Although an oil price shock has thrown a wrench into Carnival Corporation's (CCL) near-term outlook, the underlying story refuses to lose momentum. On Friday, March 27, the cruise ship company reported first-quarter fiscal 2026 results that moved past expectations on both revenue and earnings, while also delivering record bookings.

Demand, by all visible measures, continues to hum. Bookings for 2026 rose 10% year-over-year (YOY), with nearly 85% of sailings already sold. Customer deposits reached a record close to $8 billion, and onboard spending picked up pace as travelers committed earlier and spent more before even stepping onboard.

Yet the market chose to focus on a different current. The stock slipped 4.3% that day as rising fuel costs cast a shadow over the full-year outlook. Carnival now expects roughly $500 million in additional fuel expenses, driven by geopolitical tensions in the Middle East and disruptions around the Strait of Hormuz.

The company’s forecast builds on the assumption that futures for Brent crude, the global oil benchmark, will average $90 per barrel in April and May before easing to $85 in the third quarter and $80 in the fourth quarter. The management expects to offset part of the pressure through $150 million in operational improvements.

All things considered, the broader takeaway leans positive. Solid booking trends continue to anchor the demand story, while the newly authorized $2.5 billion share buyback adds a layer of confidence around capital allocation. Together, these factors reinforce the company’s long-term trajectory.

About Carnival Stock

Headquartered in Miami, Florida, Carnival Corporation stands as one of the largest cruise operators in the world, steering a diverse portfolio that stretches well beyond its fleet. With a market cap of approximately $30 billion, the company manages an ecosystem of brands, private island destinations, hotels, and transport services.

