/Super%20Micro%20Computer%20Inc%20HQ%20photo-by%20Tada%20Images%20via%20Shutterstock.jpg)

Super Micro Computer (SMCI) once rode the artificial intelligence (AI) boom like a market darling, cementing its role as a critical infrastructure provider for the data center buildout powering this generational shift. But the company that soared on its AI ambitions is now struggling to stay aloft under the weight of its own controversies. And this isn't SMCI's first brush with turbulence. Nearly two years ago, the company took a severe reputational hit when allegations of questionable accounting practices and delays in financial filing rattled investor confidence to its core.

While the company eventually regained some footing by publishing its overdue results, the episode left lasting doubts about its governance. Now, those concerns are resurfacing. A deepening legal and regulatory crisis that erupted in late March has once again sent investor confidence into a tailspin, raising uncomfortable questions about whether SMCI's governance problems are a pattern rather than a chapter. Moreover, Wall Street is starting to take notice.

Recently, analysts at Mizuho adopted a more cautious stance, downgrading SMCI to “Neutral” and cutting its price target from $33 to $25. At the same time, the investment firm shifted preference toward rival Dell Technologies (DELL), assigning it an “Outperform” rating, highlighting a potential change in leadership in the AI server race. So, with uncertainty hanging over SMCI and rivals closing in, what’s the smartest way for investors to approach the stock right now?

About Super Micro Stock

Headquartered in San Jose, California, Super Micro Computer has built its business around delivering highly customized, application-optimized IT infrastructure solutions for a rapidly evolving digital landscape. The company primarily serves enterprise, cloud, and artificial intelligence markets, while also expanding into emerging areas such as 5G and edge computing. Its broad portfolio includes servers, storage systems, AI platforms, IoT solutions, networking equipment, software, and related support services.

At the core of its strategy is a modular “Server Building Block Solutions” architecture, designed to give customers flexibility in configuring systems based on specific workload requirements. This approach allows seamless customization across processors, memory, GPUs, storage, networking, and cooling technologies, including both air and liquid cooling, making its solutions adaptable to a wide range of performance needs.

Supporting this flexibility is Super Micro’s vertically integrated operating model, with in-house design and manufacturing capabilities spanning the United States, Taiwan, and the Netherlands. By maintaining control over key components such as motherboards, power systems, and chassis, the company enhances efficiency, accelerates time-to-market, and preserves quality across its product stack. The company currently carries a market capitalization of approximately $13.2 billion.

Even with its strong positioning in AI-driven infrastructure, Super Micro has found itself under relentless selling pressure. Regulatory overhangs have increasingly taken center stage, eroding investor confidence and clouding the company’s otherwise compelling growth story. Last month, co-founder Yih-Shyan Wally Liaw, along with a company employee and a contractor, has been charged with allegedly smuggling restricted, advanced AI servers powered by Nvidia (NVDA) into China.

According to prosecutors, the scheme involved deliberately removing identifying labels and serial numbers and replacing them with dummy units to evade export controls. Authorities claim these shipments generated billions of dollars in revenue over the past few years, underscoring both the scale and the severity of the accusations.

And the impact of this news is clearly visible in the stock price. After a 31.3% decline in 2025, shares have taken another 22.55% hit so far in 2026. On the other hand, the broader S&P 500 Index ($SPX) has remained comparatively steady, rising 30.7% over the past year and slipping just 3.34% in 2026, underscoring Super Micro's sharp divergence due to company-specific challenges.

SMCI’s Blockbuster Revenue Growth Overshadowed by Shrinking Margins

Super Micro kicked off fiscal 2026 with a blockbuster second-quarter report on Feb. 3, delivering eye-popping revenue growth, but with clear cracks forming beneath the surface. The server maker posted revenue of $12.7 billion, a staggering 123% year-over-year (YOY) surge fueled by relentless demand for AI-optimized server racks and data center infrastructure, which now contribute more than 90% of its total business.

Notably, this figure also blew past Wall Street’s $10.44 billion revenue estimate. But while the top line dazzled, profitability told a more pressured story. Gross margins compressed sharply to 6.4%, down from 9.5% in the prior quarter and 11.8% a year ago, underscoring aggressive pricing as SMCI fights to defend market share against rivals like Dell (DELL) and Hewlett-Packard Enterprise (HPE) .

Even so, earnings held up better than expected. Non-GAAP EPS came in at $0.69, up 17% YOY and comfortably ahead of the Street’s $0.49 forecast. However, cash flow raised a red flag, with operating cash flow slipping into negative territory at $24 million, down sharply from $894 million in the previous quarter and $216 million in the same period last year.

