Oil prices (QAM26) have cooled off a touch, helped by reports that the United States, Iran, and regional mediators are still talking about a possible ceasefire, including reopening the vital Strait of Hormuz for shipping traffic. That brief sense of relief has not fully relaxed energy markets, however, especially after President Donald Trump paired talk of “deep negotiations” with threats of “all hell” if no deal is reached.

Despite talks, Iran’s Foreign Ministry dismissed the proposal, casting doubt on any near-term resolution and keeping global energy markets tense. These developments have trickled into broader market sentiment, shaping new pressures for businesses heavily tied to transportation and fuel costs.

One company feeling that strain more than most is Carvana (CVNA). The company's operations depend on nationwide vehicle delivery. Following these pressures, Bank of America shifted CVNA stock to a “Neutral” rating, cautioning that rising oil prices could squeeze margins and temper the company’s recent momentum.

The question now is whether this new risk will stall Carvana’s impressive run or simply test its resilience. Let’s dive in.

Carvana’s Financial Metrics

Based in Tempe, Arizona, Carvana operates an online platform for buying and selling used vehicles across the United States. Carvana has a market capitalization of about $70 billion.

Shares opened at $340.44 on April 8. As of this writing, CVNA stock is down 21% year-to-date (YTD) but has seen a 52-week gain of 90%.

The valuation remains elevated, with the trailing price-to-earnings (P/E) ratio at 39 times compared to the sector median of 15 times. Meanwhile, the price-to-sales (P/S) multiple of 3.4 times sharply exceeds the 0.91 times median benchmark.

Carvana released Q4 2025 earnings on Dec. 25, delivering mixed but strong results. Revenue came in at $5.60 billion versus analyst estimates of $5.25 billion, increasing 58% year-over-year (YOY) and beating estimates. Adjusted EPS reached $4.22, handily topping forecasts of $1.11, representing a significant improvement from prior quarters. Carvana also reported adjusted EBITDA of $511 million against the estimated $539.1 million, translating to a 9.1% margin and a modest 5.2% shortfall.

This performance maintained an operating margin of 7.6%, consistent with the year before, pointing to disciplined cost management even as operational scale increased. The company closed the fiscal year with $20.32 billion in total revenue and net income of $1.41 billion, or $8.45 per share, reflecting solid profitability.

Cash flow performance for the quarter adds another positive layer to the story. The company’s operating cash flow reached $1.04 billion, up 71% sequentially, showing stronger liquidity and better business efficiency. Net cash flow also stood at $669 million, increasing 45% from the previous quarter, signaling steady balance‑sheet improvement.

Carvana’s Core Moves

Carvana has been busy laying the groundwork for long-term expansion. The company recently confirmed a 5-for-1 stock split to make its shares more accessible to retail investors and improve overall trading liquidity. That announcement marked a key step in continuing its momentum after a strong earnings year and rising investor participation.

Following that was another wave of expansion news directly reinforcing Carvana's delivery capabilities. The firm extended its same-day delivery service to Los Angeles, tapping into one of the largest U.S. car markets. This push into high-volume urban areas strengthens Carvana’s value proposition by shortening delivery times and enhancing customer satisfaction.

That same strategy matches the company's rollout of same-day delivery to Eugene, Oregon, proving Carvana's focus on spreading operational efficiency beyond major metro hubs. Each new market adds scale to the firm's logistics network, balancing nationwide inventory management and customer reach.

How Do Analysts View Carvana Stock?

Carvana is set to release first-quarter 2026 earnings on April 29, with analysts expecting an average EPS of $1.43. That compares with $1.51 from the same period last year, reflecting a 5% YOY decline.

Some analysts have gone even further with their bullish calls on Carvana, however. UBS recently set a $485 target on CVNA stock, projecting further potential for expansion in margins once short-term pressures from higher operating costs ease.