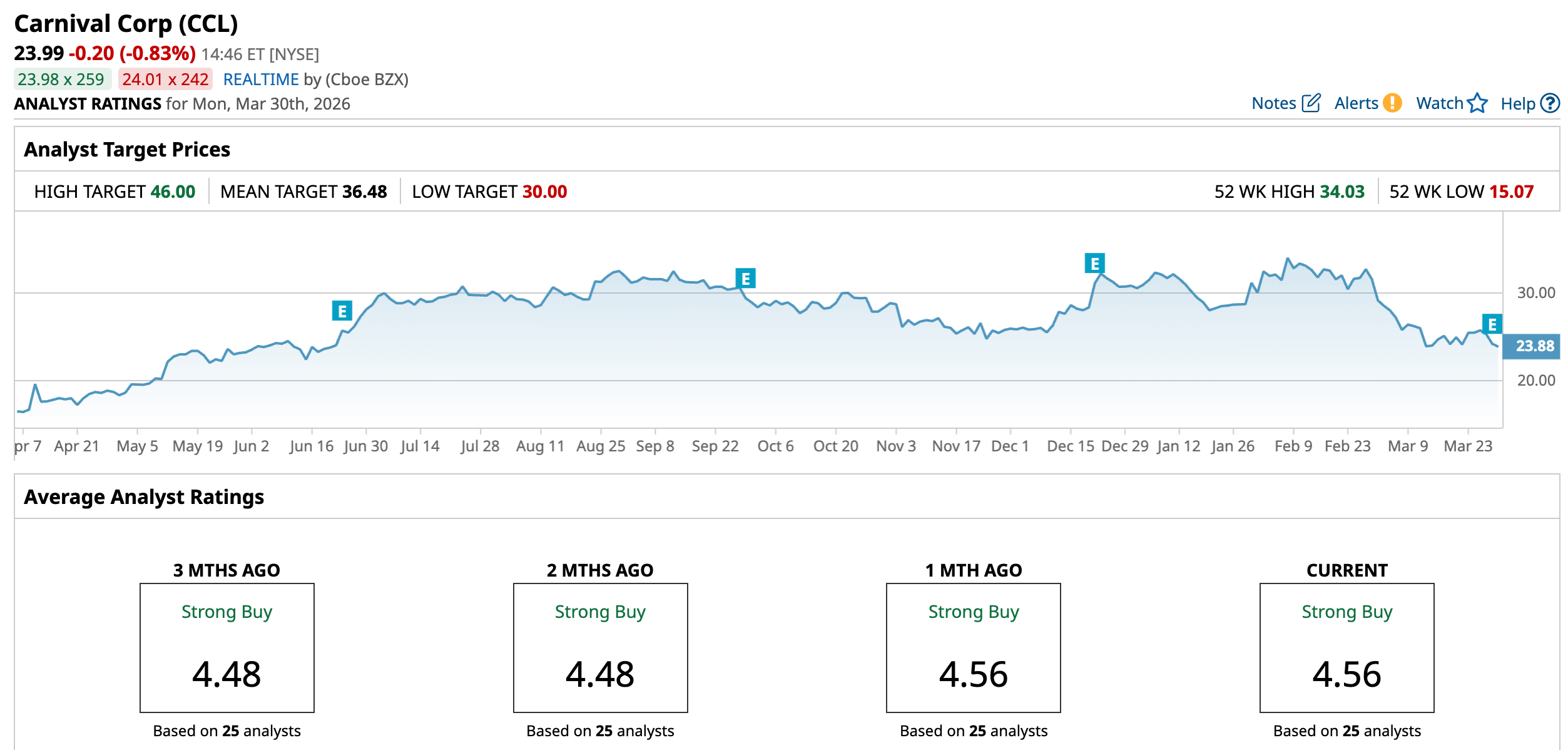

Fuel prices, geopolitical tensions, and shifting consumer dynamics have all left their mark as the stock is down 21.6% year-to-date (YTD). Even so, the stock has gained 20.48% over the past 52 weeks, which suggests the broader recovery narrative has not drifted off course.

From a valuation standpoint, CCL stock is trading at 10.69 times forward adjusted earnings, placing it at a noticeable discount to the industry average. When a company with global scale trades at a discount, it often invites a second look from those willing to stay the course.

On the income front, Carnival pays an annual dividend of $0.60 per share, translating to a yield of 2.48%. The company distributed its most recent dividend of $0.15 per share on Feb. 27 to shareholders on record as of Feb. 13. The payout signals financial stability and reinforces management’s commitment to returning capital, even as it navigates a challenging cost environment.

Carnival Surpasses Q1 Earnings

On March 27, Carnival reported its financial results for the first quarter of fiscal 2026, wherein revenue grew 6.1% YOY to $6.2 billion, topping analyst estimates of $6.1 billion. Adjusted EPS rose 53.8% from the year-ago value to $0.20, surpassing the Street’s forecast of $0.18.

Adjusted gross margin increased 7.2% from the prior year’s quarter to $4.7 billion, while adjusted net income climbed 58% to $275 million. Adjusted EBITDA was up 5.1% to $1.3 billion, reflecting steady operational traction. The company opened the year on a strong footing, recording its highest level of bookings to date, with demand stretching well into 2028 sailings.

Customer deposits reinforced the momentum, hitting a first-quarter record of nearly $8 billion, up close to 10% from the prior year. The steady inflow strengthens liquidity and provides a cushion as the company navigates cost fluctuations.

Looking ahead, management expects to deliver $7 billion in adjusted EBITDA for fiscal 2026, supported by yield growth and disciplined cost control. Operational improvements of nearly $150 million in adjusted net income should help offset part of the pressure from more than $500 million in higher fuel costs.

The cost pressure has already made its mark on guidance. The company now expects adjusted EPS of $2.21 for the full year, down from its earlier forecast of $2.48.

On the other hand, analysts expect second-quarter fiscal 2026 EPS of $0.34, reflecting a 2.9% YOY decline. Full-year earnings are projected to dip 1.8% to $2.21. However, projections for fiscal year 2027 call for a 20.8% rebound to $2.67, suggesting that while near-term margins may feel the heat, the longer-term earnings trajectory remains intact.

What Do Analysts Expect for Carnival Stock?

