/Intel%20Corp_%20logo%20on%20mobile%20phone-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

When Nvidia (NVDA) expresses interest in any company, investors should pay attention. According to a recent 13F-filing, Nvidia has invested a hefty amount of around $7.9 billion in Intel (INTC), now holding 214,776,632 shares of INTC stock.

The timing is not random. Intel has been in the spotlight as it rebuilds its foundation for the artificial intelligence (AI) age. This investment signals Nvidia's confidence in Intel's comeback story.

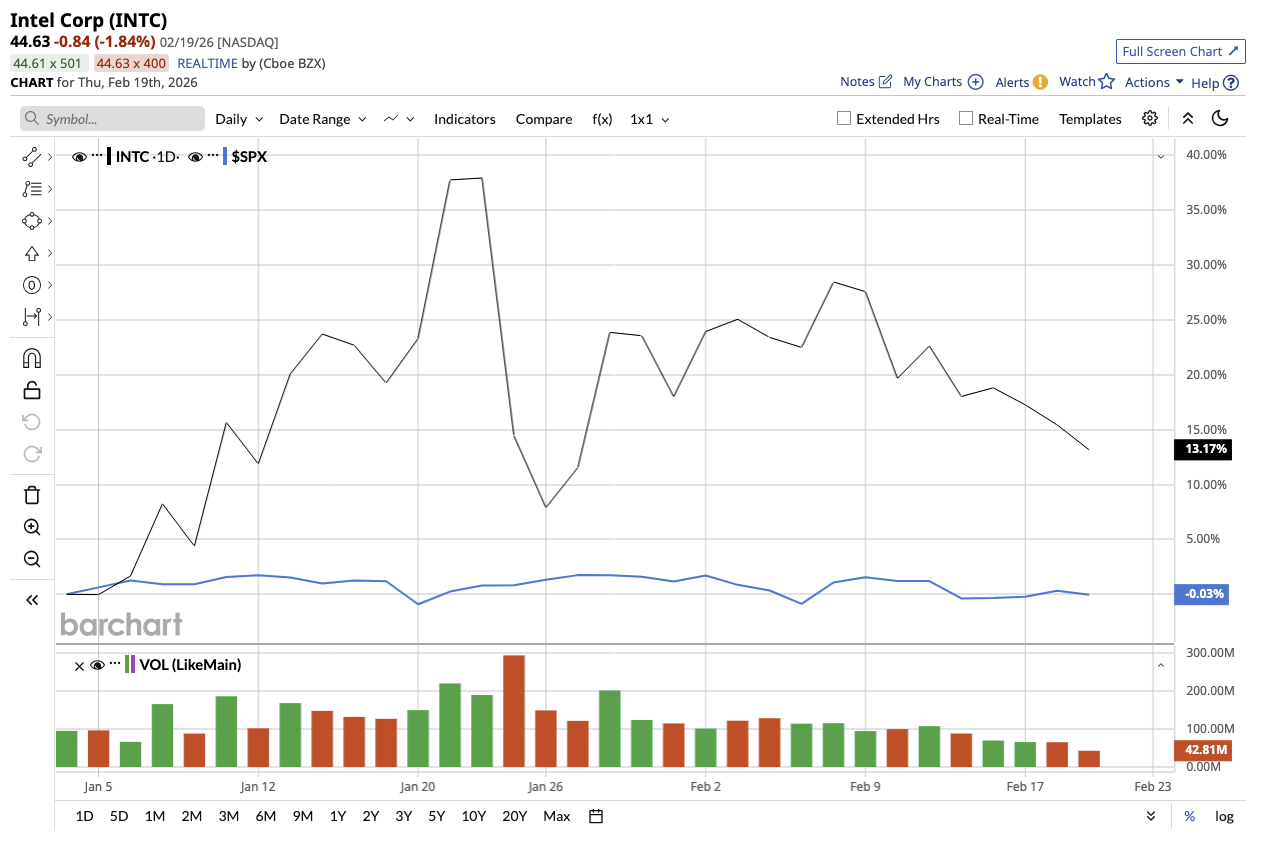

INTC stock is up 21% so far this year, outperforming the S&P 500 Index ($SPX). Should you grab INTC stock now?

A Company in the Middle of a Turnaround

Valued at $227 billion, Intel designs and manufactures semiconductor chips that power PCs, data centers, and AI systems. During the fourth-quarter earnings call, management emphasized that Intel’s biggest issue is constrained supply and not weak demand. Intel saw strong demand across client computing, data centers, AI infrastructure, custom silicon, and networking. The company reported $52.9 billion in total revenue in 2025, flat year-over-year (YOY). However, the firm also reported a profit of $0.42 per share, compared to a loss of $0.13 in 2024.