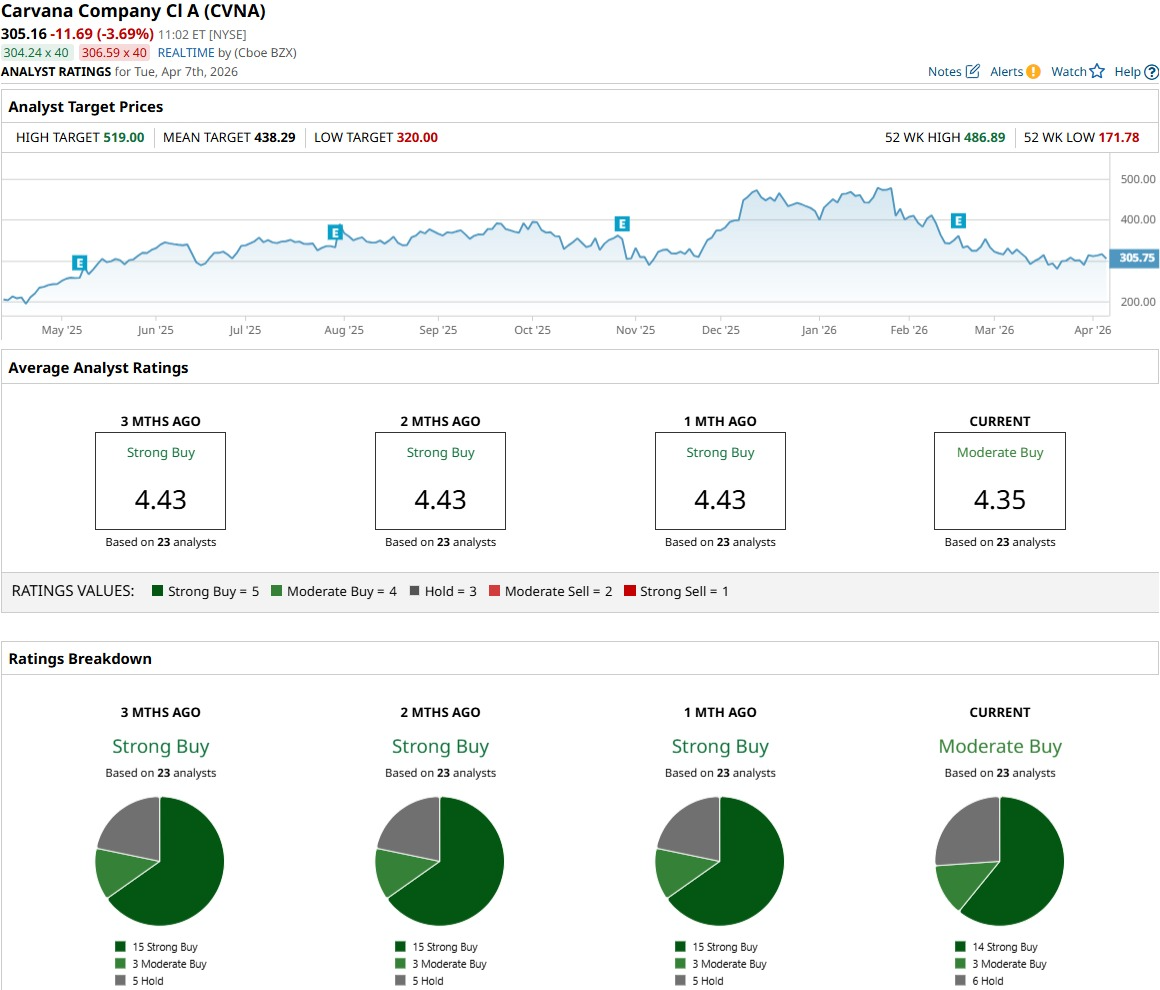

Even with that mild contraction, analysts remain optimistic, as 23 experts give CVNA stock a consensus “Moderate Buy" rating. The average price target of $438.29 suggests strong investor conviction in the company’s recovery potential, representing about 29% potential upside.

Conclusion

Carvana’s growth story remains intact, even as short-term pressures from higher oil prices cloud the outlook. The recent downgrade from BofA signals caution, but the company’s fundamentals and analyst confidence still point to strong underlying momentum. Most signs suggest that CVNA stock could stabilize and edge higher once fuel costs ease and sentiment improves. The coming earnings report will likely decide the next move, but the long-term setup leans positive.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)