On the balance sheet, Super Micro reported $4.1 billion in cash and cash equivalents as of Dec. 31, 2025, against $4.9 billion in total bank debt and convertible notes. Looking ahead, the company expects at least $12.3 billion in fiscal 2026 third-quarter revenue, along with GAAP EPS of at least $0.52 and non-GAAP EPS of at least $0.60. For the full fiscal year, SMCI is targeting revenue of at least $40 billion.

What Do Analysts Think About SMCI Stock?

On Apr. 6, Mizuho lowered its price target on SMCI to $25 from $33 while maintaining a “Neutral” rating, reflecting a more cautious stance despite powerful industry tailwinds. Analysts led by Vijay Rakesh emphasized that AI server demand remains strong, with Nvidia’s data center revenue expected to grow more than 50% YOY through 2027. At the same time, cloud spending continues to surge, with capex projected to reach $689 billion in 2026 and potentially $811 billion in 2027, fueled by the rapid adoption of agentic AI platforms such as Claude and ChatGPT.

Despite these favorable trends, Rakesh and his team noted that SMCI leadership in AI server technology, backed by its agile and innovative execution, could face near-term pressure. Ongoing concerns around reports of former employees diverting Nvidia GPUs to China may weigh on sentiment and create hesitation among customers, potentially redirecting some risk-sensitive orders to competitors like Dell.

