March was a wake-up call for the market. But not only because stock and bond prices fell. It was a reminder to ETF investors in particular that you’d better know what you own.

So in the spirit of Passover, the Jewish holiday that starts this week, and the traditional Seder meal that commemorates freedom from slavery during biblical times, I am supplying four questions I think are critical for ETF holders to ask themselves. For those unfamiliar with Passover, the four questions are a basic discussion of why that particular night is treated differently than others.

That ties directly to what I see as an overarching investment theme in 2026. That this market environment is different from all others. At least all others I’ve seen since entering the business in 1986.

Buying an ETF is no longer just about picking a ticker. Successful, disciplined investors audit the structural integrity of a basket of stocks or other assets. Why? Because we are dealing with an increasingly crowded and correlated market. So before you commit capital, look past the name and ask these four specific questions to ensure you aren’t walking into a trap.

1. What is the ETF’s actual overlap with my current core holdings?

The biggest risk for the modern investor is the illusion of diversification. As I’ve written about here, we have seen with the top tech-focused ETFs that many funds that appear different on the surface are actually 90%-100% identical. That’s because they are anchored by the same mega-cap stocks.

If you add a new sector or thematic ETF to a portfolio that already holds a broad index ETF like SPY, you may simply be doubling your concentration in a few names rather than adding a new return driver. You must ask: Am I buying a new asset class, or am I just buying the same product in a slightly different shade?

2. What is the true total cost of ownership beyond the expense ratio?

The headline expense ratio is only the starting point. In a volatile market like 2026, hidden costs such as the bid-ask spread and tracking error can significantly erode your returns. If an ETF is thinly traded, you might lose 0.50% just entering and exiting the position, which can wipe out months of gains. Additionally, it helps to check the tracking difference. That is, if the ETF consistently underperforms its benchmark by more than its expense ratio, it suggests poor management execution or high internal transaction costs that are being passed on to you.

3. How liquid are the underlying assets in a stress scenario?

An ETF is only as liquid as the stuff it holds inside. This became a critical lesson during last month’s energy shock in the Strait of Hormuz. While the ETF itself might trade millions of shares a day, if it holds illiquid small-cap stocks or exotic bonds, the “authorized participants” who create the basket of stocks to deliver that ETF trade may struggle to create or redeem shares during a panic. This can lead to the ETF trading at a significant discount to its net asset value (NAV), meaning you could be forced to sell for much less than the underlying assets are actually worth.

4. Is this a core building block or a tactical satellite?

You must define the mission of the ETF before it enters your portfolio. A core building block should be low-cost, broad-based, and held for years to capture the beta of the market. A tactical satellite, like a semiconductor fund (SOXX) or gold mining ETF (GDX), is designed to capture a specific move or hedge a specific risk. If you treat a high-fee, high-volatility satellite fund as a core holding, you are exposing your long-term wealth to unnecessary decay and sequence-of-returns risk.

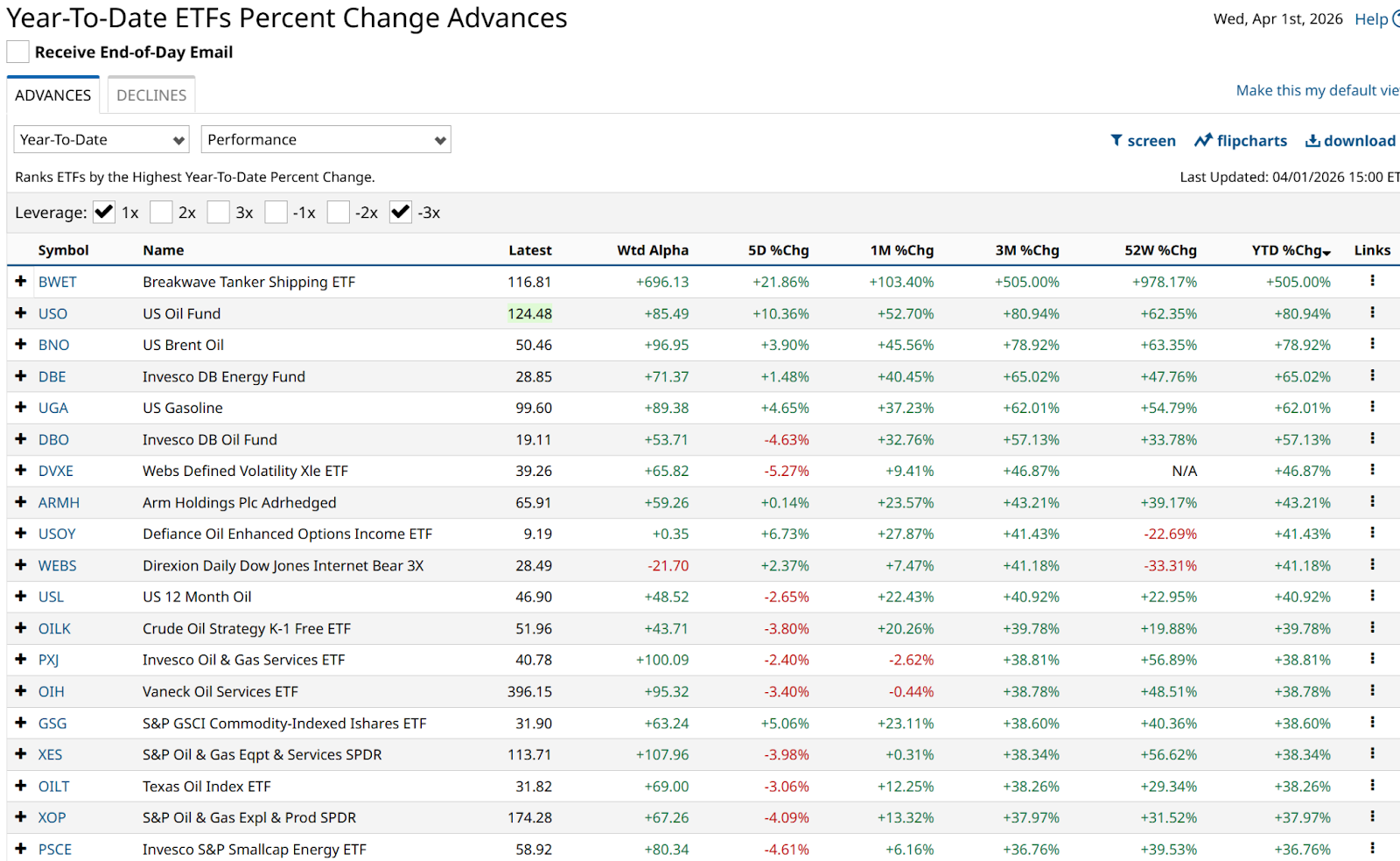

Here’s a look at non-leveraged ETF performance leaders year to date. Do you see what I see? Energy this and energy that. Sure, there are different levels of positive performance in that rightmost column. But that is just a volatility difference between those ETFs. They all have the same engine, or brain, if you will.

This is important at the individual ETF level, but also at the total portfolio level. And increasingly, I firmly believe that portfolio creation, allocation, and rotation among assets over time will provide significant performance advantages, over those who simply buy something because it sounds good. Ironically, the markets have not distinguished between those two ends of the investor spectrum for a long time. But I think that it is changing.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob's written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)