/Micron%20Technology%20Inc_logo%20and%20website-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)

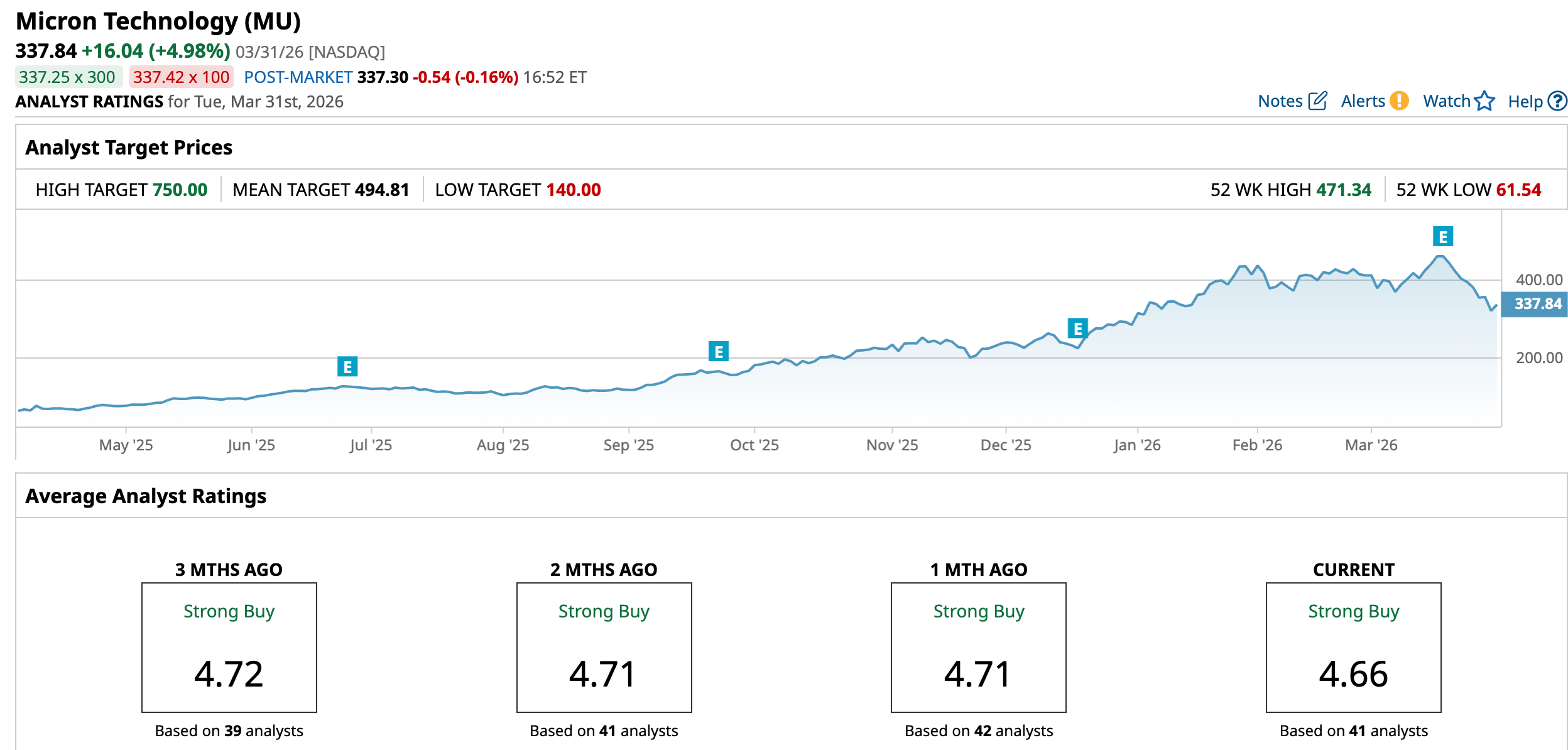

Micron (MU) stock has been under sustained pressure since the company released its second-quarter fiscal 2026 financial results. Shares have fallen 28% from their all-time high of $471.34, reflecting investor concerns that emerged following the earnings announcement. The primary reason for the decline has been the company’s updated capital expenditure outlook, which signaled a significant increase in spending.

Micron now expects fiscal 2026 capital expenditures to exceed $25 billion, well above its earlier estimate of $20 billion. This larger investment plan has raised concerns about potential margin compression and earnings growth in the coming years.

Additional uncertainty has stemmed from Alphabet’s recently introduced TurboQuant, a technology designed to reduce memory requirements in AI models. Because Micron’s growth is driven by the expansion of AI infrastructure, the prospect of more memory-efficient AI architectures has weighed on investor sentiment toward the stock.

In recent years, Micron’s share price has benefited significantly from the rapid buildout of AI data centers, where advanced memory solutions are essential for supporting compute-intensive workloads. High-performance memory is critical to enabling large-scale AI training and inference, positioning Micron as a key supplier in the AI value chain. However, innovations that improve algorithmic efficiency could represent a structural shift. If AI systems increasingly require less memory to achieve similar levels of performance, the long-term growth trajectory for memory demand could moderate.

Should You Buy Micron Stock Now?

