/AI%20(artificial%20intelligence)/AI%20by%20TierneyMJ%20via%20Shutterstock.jpg)

Artificial intelligence (AI) has been the core investment theme of the decade, but 2026 is showing that even the hottest sectors don’t move in a straight line. After a massive multi-year rally, investors are now rotating out of AI stocks toward more stable and resilient sectors like energy and the consumer sector. Still, AI hasn’t lost all of its momentum and could be the central theme even in the next decade. While some companies continue to dominate on fundamentals, others are quietly positioning for a comeback.

This split is creating a new opportunity for investors to play the next phase of AI. On one side stands Nvidia (NVDA), which remains the backbone of the AI revolution even as NVDA stock cools. On the other side is Intel (INTC), a legacy chip giant attempting one of the most ambitious turnarounds in semiconductor history.

Nvidia: The AI King Facing a Pause, Not a Decline

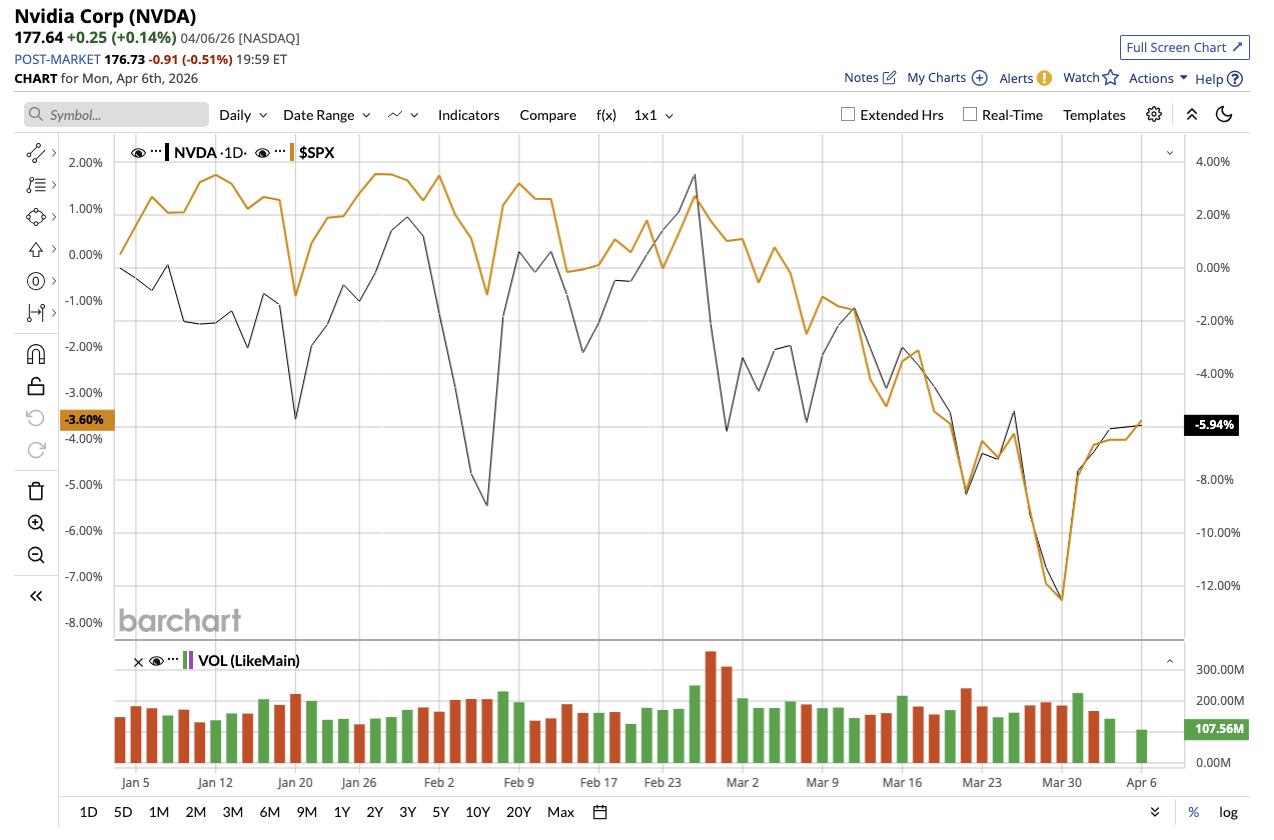

Nvidia has dominated the AI space, powering everything from large language models (LLMs) to hyperscale data centers. Over the past five years, NVDA stock has returned around 1,019%. Despite this dominance, the stock that has powered the market over the last few years is suprisingly suffering a rough patch this year. Nvidia stock is down 3% year-to-date (YTD), compared to the overall market's dip of 1% YTD.

