The broader stock market has struggled lately. U.S. stocks finished sharply lower on March 27 as worries about the Iran war pushed oil prices and bond yields higher, with the S&P 500 ($SPX) down 1.7%, the Dow Jones Industrial Average ($DOWI) off by 1.7%, and the Nasdaq Composite ($NASX) lower by 2.1% in a single session.

Real estate investment trusts (REITs) have been caught in that pressure, too. The Vanguard Real Estate ETF (VNQ) — a bellwether fund with more than $34 billion in assets under management — has lost almost 4% over the last five years, with a sizable portion of that drop in just the past month. Even so, JPMorgan Research still expects 6% growth in funds from operations (FFO) for the REIT sector in 2026, a measure that strips out non-cash items to better gauge how well a trust can keep paying its dividend. That outlook is drawing fresh interest back into the group.

Manufactured housing REITs are getting special attention as a steadier corner of the real estate market. On March 31, Mizuho launched coverage on the manufactured housing space with a positive view, naming Equity Lifestyle Properties (ELS) and Sun Communities (SUI) as top choices. Mizuho gave “Outperform” ratings for both names, calling them near-term “winners” among residential REITs that are “viewed as a ‘safe haven’ amid the current volatile macro.”

In a market where most REITs are still trying to regain their footing, what exactly makes these two manufactured housing names worth watching right now? Let’s find out.

REIT #1: Equity LifeStyle Properties (ELS)

Equity LifeStyle Properties (ELS) is a REIT that focuses on manufactured home communities, RV resorts, and campgrounds across the U.S. and Canada, with more than 450 properties in its portfolio. It caters mainly to retirees, long‑term renters, and travelers looking for affordable and flexible places to live or stay.

Over the past year, ELS has shown both strength and some investor caution, down more than 3% over the last 52 weeks but up more than 5% year-to-date (YTD).

