Netflix (NFLX), the streaming giant, has kept evolving, expanding its global reach, doubling down on a relentless content engine, and leaning into ad-supported offerings. Netflix’s edge still comes down to one thing – consistently giving audiences a reason to stay.

It’s from this position of strength that the company was set to acquire Warner Bros. Discovery (WBD), aiming to add a deep vault of iconic stories to its arsenal. But the script flipped. When Paramount Skydance Corporation (PSKY) came in with a stronger bid, Netflix chose to walk away, collecting a sizable breakup fee while avoiding the weight of debt and the complexity that comes with integrating legacy media businesses.

That decision, while surprising on the surface, may have sharpened Netflix’s focus. Instead of chasing scale for its own sake, the company can now double down on its digital-first model, investing in content, expanding its advertising engine, and steadily returning capital to shareholders.

That’s why Goldman Sachs sees a more favorable risk-reward setup ahead, with analyst Eric Sheridan pointing to steady growth, improving profitability, and a clearer execution story. It suggests that while Netflix may have stepped back from one battle, it is positioning itself to win the larger war, making the stock a compelling buy now.

About Netflix Stock

Netflix started out as a DVD rental service but has since grown into a global streaming giant based in California, now valued at $417.7 billion by market cap. Over the years, it has reshaped the ways in which people watch entertainment, using smart artificial intelligence (AI)-driven recommendations to keep viewers hooked and coming back for more.

The company has stayed ahead of the curve with smart moves like launching an ad-supported tier and cracking down on password sharing, while also expanding into live events, from NFL games to comedy specials. Today, Netflix offers everything from series and films to documentaries and games across more than 190 countries, serving roughly 325 million paid subscribers. By consistently investing in and producing original content at scale, Netflix has not only disrupted traditional media but also built a strong, global platform that continues to define the future of entertainment.

The mega-cap streamer’s shares have been moving through an interesting phase – part strength, part reset. Over the past 52 weeks, shares are up a solid 13.87%, reflecting confidence in its subscription growth and steady revenue engine. But that strength comes with context. The stock is still down about 26% from its high of $134.12, indicating sentiments cooling since then.

In the last six months, NFLX slipped roughly 17%, even as the broader story remained intact. Yet, momentum has started to turn. The stock is up 8.92% over the past three months and nearly 6.29% in just the past five days, hinting at a recovery from oversold levels in February, especially after recent price hike announcements.

A key turning point came when Netflix walked away from acquiring Warner Bros. Discovery, ending the bidding war with Paramount Skydance. The market clearly welcomed the move, pushing shares higher.

Technically, too, strength is building, with the 14-day RSI hovering around 65.31, suggesting growing bullish momentum as investor confidence slowly returns.

Netflix’s shares do not come cheap, priced at 31.11 times forward adjusted earnings and 8.15 times sales. But that premium looks justified. With strong bets on content, ads, live events, and gaming, Netflix is building multiple growth engines. As these bets start paying off, the rich valuation is slowly turning skeptics into believers.

Netflix Beats Q4 Earnings

Netflix wrapped up its fourth quarter of fiscal 2025 with a steady beat, showing that its growth engine is still running well. Revenue rose 17.6% year-over-year (YOY) to $12.05 billion, coming in ahead of expectations, driven by a mix of subscriber additions, pricing moves, and a strong push in advertising.

On the earnings side, the momentum was just as clear. Operating income jumped 30.1% annually to around $3 billion, while net income grew 29.4% YOY to $2.4 billion. EPS rose 31% YOY to $0.56, slightly ahead of estimates.

Advertising continued to stand out as a key driver. The company generated over $1.5 billion in ad revenue in 2025, more than 2.5 times the previous year. Strong ad demand even helped offset foreign exchange headwinds, pushing Q4 revenue above guidance.

Also, cash generation improved, with free cash flow in Q4 rising 35.8% annually to $1.9 billion, and for fiscal 2025 it amounted to $9.5 billion. Meanwhile, engagement remained stable, with users watching 96 billion hours of content in the second half of 2025, up 2% YOY. Much of this was fueled by stronger traction in its original content, where viewing jumped 9% YOY over the same period.

Looking ahead, management expects fiscal 2026 revenue between $50.7 billion and $51.7 billion, implying 12% to 14% annual growth, with advertising revenue set to roughly double again. Revenue for the first quarter of fiscal 2026 is projected to be around $12.16 billion, with EPS expected to be $0.76.

Netflix changed entertainment when it moved into streaming, and despite rising competition, it has kept delivering value. Its biggest edge remains strong content. Its biggest edge remains its strong content library. Building on that, Netflix is now raising subscription prices across different plans, aiming to reinvest in better content and user experience.

With Netflix gearing up to drop its Q1 earnings report for fiscal 2026 on Thursday, April 16, investors won’t have to wait much longer to see whether its current strategy is delivering results. Wall Street is watching closely, expecting Q1 revenue to hit $12.17 billion, while EPS is forecasted to rise 15.2% YOY to $0.76.

Looking further ahead, fiscal 2026 EPS is anticipated to grow by 25.3% to $3.17, with the bottom line for fiscal 2027 projected to reach $3.86 per share, up 21.8%. If these numbers play out, Netflix might just be scripting a blockbuster run beyond the charts.

What Do Analysts Expect for Netflix Stock?

Stepping back from the deal drama, Goldman Sachs’ Eric Sheridan turns optimistic on Netflix. Sheridan sees the company entering a steady growth phase, projecting double-digit revenue expansion over the next three to four years. A key driver here is the company’s advertising business, which the analyst expects to scale meaningfully, reaching around $9.5 billion by 2030. Alongside that, periodic subscription price hikes should continue to support top line momentum without derailing demand.