Investors now wonder if the AI trade is losing steam. But this is less about Nvidia’s fundamentals, which remain solid as ever, and more about broader market dynamics.

Nvidia’s data-center segment has grown roughly 13 times since fiscal 2023, reflecting how its GPUs have become the gold standard for training and deploying AI. Importantly, demand visibility remains unusually strong for Nvidia’s products. The Blackwell architecture is seeing strong adoption. Combined with its CUDA software ecosystem, Nvidia has built a full-stack advantage that competitors still struggle to match.

Management recently emphasized that the “transition to accelerated computing and the infusion of AI across existing hyperscale workloads” continues to drive growth, indicating that the AI cycle is still in its early stages. Nvidia has secured supply agreements through 2027, as hyperscalers alone are estimated to drive capital expenditures to $700 billion, providing a significant tailwind for Nvidia's core business. Nvidia earned $97 billion in adjusted free cash flow in fiscal 2026, giving it substantial financial flexibility to spend on product innovation while returning capital to shareholders.

Analysts predict EPS to increase by 68% in fiscal 2027 to $7.66, followed by 31% growth in fiscal 2028 to $10.05. For this rate of estimated growth, the chip giant currently trades at a discount of 23 times forward earnings.

For investors, Nvidia’s long-term growth hasn’t changed. The recent stock dip is not a sign of weakening fundamentals, but rather a natural cooling period after an explosive run. This pullback could be a great opportunity for long-term investors to accumulate shares now.

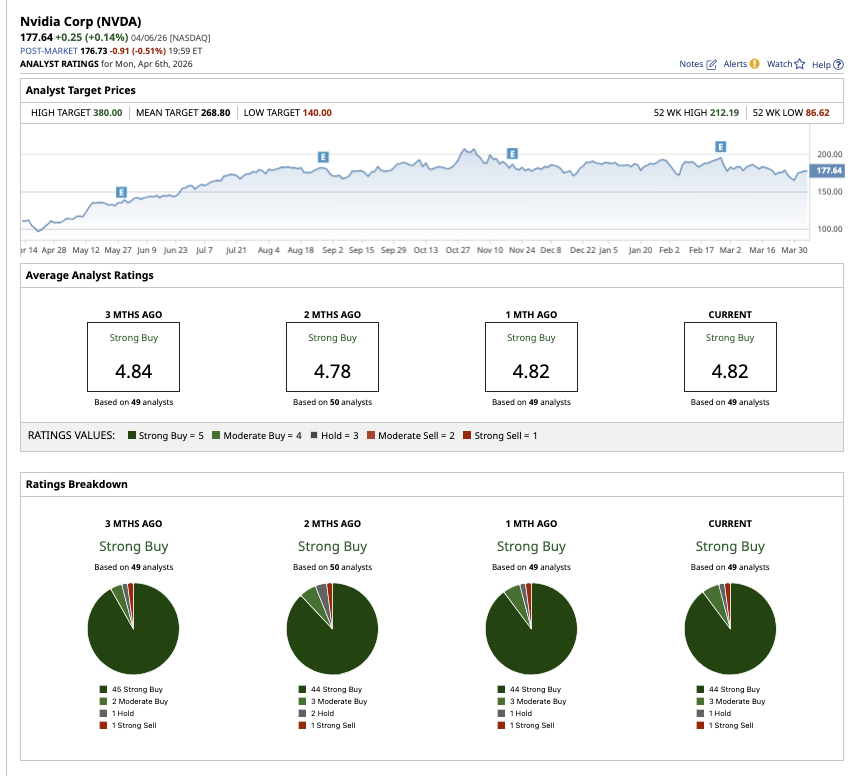

Overall, NVDA stock remains a “Strong Buy” on Wall Street. Out of the 49 analysts covering the stock, 44 have a “Strong Buy” recommendation, three rate it a “Moderate Buy,” one rates it a “Hold,” and one analyst has a “Strong Sell" rating. The mean target price of $268.80 implies potential upside of 48% from current levels. Plus, the high price estimate of $380 suggests that NVDA stock could rally as much as 109% over the next 12 months.