For Nvidia, which relies on CPUs as host processors in AI systems, deeper integration with Intel strengthens its ecosystem positioning. This is especially relevant now that Intel is building a custom Xeon that is fully integrated with Nvidia's NVLink technology. Another strategic asset Intel brings to the table is the ability to deploy devices based on Intel 18A, the most sophisticated semiconductor process created and manufactured in the United States. Nvidia relies heavily on external foundry capacity. Thus, having a strategic ownership in a U.S.-based advanced manufacturing partner provides Nvidia with supplier diversity, risk mitigation, and greater manufacturing control, giving it a competitive advantage.

Furthermore, Intel is not seeking short-term aggressive growth. Instead, the company is focusing on stabilizing yields, improving wafer starts across current nodes, keeping a tight capital allocation, and delaying spending on 14A nodes until customers commit. These strategic moves are likely why Nvidia chose Intel, as it reveals it could prove to be a stable and reliable long-term partner in advanced manufacturing and AI infrastructure.

Intel’s balance sheet has also strengthened, thanks to strategic investments from Nvidia and SoftBank (SFTBY), government funding, and monetized assets involving Mobileye and Altera. Intel repaid $3.7 billion in debt and ended the year with $37.4 billion in cash and short-term investments.

Analysts expect significant earnings recovery in the next two years, with earnings projected to rise by 15% in fiscal 2026 and 105% in fiscal 2027. INTC stock is trading at a premium of roughly 45 times forward 2027 earnings, reflecting investors’ confidence in its rebound story that AI-driven growth will boost profits. Heading into 2026, Intel is showing revenue stability, profit recovery, improving free cash flow, strong liquidity, controlled capital spending, and strong AI-related demand across segments. In short, Nvidia’s investment signals confidence in Intel’s long-term relevance in the AI ecosystem.

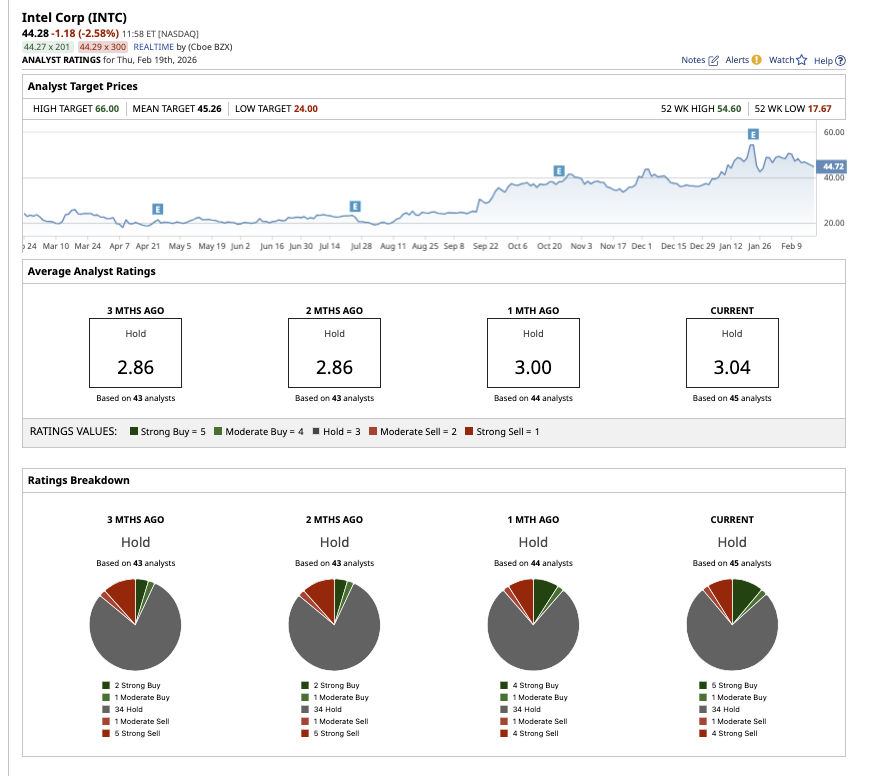

Is INTC Stock a Buy, Hold, or Sell on Wall Street?

Wall Street believes in Intel’s turnaround story as much as Nvidia and has allotted an overall “Hold" rating. Of the 45 analysts covering the stock, five rate it a “Strong Buy,” one has a “Moderate Buy” rating, 34 rate it a “Hold,” one analyst has a “Moderate Sell,” and four suggest a “Strong Sell" rating. As of this writing, INTC stock is trading close to its average target price of $45.26. However, the Street-high estimate of $66 suggests the stock has potential upside of 48% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)