USDA grain market report days don’t come any bigger than Tuesday’s planting intentions and quarterly grain stocks reports, especially with spiking fertilizer prices and availability concerns bringing a new twist for potentially less U.S. corn planted acres this year.

A Dow Jones Newswires survey shows the average of analysts surveyed put U.S. planted corn acres at 94.481 million. Traders also expect higher U.S. corn stockpiles as of March 1 than seen at the same time last year. U.S. planted soybean acres are seen by analysts at 85.463 million acres. Traders also expect higher U.S. soybean stockpiles as of March 1 than seen at the same time last year. U.S. all wheat acres are seen by the analysts’ average at 44.605 million acres. The survey showed traders expect higher U.S. wheat stockpiles as of March 1 than seen at the same time last year.

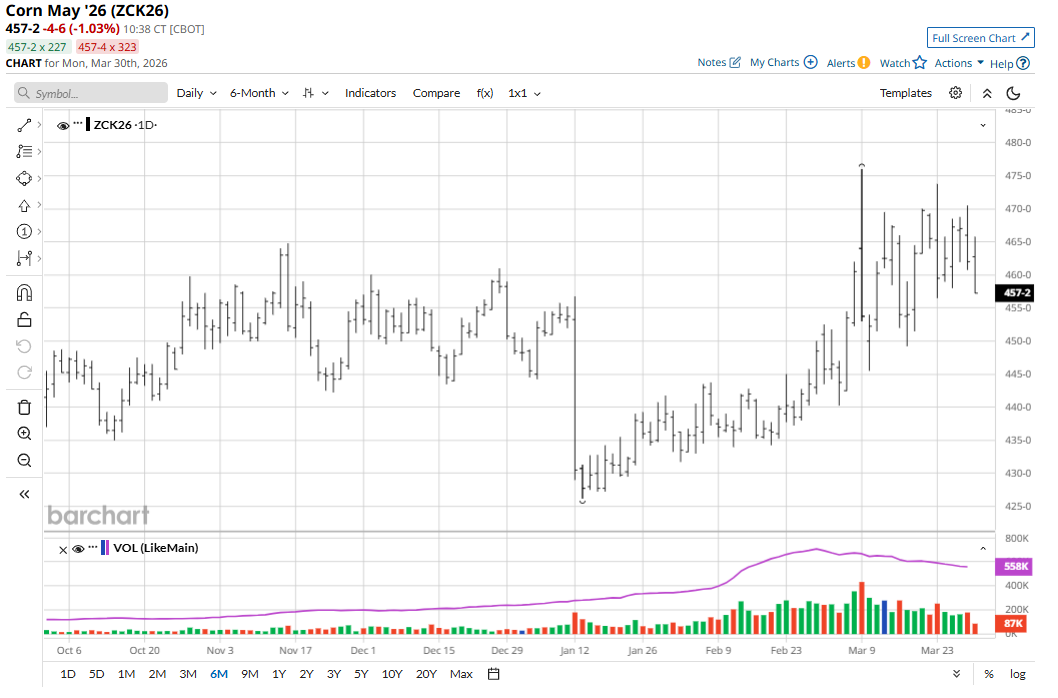

Corn Bulls Keep Price Uptrend Alive on Daily Chart

May corn (ZCK26) futures last week fell 3 1/2 cents for the week but a price uptrend on the daily bar chart remains in place. That should keep the technically oriented traders favoring the long side.

However, keener risk aversion in the general marketplace recently, due to the Middle East war, has worked to limit buying interest in the grain markets. So has a stronger U.S. dollar index ($DXY) that is hovering near a 10-month high. The grain markets will also remain vulnerable to swings in crude oil (CLK26) prices over the coming weeks as the war in Iran plays out.

Corn Traders Get Positive News on U.S. Biofuels Legislation

The EPA signed a waiver last week allowing for expanded sales of E15 gasoline at retail pumps into the early summer, and that waiver is likely to be extended. While the move is positive for ethanol demand, the reaction from markets was somewhat muted. Similar waivers have been signed in recent years and year-round E15 by way of legislation remains at a standstill. Further U.S. biofuels policy news is expected to be released as soon as this week.