Intel: A Comeback Play Gaining Credibility

Intel’s turnaround story is increasingly being shaped by AI and its continued dominance in CPUs. Intel stressed that while GPUs get most of the attention, CPUs remain an essential part of AI workloads, particularly as inference demand increases.

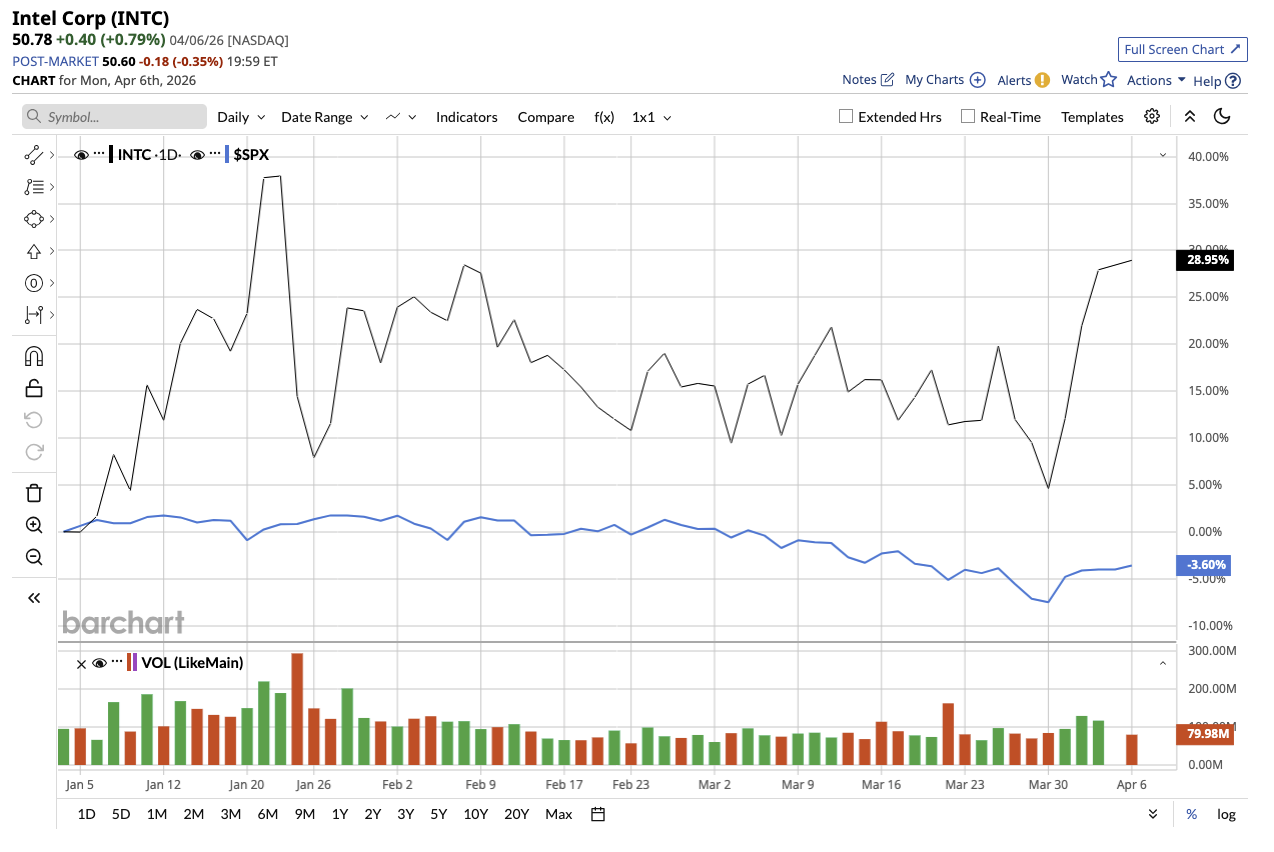

This is probably why investors are starting to pay attention to Intel stock, which has gained 59% YTD.