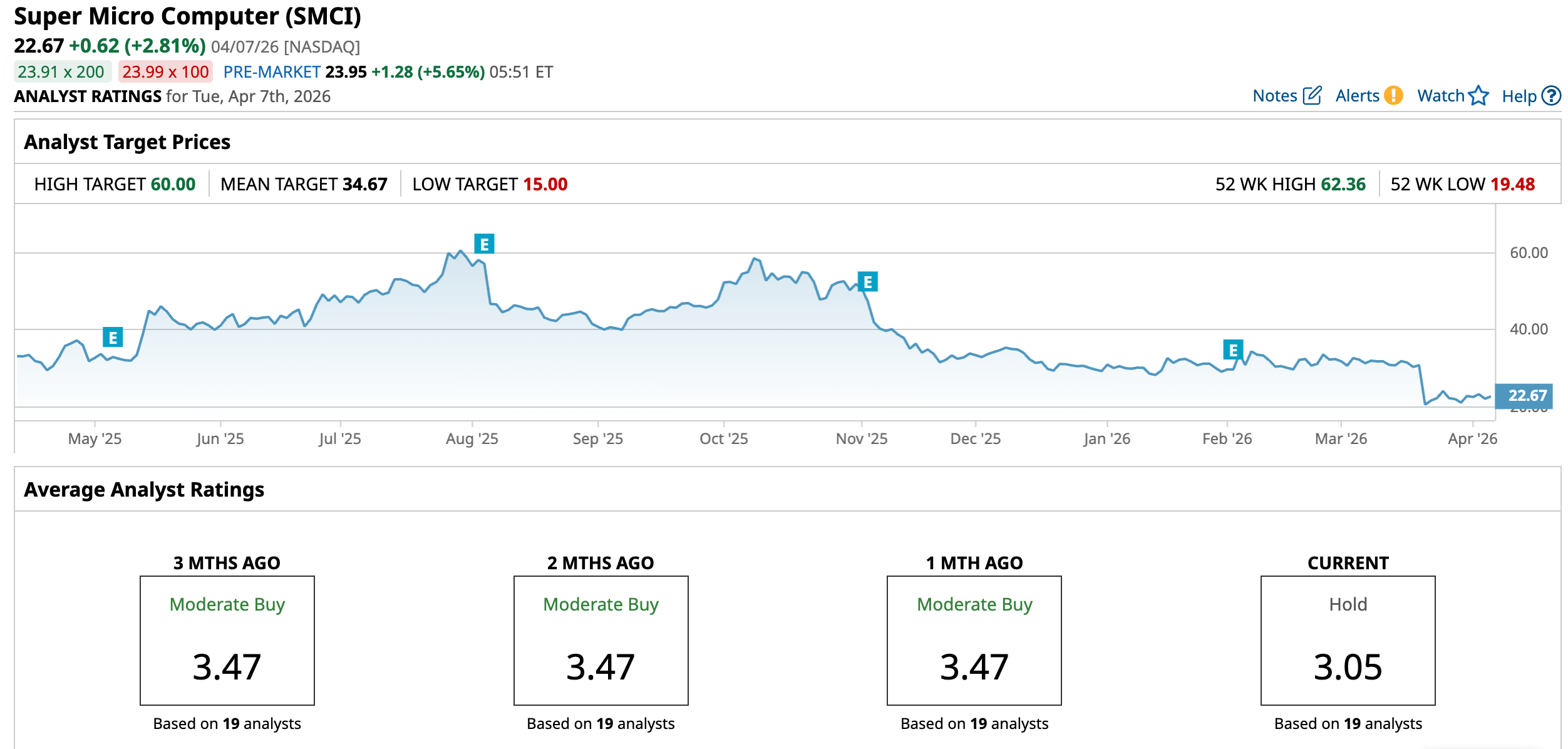

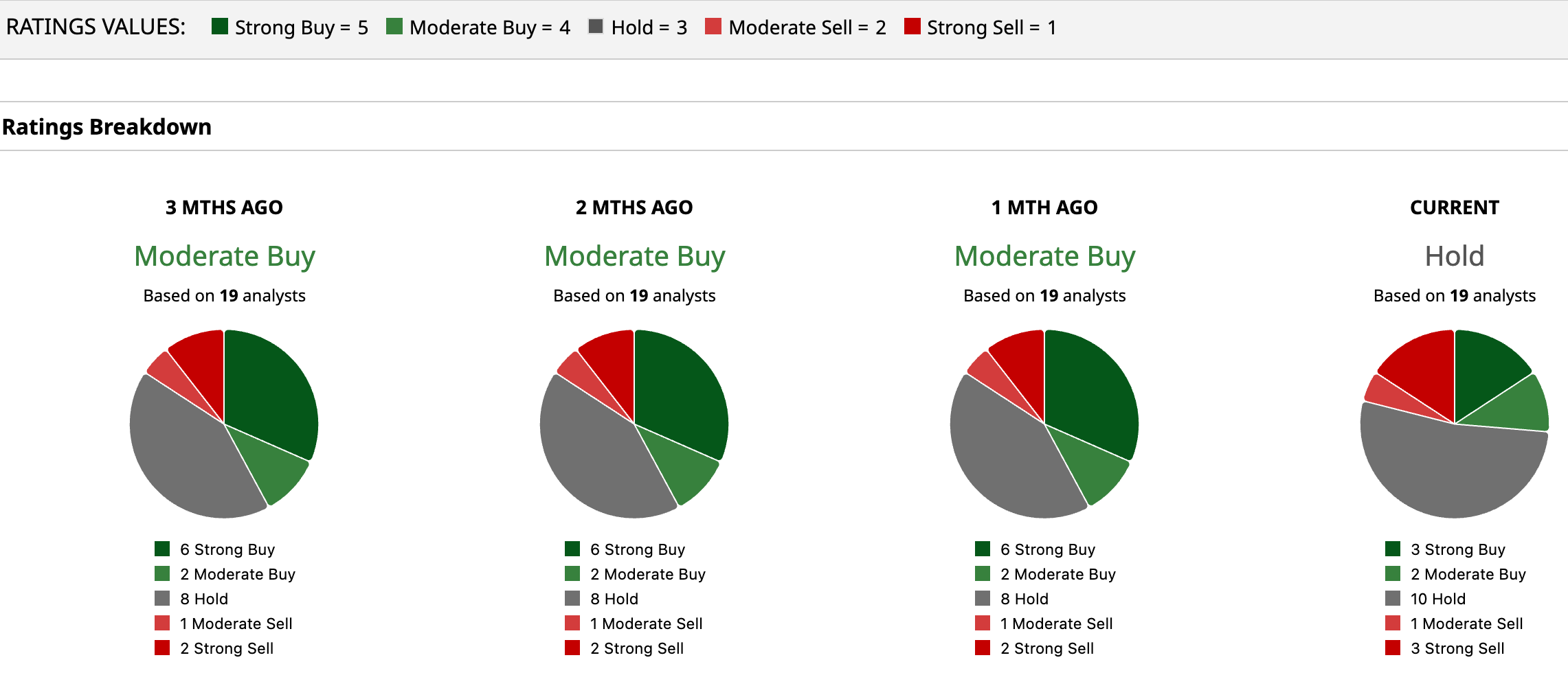

Overall, Wall Street is cautious about Super Micro, with the stock currently carrying a consensus “Hold” rating. Out of 19 analysts covering the name, only three are strongly bullish with “Strong Buy” ratings, while two lean positive with “Moderate Buy.” The majority remain on the sidelines, with 10 analysts rating the stock a “Hold,” while bearish sentiment includes one “Moderate Sell” and three “Strong Sell” recommendations.

Despite the mixed outlook, price targets suggest notable upside potential. The average target of $34.67 implies a possible 52.9% gain from current levels, indicating room for recovery if sentiment improves. At the upper end, the Street-high target of $60 points to a significant 164.7% upside, highlighting the stock’s potential if key concerns begin to ease.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)

/Gen%20Digital%20Inc%20logo%20on%20building-by%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)

/EV%20in%20showroom%20by%20Robert%20Way%20via%20Shutterstock.jpg)