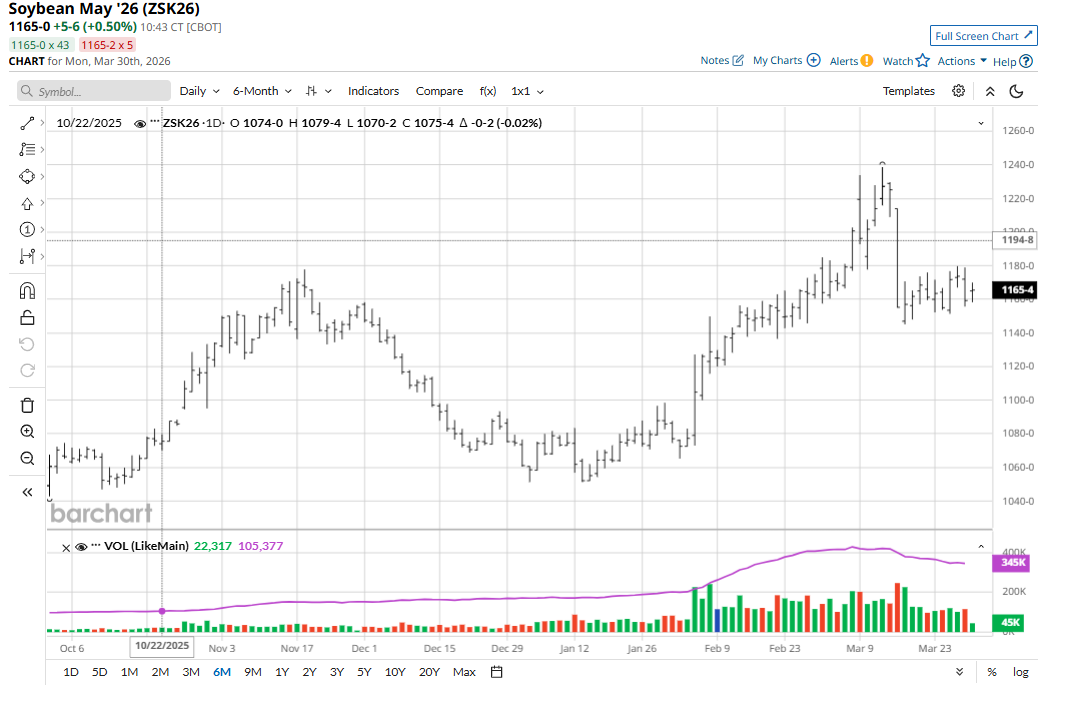

Soybean Bulls Continue to Struggle

May soybean (ZSK26) futures last week fell 2 cents on the week. The bean market has seen technical selling pressure as recent price action has formed a classic bear flag pattern on the daily bar charts for May and July futures.

Soybean and corn traders are still closely watching weather conditions in South American soybean-growing regions. Weather watchers say soil moisture in some Brazil crop areas is depleted and a boost in precipitation is needed to ensure the best crop development over the next few weeks. Argentina has become a little too wet recently in parts of the south and more rain is expected in that region over the next 10 days, raising some concern. However, South America’s corn and soybean growing seasons have not experienced any serious weather problems to cause serious crop damage or significant “weather scares” in the corn and soybean futures markets.

Grain Markets, Especially Soybeans, Await Trump-Xi May Summit

The planned summit between Presidents Donald Trump and Xi Jinping in China in mid-May have encouraged soybean complex bulls. However, bulls were somewhat dented late last week on news that China announced investigations into unfair U.S. trade practices.

