, up 6.6% from $4.97 in fiscal 2025. Its EPS is expected to rise 9.4% year over year to $5.80 in fiscal 2027.

Shares of HSIC have soared 14.3% over the past year, lagging the S&P 500’s ($SPX) 25.1% gains but surpassing the State Street Health Care Select Sector SPDR Fund’s (XLV) 7.6% rise over the same time frame.

Henry Schein has faced challenges over the past year due to soft demand in dental markets, margin pressures, and slower growth expectations. The company has faced weaker patient traffic and reduced discretionary dental procedures, which weigh heavily on its core dental segment. At the same time, inflation in input and operating costs has pressured profitability, and investments in technology and transformation have further constrained margins.

Additionally, supply chain disruptions and integration challenges in its specialty and technology businesses have limited near-term earnings momentum, leading investors to favor faster-growing healthcare and tech names in the broader market.

Analysts’ consensus opinion on HSIC stock is reasonably bullish, with a “Moderate Buy” rating overall. Out of 16 analysts covering the stock, seven advise a “Strong Buy” rating, eight give a “Hold” rating, and one suggests a “Strong Sell” rating.

HSIC’s average analyst price target is $89.07, indicating a potential upside of 17.8% from the current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)