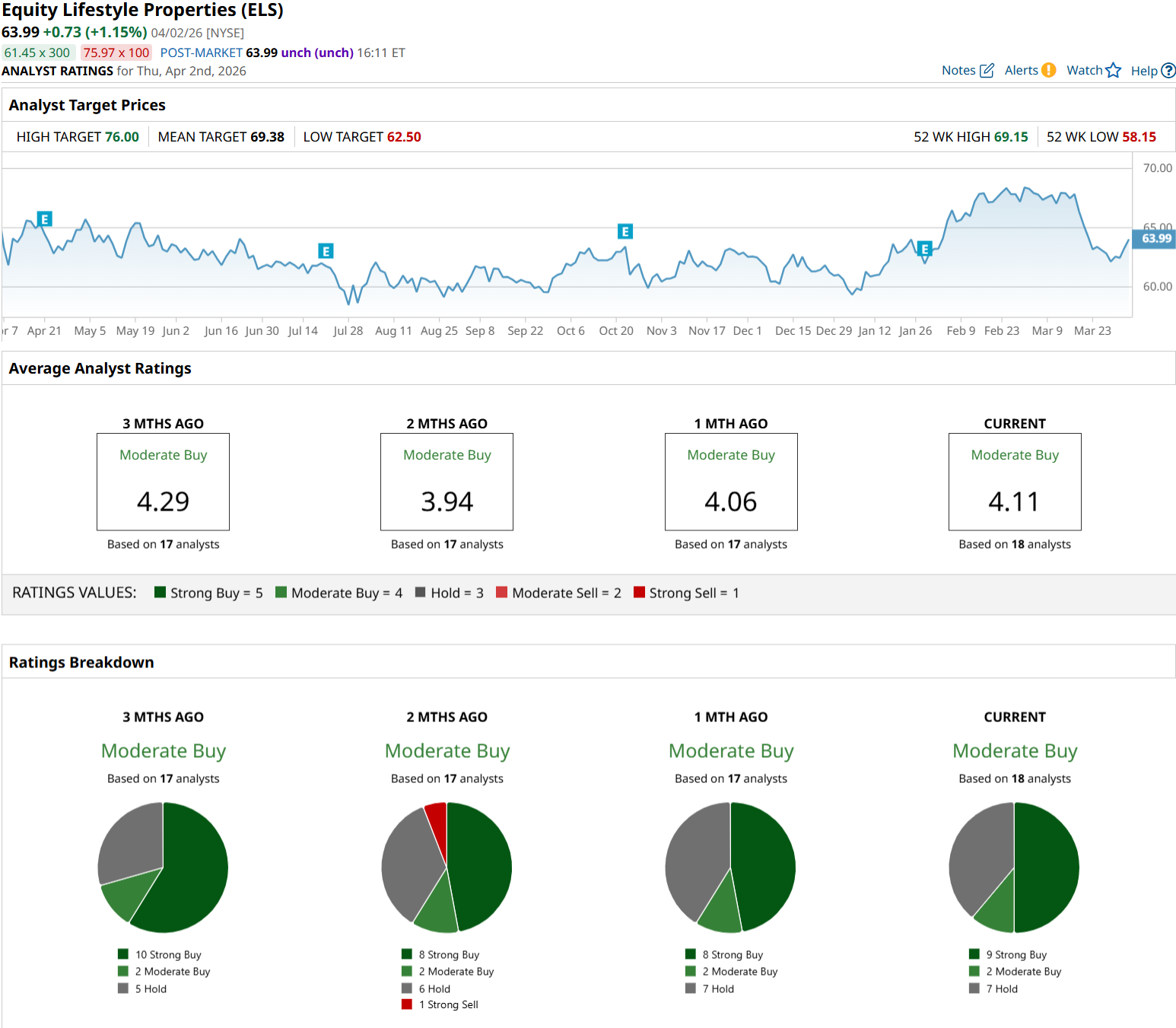

On valuation, ELS trades at a forward price-to-earnings (P/E) multiple of about 19.8 times, below the sector average of 30.6 times. That suggests it is still reasonably priced compared with peers. The 60‑month beta of 0.76 also points to lower volatility.

The dividend yield is around 3.4%, backed by a recent increase to an annual rate of $2.17 per share, marking 22-straight years of dividend growth and highlighting solid, repeatable cash flow.

On the earnings front, Equity LifeStyle Properties delivered a steady fourth quarter, posting funds from operations of $157.6 million, or $0.79 per share, slightly ahead of expectations. For the full year, revenue came in at $1.53 billion while FFO totaled $612.4 million. Management is guiding 2026 FFO in a range of $3.12 to $3.22 per share, pointing to steady growth rather than a step change.

Longer term, the backdrop in affordable housing remains a key support, with manufactured home communities helping absorb some of the pressure from rising housing costs. As that trend builds, Equity LifeStyle's large presence in both manufactured housing and long‑stay RV communities leaves it well placed to capture ongoing demand.

Analysts broadly share that view. Based on 18 analysts with coverage, the consensus sits at a “Moderate Buy" rating. The average price target of $69.38 implies roughly 9% potential upside from current levels.

REIT #2: Sun Communities

Sun Communities (SUI) runs a large network of manufactured housing communities and RV resorts across North America and the United Kingdom, giving it a wide footprint in both long‑term housing and vacation stays. The business sits at the intersection of two key trends: a shortage of affordable housing and growing interest in outdoor “drive‑to” trips.

Even with a tougher market backdrop, SUI has held up reasonably well, up roughly 3% over the past 52 weeks and up 3.5% YTD.

