/Tesla%20Inc%20elon%20musk%20by-%20Frederic%20Legrand-CO%20via%20Shutterstock(1).jpg)

Tesla (TSLA) heads into its Apr. 22 earnings with an eerie silence. The stock has lost one-third of its value since hitting all-time highs in December last year. Elon Musk has been relatively subdued and hasn’t said anything controversial about the company. U.S. sales are weak but offset by strength in China and Europe. Inventories are rising. Yet none of this explains the consistent decline in stock price during the first quarter of the year. What gives?

The nature of the sell-off suggests investors are only adjusting to a new valuation, not a new headline, as is often the case with Tesla stock. For years, Tesla has traded on narrative. Its most recent buzzwords include autonomy, robotics, and AI. Considering the global geopolitical situation and a wave of inflation hit the U.S. economy, investors are asking Tesla to back the narrative with numbers, or else, they’ll go elsewhere. This is precisely what is generating a new buying opportunity in the stock.

About Tesla Stock

Tesla operates as a developer, designer, manufacturer, seller, and lessor of electric vehicles as well as energy generation and storage systems. It operates through the Automotive and Energy Generation & Storage segments. The company also offers sedans and sport utility vehicles, services for electric vehicles, purchase financing and leasing, and limited vehicle warranties and extended service plans. It was founded in 2003 and is based in Austin, Texas.

The stock posted an impressive performance over the last year, surging around 27%, while the broader S&P 500 Index ($SPX) gained 25% during the same period. The company’s slight outperformance relative to the S&P 500 highlights its potential and the confidence investors place in its stock. It must be added, though, that the stock has lost one-fifth of its value this year alone, underperforming the broader market. This makes the upcoming earnings report all the more important.

Tesla’s valuation always brings back the ‘not just a car company’ debate, and that has never been truer than it is today. The company’s valuation is at the end of the spectrum with a forward P/E of 244 times. For context, it’s 5-year average forward P/E is 146.6 times. Investors today are paying a huge premium despite the recent dip.

The reason is quite simple. Tesla sits on data that its nearest competitor cannot even imagine accumulating. The value of over six million cars on the road, sending the company driving data every single second, is immense. This data will power the autonomy that, together with AI, will change how people travel. Is 244 times the right multiple to pay for that growth? The answer is yes, simply because these new technologies can be scaled to unlock trillions in future value. Some may be worried about the threat posed by Alphabet's (GOOG) (GOOGL) Waymo, but those robotaxis operate on a completely different technology that would be extremely hard to scale.

Deliveries Drop But FSD Adoption Grows

Tesla announced its fourth-quarter fiscal 2025 earnings on Jan. 25. Despite a 16% drop in deliveries, automotive gross profit remained flat compared to the previous quarter. Overall gross profit margin for the quarter was 20.1%. FSD adoption grew to nearly 1.1 million paid users worldwide. The energy segment contributed $12.8 billion in revenue, representing a 26.6% year-over-year (YOY) growth. The company generated $1.4 billion in free cash flows.

In 2026, Tesla expects major capital spending to exceed $20 billion. These funds will focus on robotics, AI, and manufacturing expansions, including Megablock and Megapack 3. Due to policy changes, low-cost competition, and tariffs, the company projects margin pressure in its energy segment. FDS will move to a fully subscription model, which may affect short-term automotive margins. First-quarter earnings are set to be released on Apr. 22.

What Are Analysts Saying About Tesla Stock

George Gianarikas from Canaccord maintained a “Buy” rating on the stock with a price target of $420 ahead of the Q1 earnings report. He pointed out the strong demand for electric vehicles in the U.S., supported by rising used-Tesla prices and higher gas prices. The analyst expects the market to improve further, especially if Elon Musk delivers a new family-focused model that is more appealing than a minivan.

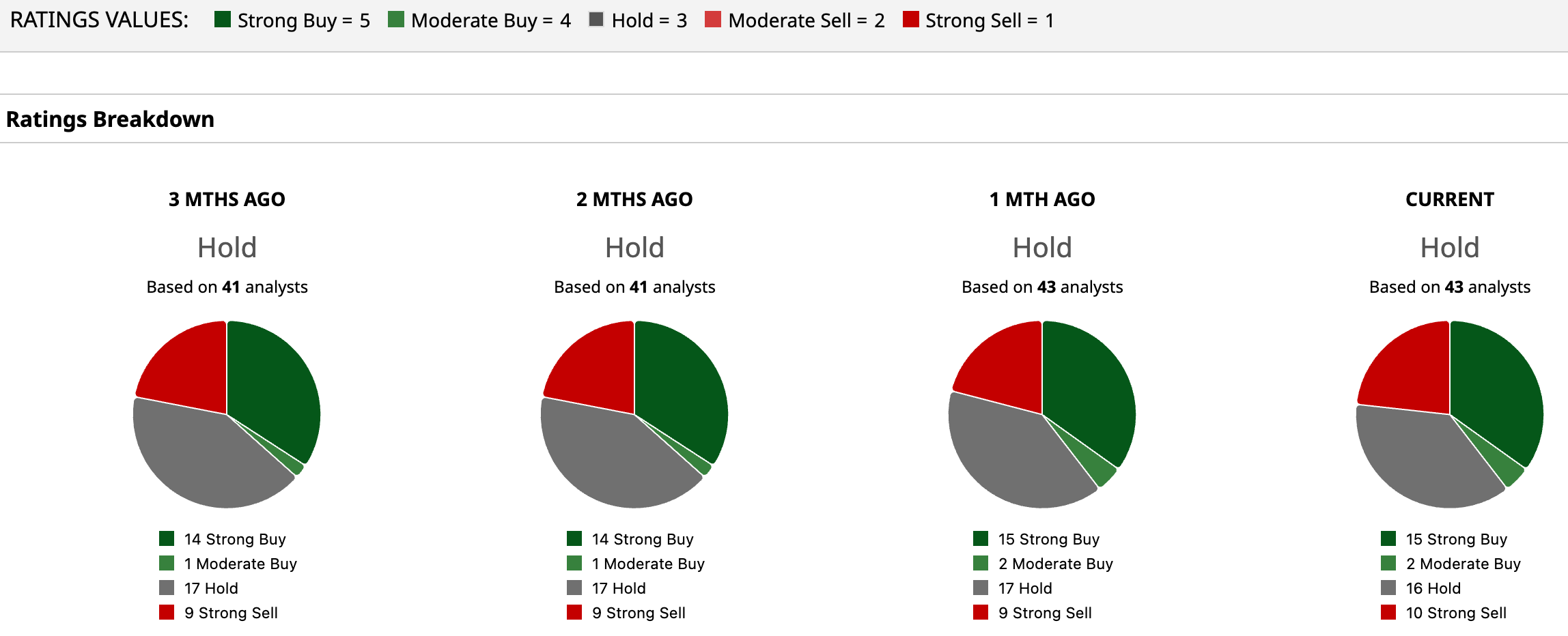

Based on 43 analyst estimates, Tesla stock has a consensus "Hold" rating. The stock has a mean price target of $403.47, reflecting about 16.74% upside from the current levels.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)