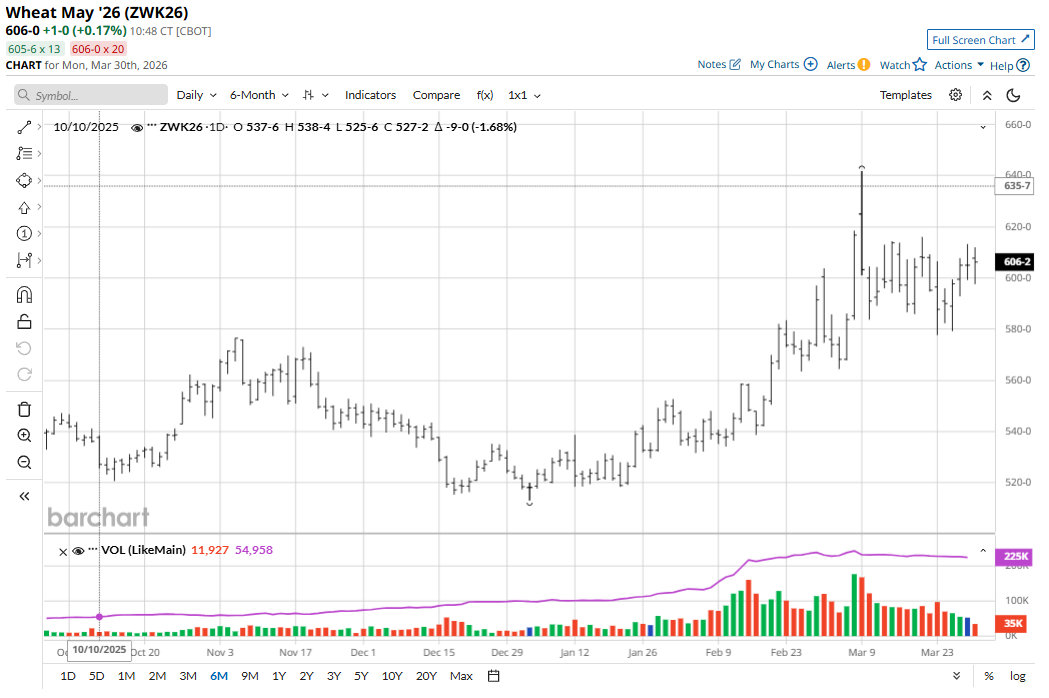

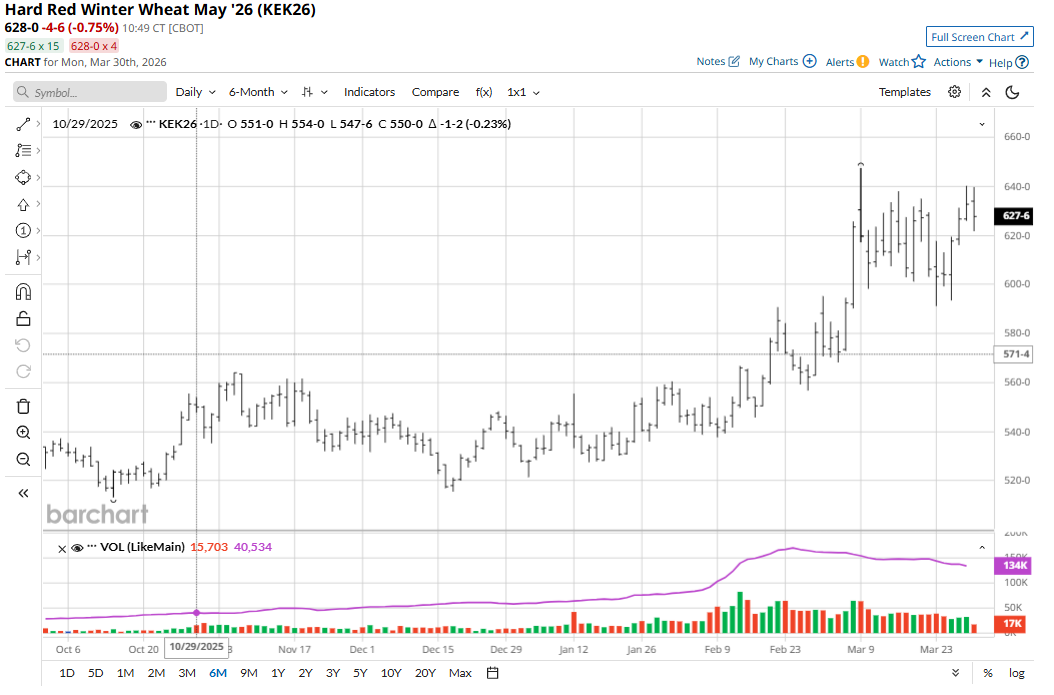

Winter Wheat Market Bulls Showing Resilience

May soft red winter (SRW) (ZWK26) wheat last week gained 9 3/4 cents. May hard red winter (HRW) wheat (KEK26) futures were up 26 1/2 cents on the week. Extreme weather fluctuations in the southern U.S. Plains have pushed the price premium HRW holds over SRW to over 25 cents a bushel. The winter wheat futures markets bulls had a good week last week. Price uptrends on the daily bar charts have restarted, which should continue to support some chart-based buying in the near term.

Winter wheat production concerns in the U.S. Plains are growing. Crop condition ratings have continued to decline in the region and more widespread ratings will be available next month as the growing season and USDA Crop Progress reports resume.

Lower Global Wheat Production This Year?

Rising input costs are likely to influence lower wheat plantings in the southern hemisphere, namely Australia. Reduced acres and potentially lower yields resulting from less fertilizer applications would help to ease the bloated supply weighing on global wheat balance sheets.

Tell me what you think. I enjoy hearing from my valued Barchart readers from all around the globe. Email me at jim@jimwyckoff.com.

On the date of publication, Jim Wyckoff did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)