On the profitability front, the outlook looks just as solid. Sheridan estimates about 250 basis points of annual GAAP operating margin expansion over the next three years, driven by disciplined cost management and more measured content spending.

Then comes the shareholder angle. With the Warner pursuit behind it, Netflix is now in a position to return meaningful capital, potentially 20% to 25% of its market cap over the next five years. Putting it all together – growth, margins, and cash returns – Sheridan anticipates a clearer, stronger path ahead, backing NFLX with a “Buy” rating and a price target of $120, which implies an upside potential of 21.3%.

Beyond Goldman Sachs, the broader Wall Street view on NFLX is cautiously optimistic. Bank of America’s Jessica Reif Ehrlich believes Netflix is simply returning to “business as usual,” focusing on organic growth, steady content investment, and scaling its advertising arm. The analyst anticipates NFLX being driven by consistent subscriber gains, improving earnings, and a long runway in ads and live content. The analyst maintains a “Buy” rating with a $125 price target.

Netflix’s recent price hikes, pushing its Premium tier to $26.99 in the U.S., are being viewed as a sign of confidence rather than risk. Ehrlich calls it a validation of Netflix’s pricing power, especially as the platform remains “sticky” even in a shaky macro environment.

Meanwhile, Needham analyst Laura Martin estimates these hikes alone could add $1.7 billion in revenue by 2026, potentially pushing growth beyond its 12% to 14% top line guidance range. She also highlights early bets on generative AI as a quiet margin booster. Even newer formats are gaining traction. KeyBanc Capital Markets analyst Brandon Nispel points to rising interest in video podcasts, reinforcing Netflix’s position as a service users are least likely to cancel.

Still, not everything is smooth sailing. Questions around engagement trends, AI’s long-term impact on content, and a slight dip in global penetration suggest that while the story is strong, a few chapters are still unfolding.

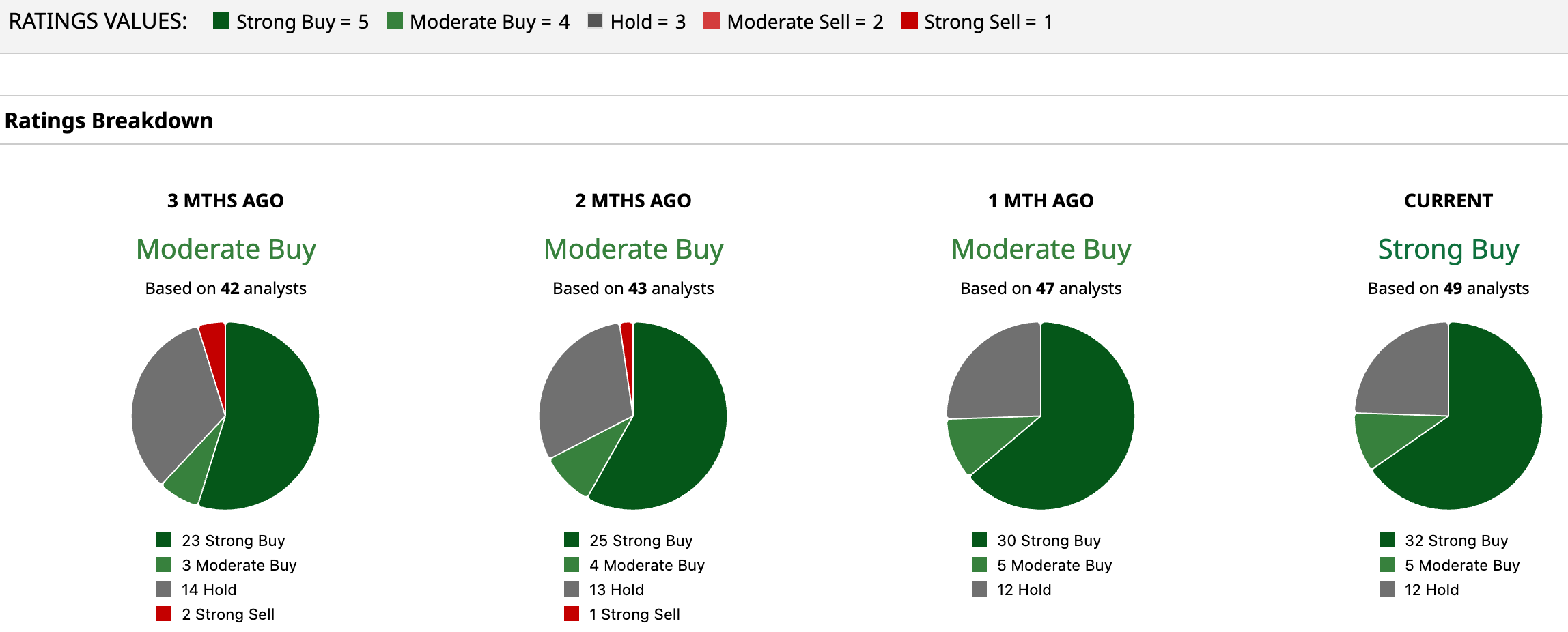

Overall, Wall Street is leaning bullish on NFLX, giving a consensus “Strong Buy” rating. Of the 49 analysts rating the stock, a majority of 32 analysts have recommended a “Strong Buy,” five suggest a “Moderate Buy,” and the remaining 12 analysts have a “Hold” rating.

Meanwhile, the stock has a mean price target of $114.86, which suggests upside potential of 16.23% from the current price levels. Meanwhile, the Street-high target of $137 implies the streaming giant’s stock could rise as much as 38.6%.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)