/Align%20Technology%2C%20Inc_%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

With a market cap of $12.3 billion, Align Technology, Inc. (ALGN) is a global medical device company that develops and markets Invisalign clear aligners, Vivera retainers, and iTero intraoral scanning systems for orthodontic and dental care. It operates through Clear Aligner and Imaging Systems segments, offering advanced digital solutions and treatment options for patients and dental professionals worldwide.

The Tempe, Arizona-based company is expected to unveil its fiscal Q1 2026 results after the market closes on Wednesday, Apr. 29. Ahead of the event, analysts forecast ALGN to post a profit of $1.74 per share, a growth of 14.5% from $1.52 per share in the same quarter last year. It has surpassed Wall Street's bottom-line projections in three of the past four quarters while missing on another occasion.

For fiscal 2026, analysts expect the Invisalign tooth-straightening system maker to report EPS of $9.12, a 7.8% rise from $8.46 in fiscal 2025. Moreover, EPS is anticipated to increase 9.9% year-over-year to $10.02 in fiscal 2027.

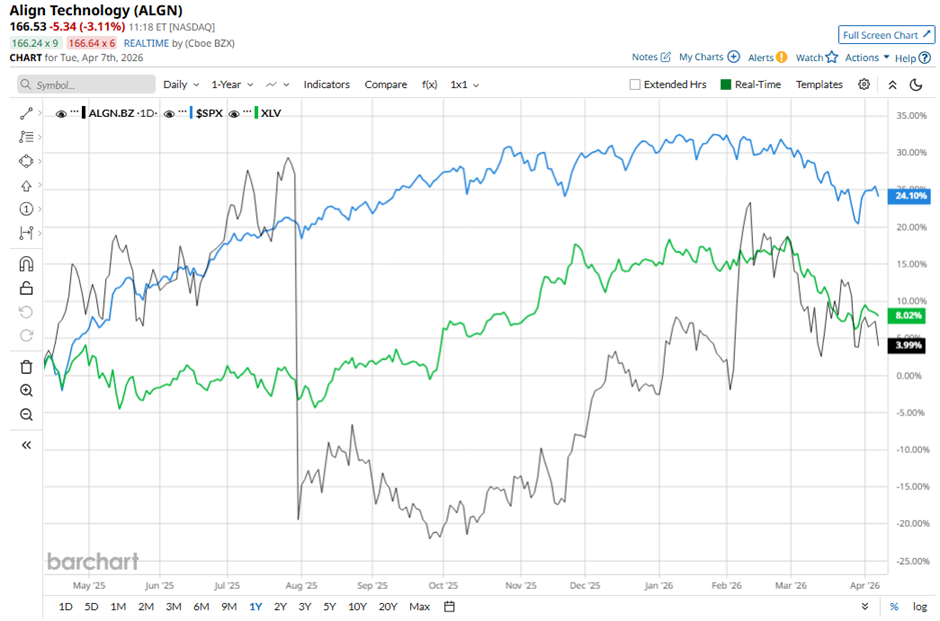

ALGN stock has gained 8.8% over the past 52 weeks, underperforming the broader S&P 500 Index's ($SPX) 29.7% rise. However, the stock has slightly outpaced the State Street Health Care Select Sector SPDR ETF's (XLV) 8.3% return over the same period.

Shares of Align Technology climbed 8.9% following its Q4 2025 results on Feb. 4 as the company delivered record quarterly revenue of $1.05 billion (up 5.3% year-over-year and 5.2% sequentially) along with strong Clear Aligner revenue of $838.1 million (up 5.5%). Investor confidence was further boosted by robust DSO-driven growth (double-digit gains in top accounts) and continued innovation, including the planned 2026 rollout of 3D-printed Invisalign products.

Additionally, management’s outlook supported the rally with Q1 2026 revenue guidance of $1.01 billion - $1.03 billion (up 3% - 5%) and full-year 2026 growth guidance of 3% - 4%.

Analysts' consensus rating on ALGN stock is cautiously optimistic, with a "Moderate Buy" rating overall. Out of 15 analysts covering the stock, opinions include nine "Strong Buys," five "Holds," and one "Moderate Sell." The average analyst price target is $200.15, suggesting a potential upside of 20.2% from current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)