Analyst Ben Chaiken of Mizuho Securities, the Japanese investment banking and securities firm, maintains a “Buy” rating on the stock and has raised his price target from $38 to $39, reflecting growing confidence in the company’s ability to navigate near-term cost pressures while keeping its long-term growth engine intact.

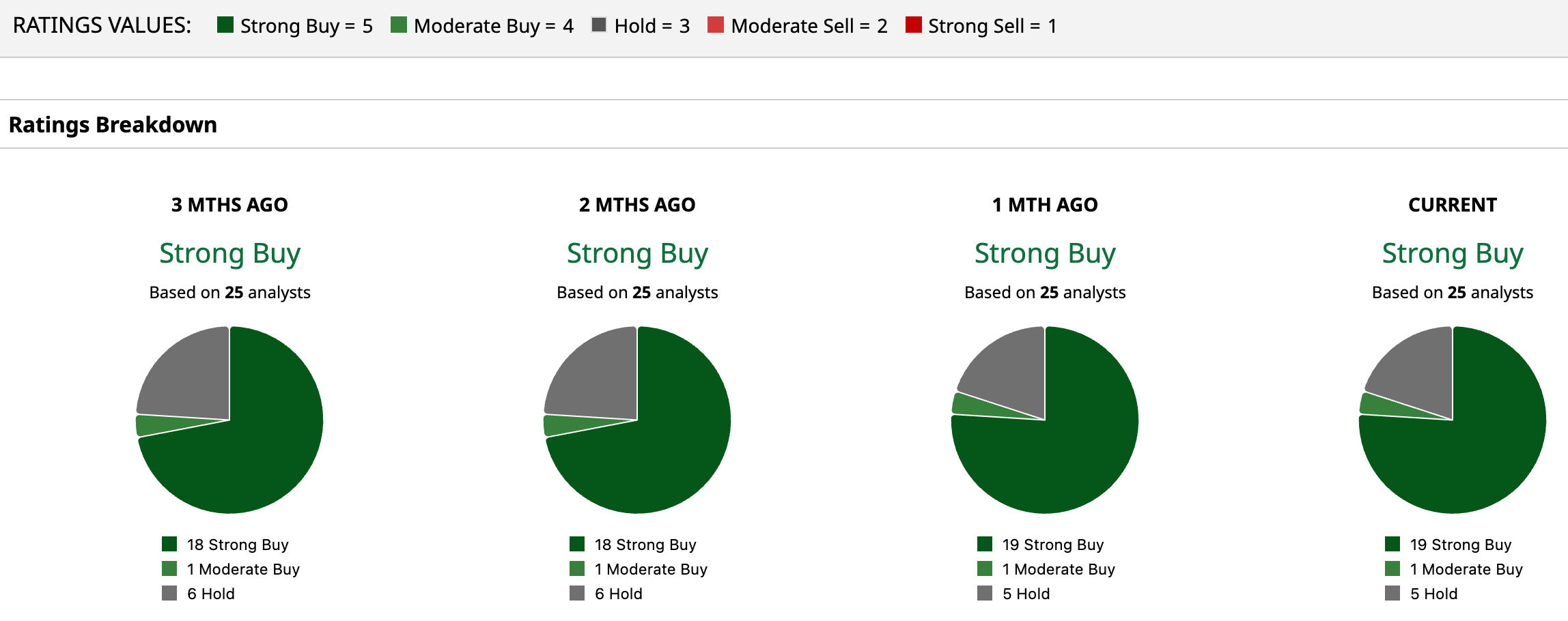

Wall Street, in fact, leans firmly in Carnival’s corner. The stock carries an overall rating of “Strong Buy.” Among 25 analysts covering the name, 19 have issued a “Strong Buy” rating, one recommends a “Moderate Buy,” and five suggest “Hold.”

The numbers reinforce that view with an average price target of $36.48, implying potential upside of 52%. Meanwhile, the Street-high target of $46 points to a possible gain of 91.8% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Lululemon%20Athletica%20inc_%20storefront%20by-%20Robert%20Way%20via%20iStock.jpg)

/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)