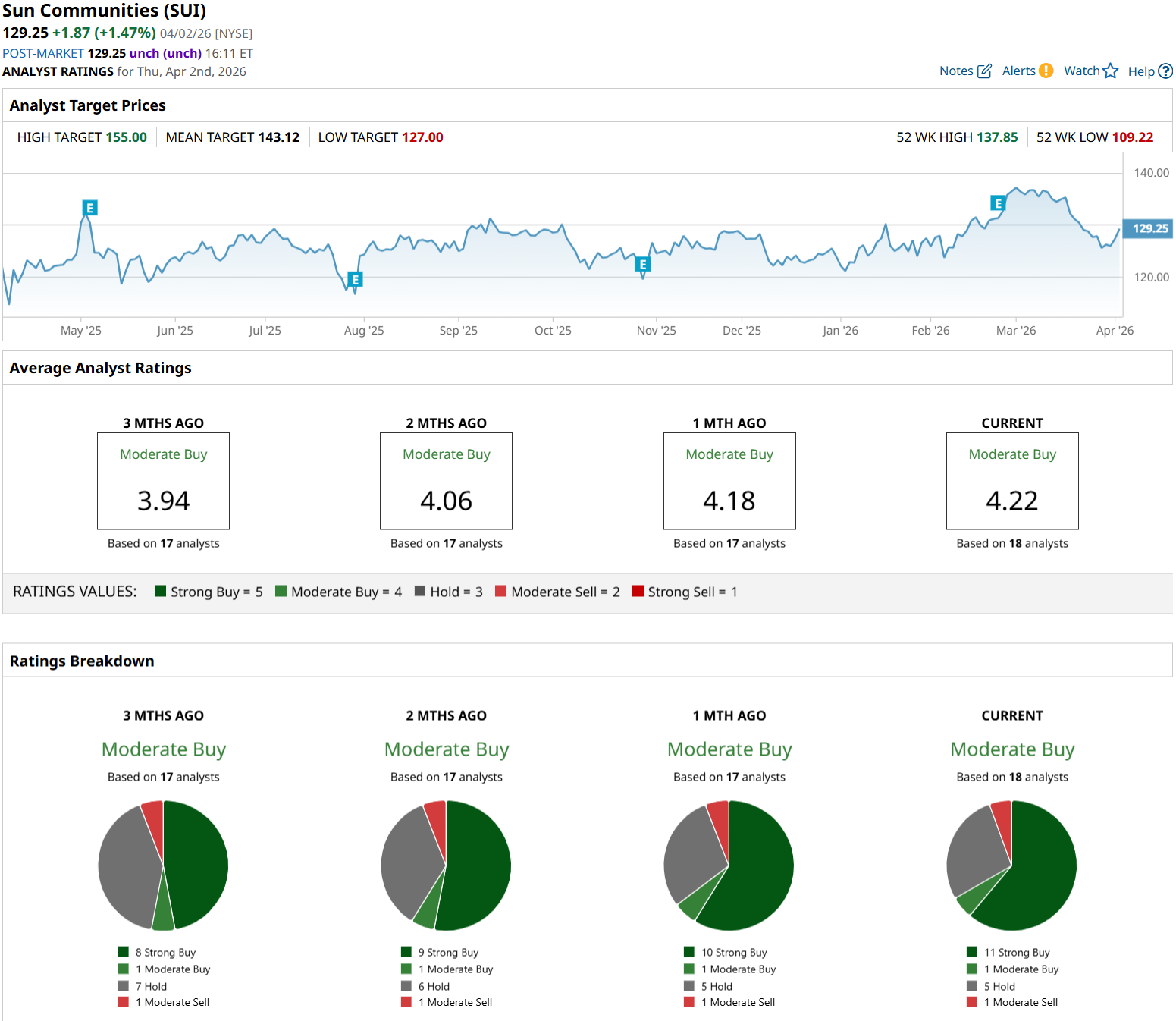

Sun Communities has a market capitalization of about $15.9 billion and trades at a forward P/E of 18.3 times, which is below the sector average. That points to potential upside if the gap closes. Income is also a major part of the story.

SUI has a forward yield of about 3.5% and pays a quarterly dividend of $1.12, backed by eight-straight years of dividend raises that speak to steady cash generation.

Recent numbers support that view. For 2025, Sun reported net income of $0.99 per share for the fourth quarter and $10.84 for the full year. Core FFO came in at $1.40 for Q4 and $6.68 for the year, while North America same‑property NOI rose nearly 8% in Q4. For 2026, management is guiding core FFO to range from $6.83 to $7.03 per share, signaling expectations for continued growth.

One of the biggest moves this year was the sale of Safe Harbor Marinas to Blackstone's (BX) infrastucture segment for $5.65 billion in cash. The deal is expected to generate about $5.5 billion in net proceeds and gives Sun room to pay down debt, return capital to shareholders, and reinvest in its core manufactured housing and RV business. That combination should strengthen the balance sheet and sharpen Sun's focus on higher‑margin assets.

Analysts remain constructive on the name. Based on 18 analysts, SUI has a consensus “Moderate Buy” rating. The average price target of $143.12 implies roughly 12% potential upside from here.

Conclusion

All told, both Equity LifeStyle Properties and Sun Communities look set to weather current market turbulence better than most. Their exposure to steady, need‑based demand for affordable housing and leisure adds a layer of defense that’s increasingly valuable as rate volatility and inflation bite into other parts of real estate. With fundamentals pointing upward and analysts leaning positive, ELS and SUI seem likely to grind higher through 2026 as investors start rotating toward stable, income‑producing assets.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)