Walmart (WMT) is one of the world’s largest retailers by revenue, The company has evolved from a discount "big-box" store into a sophisticated omnichannel ecosystem. Operating through Walmart U.S., Walmart International, and Sam’s Club, the firm serves more than 250 million customers weekly. Walmart has also undergone a digital transformation, integrating AI-driven logistics, a robust e-commerce marketplace, and a high-margin advertising business via Walmart Connect.

Walmart has a remained a steady force in the retail space. Most recently, though, analysts are wondering how new price hikes at Sam's Club stores will affect shares of WMT stock. Let's take a closer look.

About Walmart Stock

WMT stock currently reflects a strong one-year gain of approximately 45%, with Walmart reaching a market capitalization of $1 trillion, a milestone driven by the market's recognition of its margin expansion and tech-driven growth. Recently, though, shares have seen minor consolidation due to the premium valuation.

In comparison to the S&P 500 Consumer Staples Index ($SRCS), Walmart has been a massive outperformer over the last 12 months. The broader staples index, composed of slower-growing essential goods companies, has gained roughly 8% over the period. Meanwhile, Walmart’s 52-week surge highlights its unique position as a growth-oriented retail-tech hybrid.

Walmart's Financial Results

Walmart concluded a historic fiscal 2026 by reporting record fourth-quarter revenue of $190.7 billion, a 5.6% increase year-over-year (YOY). The standout driver was global e-commerce sales, which surged 24%, led by store-fulfilled delivery and a thriving third-party marketplace. Walmart's high-margin global advertising business also grew 46% to $6.4 billion for the full year. Combined with membership fees, these diversified streams now account for about a third of the company's total operating profit.

Walmart reported adjusted EPS of $0.74 for Q4, beating estimates and demonstrating successful expense leverage through automated fulfillment centers. For the full fiscal-year 2026, total revenue reached $713.2 billion, a 4.7% YOY increase that showcased the company's "phygital" dominance. Full-year operating income grew faster than sales, up 5.4% on an adjusted basis, reflecting improved e-commerce economics and a more profitable business mix.

Management signaled continued confidence in the company's transformation by authorizing a new $30 billion share repurchase program. Looking ahead to fiscal 2027, Walmart also issued an optimistic outlook, projecting revenue growth of 3.5% to 4.5% and adjusted EPS between $2.75 and $2.85.

Walmart Hikes Sam's Club Membership Fees

Analysts are currently weighing the impact of the first Sam’s Club membership fee increase since 2022, which is set to begin on May 1, 2026. Annual fees for the basic "Club" tier will rise from $50 to $60, while "Plus" memberships will increase from $110 to $120. To offset the price hikes, Walmart is enhancing benefits, such as raising the annual "Sam’s Cash" reward cap for Plus members to $750.

Jefferies analyst Corey Tarlowe views the move as "structurally positive," noting that higher membership fees carry high incremental margins that boost overall earnings power. Furthermore, the increase is expected to normalize higher pricing across the warehouse sector, potentially benefiting competitors like Costco (COST) and BJ’s Wholesale Club (BJ).

Despite potential near-term renewal headwinds, WMT stock remains a “Buy” favorite with a $145 price target from Jefferies. Defensive positioning has allowed Walmart to outperform broad market averages throughout 2026 as investors prioritize stable, cash-generating retail leaders.

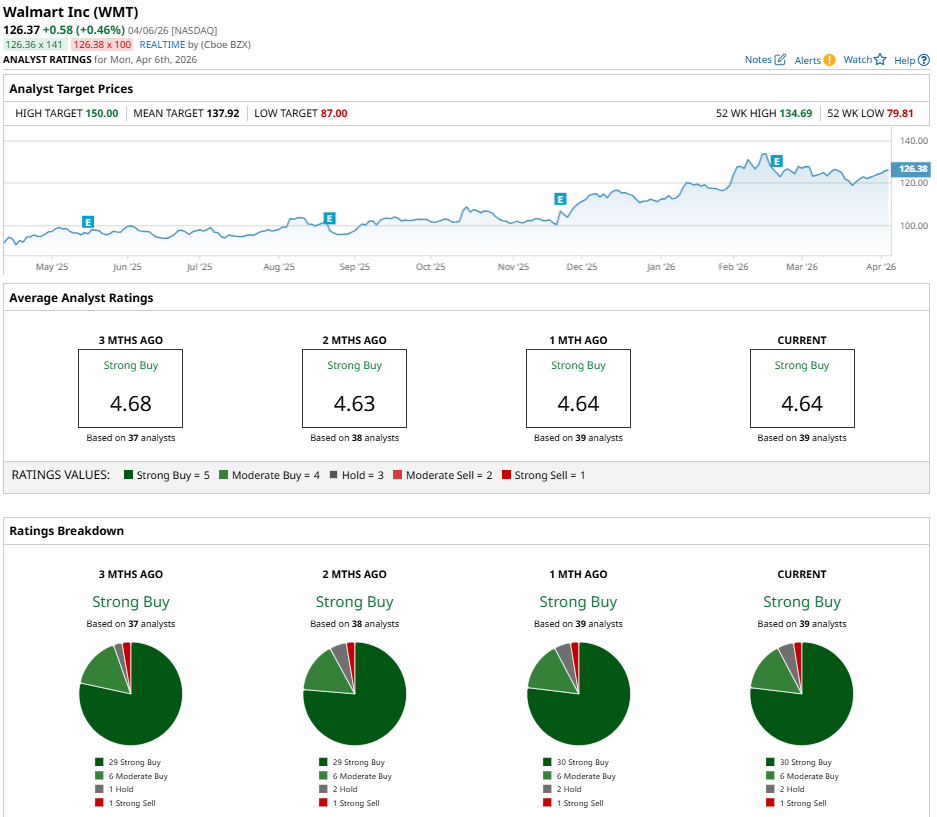

Should You Buy WMT Stock?

Walmart remains a titan of retail stability, bolstered by its recent milestone of becoming a $1 trillion company. WMT stock currently holds a consensus "Strong Buy" rating, based on 30 “Strong Buy” ratings, six “Moderate Buy” ratings, two “Hold” ratings, and one “Strong Sell” rating. The mean price target of $137.92 implies potential upside of nearly 13% from current levels.

Walmart offers a steady growth trajectory supported by its 24% surge in e-commerce in Q4 and its high-margin advertising business. For investors seeking a blend of defensive reliability and tech-driven upside, Walmart’s current valuation represents a premium but justified entry point into the future of automated, omnichannel retail.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)