Intel is also expanding its AI strategy beyond CPUs. The company is developing a broad portfolio that includes AI accelerators, custom ASICs, and integrated solutions that combine CPUs with specialized silicon.

Financially, the company is showing early signs of stabilization. In 2025, revenue remained flat year-over-year (YOY) at $52.9 billion. But the company reported a profit of $0.42 per share over a loss of $0.13 in the previous year.

Intel is also making steady progress on its advanced process technologies, including Intel 18A, which is already in production with improving yields. Management stressed that the firm is now operating in an environment where demand is strong, but execution and supply remain the main challenges.

As Intel rebuilds its business for the AI era, Nvidia has reportedly invested about $7.9 billion in Intel, according to its recent 13F-filing. This partnership also has strategic value as Intel is developing Xeon chips integrated with Nvidia’s NVLink and advancing its 18A manufacturing process. Nvidia’s growing interest in Intel signals rising confidence in its turnaround story.

Intel’s earnings are projected to rise by 17% in fiscal 2026 and 104% in fiscal 2027. Currently, INTC stock is valued at 103 times forward 2026 earnings, reflecting investors’ confidence in its turnaround story. Unlike Nvidia, Intel is a better option for patient and long-term investors. If the company successfully executes its comeback strategy, it has the potential to reemerge as a key player in the semiconductor space. However, investors should also note that Intel’s turnaround is complex and capital-intensive, and progress will take time.

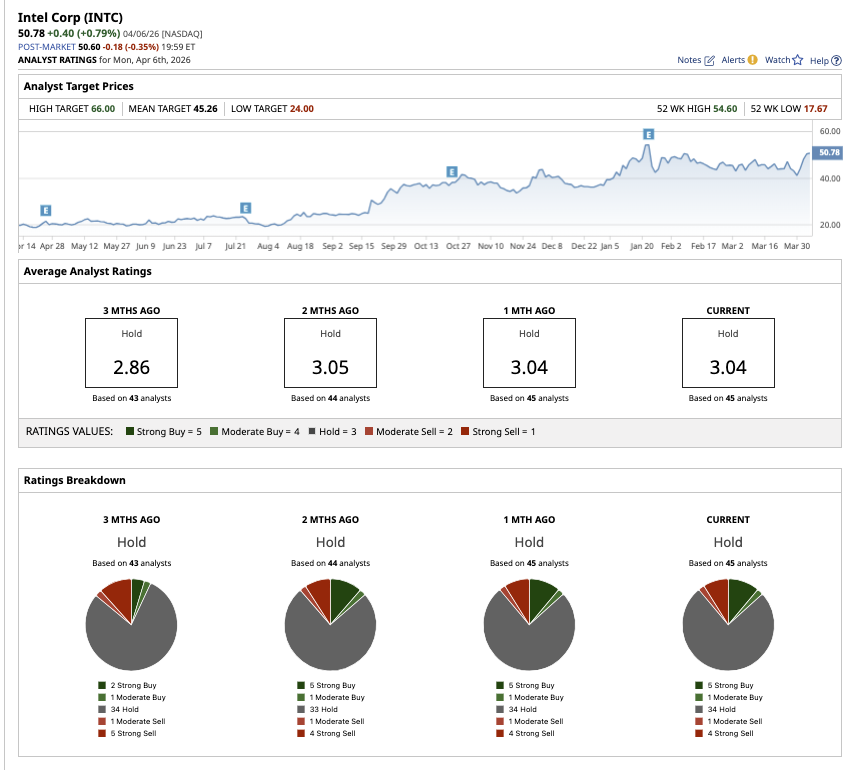

Wall Street believes INTC stock is an overall “Hold.” Of the 45 analysts covering the stock, five rate it a “Strong Buy,” one has a “Moderate Buy” rating, 34 analysts rate it a “Hold,” one analyst has a “Moderate Sell,” and four suggest a “Strong Sell" rating. INTC stock has surpassed its average target price of $45.26. However, the Street-high estimate of $66 suggests INTC stock has potential upside of 13% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)