Despite these concerns, Micron’s near-term fundamentals remain relatively strong. Demand for memory products related to AI infrastructure continues to expand, while industry-wide supply constraints are supporting pricing. These dynamics are expected to drive solid financial performance in the near term. In particular, margin expansion driven by favorable supply-demand conditions could continue to support earnings growth and could lead to a recovery in MU stock. In addition, its relatively modest valuation further suggests potential upside.

Supporting Micron’s favorable outlook are the advancements in AI systems, which are memory-intensive. This structural shift positions Micron as a major beneficiary within the AI ecosystem.

Furthermore, management’s upbeat commentary reflects confidence in the business. During its second-quarter conference call, the company projected third-quarter revenue of approximately $33.5 billion, implying year-over-year (YOY) growth of more than 260%. This anticipated top line strength is expected to translate into meaningful profitability gains.

Despite higher capex concerns, MU’s gross margin is projected to reach roughly 81%, representing a sharp improvement from the 39% adjusted gross margin recorded in the same period of the previous fiscal year. Earnings are similarly expected to accelerate, with projected earnings per share of $19.15 at the midpoint, compared with $1.91 a year earlier.

The data center business will sustain momentum. Strong demand for server infrastructure, combined with Micron’s strategic focus on high-value products such as high-bandwidth memory, high-capacity server modules, and data center solid-state drives, positions it well to capture demand.

Looking ahead, the company’s growth prospects are underpinned by sustained demand, an expanding addressable market, supportive pricing, and continued investment in next-generation technologies. Together, these factors provide a strong foundation for long-term performance.

From a valuation perspective, Micron trades at 6.19 times forward earnings, which is cheap relative to its projected growth. Consensus estimates indicate earnings could increase by more than 651% in 2026, followed by an additional 67.3% rise in fiscal 2027. Its robust growth and low valuation multiple suggest further upside potential in Micron stock.

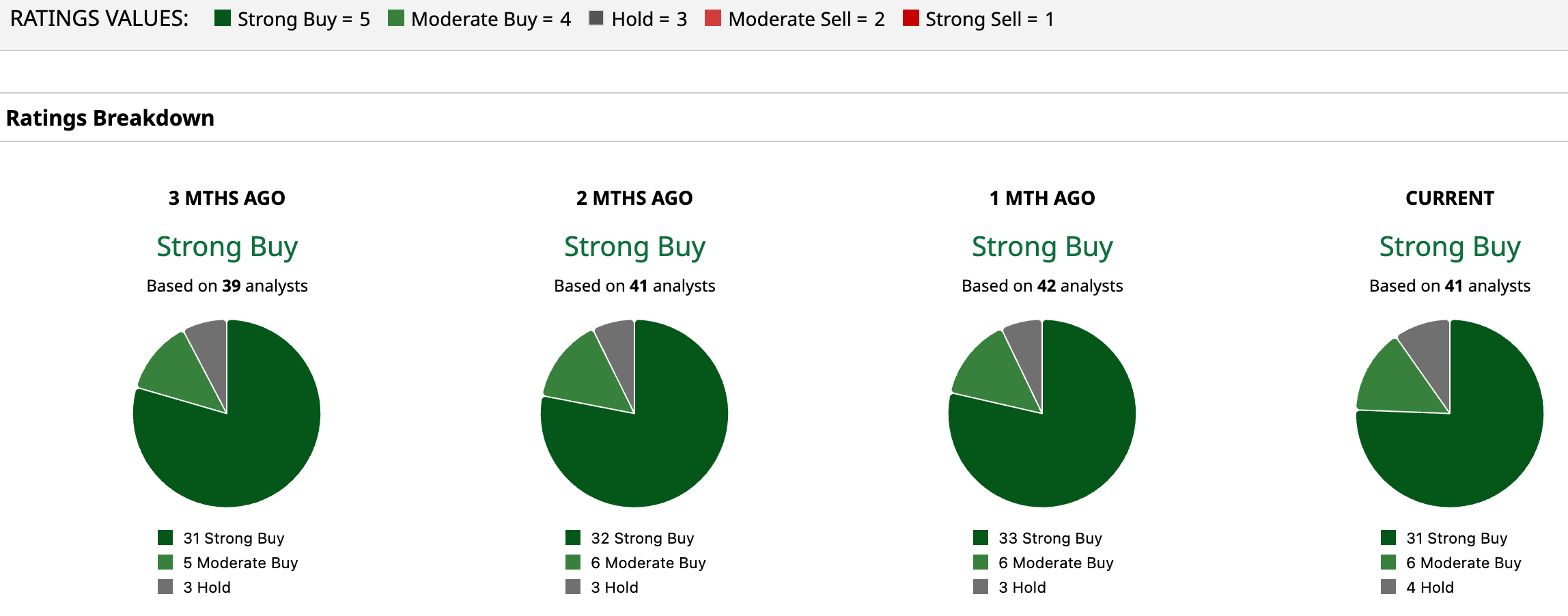

Wall Street’s sentiment toward MU stock remains favorable, with most analysts maintaining a “Strong Buy” consensus rating. Finally, analysts’ average price target of $494.81 implies about 46.5% upside potential from its recent closing price of $$337.84.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Renewable%20Energy%20by%20Yuri%20Hoya%20via%20Shutterstock.jpg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)