/Apple%20Inc%20logo%20on%20Apple%20store-by%20PhillDanze%20via%20iStock.jpg)

Wall Street firm Wedbush has sounded another voice of optimism for Apple (AAPL). This time, the reason is the company's upcoming developers conference (WWDC) in June. In a note to clients, the firm hinted that with an array of new products already under development or set for launch soon, Apple is positioned well to see a meaningful surge in revenues.

The firm said, “We note that the company is likely in the later stages of developing its foldable phone, iPhone Fold, based on supply chain checks, which is rumored to launch later this year alongside the iPhone 18 launch in September, adding an additional catalyst to its hardware revenue. We also note that the company continues to fuel its innovation engine with more Mac products expected to hit Apple’s stores with many rumors circulating around a touchscreen MacBook to allow developers to improve app testing and functionalities.”

Valued at a market cap of $3.6 trillion, AAPL stock is up 13% in the past year, with the launch of the iPhone 17 providing a much-needed boost to its fortunes. Now, if Wedbush is to be believed, the stock is poised for further upside. Does that warrant an investment in the iPhone maker's stock? Let's find out.

Numbers Remain Robust

Apple continues to demonstrate remarkable staying power in the consumer technology space, even with its premium pricing strategy. Over the past decade, the company has achieved CAGRs of 6.37% in revenue and 8.16% in earnings, a clear reflection of its powerful brand and the consistent quality of its products and services.

Notably, the most recent quarter provided further evidence of this strength. Revenue reached $143.8 billion, up 16% year-over-year (YoY) and ahead of consensus expectations. Much of the momentum came from the iPhone 17 lineup, which drove iPhone sales to $85.3 billion, a 23% increase from the prior year. The high-margin services business also performed well, growing to $30 billion from $26.3 billion in the year-ago period.

Gross margins also improved to 48.2%, highlighting Apple’s continued pricing discipline. Earnings per share rose 18% to $2.84, beating the Street forecast of $2.65. The company also returned capital to shareholders through $25.2 billion in share repurchases, providing an additional boost to EPS.

Meanwhile, cash flow from operations was particularly robust at $53.9 billion, an 80% increase from the previous year. Apple ended the quarter with $45.3 billion in cash and equivalents, comfortably exceeding its short-term debt of $13.8 billion.

From a valuation standpoint, AAPL trades at a premium to the broader sector, with forward P/E, P/S, and P/CF multiples of 29.25x, 7.85x, and 24.98x, respectively. However, when viewed against Apple’s own five-year averages, the current levels appear reasonable for a company of its caliber.

Leveraging AI To Make Its Products Even Better

Many had written Apple off due to its perceived slowness in adopting AI. Moreover, the somewhat botched launch of Apple Intelligence did not do its AI reputation any good. However, the company seems to be finally getting its act together, with a strategy based on its core strengths of design and privacy.

While other tech giants have rushed to launch standalone chatbots or highlight raw computational power, Apple is treating AI as an extension of user interface and product design. Apple Intelligence is being woven seamlessly into the daily user experience, such as smart notification summaries, writing assistance natively embedded in the keyboard, and intuitive photo editing. By prioritizing ease of use over technical flexibility, Apple is domesticating AI for the mainstream consumer, focusing on slowly but surely embedding AI across its 2.5 billion device base.

Then, a key component of Apple's design ethos is user privacy, which serves as a major attraction for many consumers. Notably, Apple's architecture specifically relies on on-device processing for most AI tasks and Private Cloud Compute for heavier workloads, creating a formidable competitive moat for the company. This privacy-centric design appeals to consumers and enterprise users who are hesitant to adopt AI due to data security concerns, ultimately reinforcing brand loyalty and ecosystem lock-in.

Meanwhile, the WWDC in June is expected to build upon these strengths by launching the revamped Siri. After significant delays, this new iteration of Siri is expected to finally deliver advanced conversational capabilities and deep ecosystem integration, potentially powered in part by a partnership with Google (GOOG) (GOOGL) Gemini. Notably, Apple is expected to showcase how Siri can now retain personal context, demonstrate onscreen awareness, and execute complex cross-application actions natively.

The event will also likely highlight the robust AI capabilities of the recently released M5 family of processors, which serve as the hardware foundation for these software advancements. Built on a third-generation 3nm process, the M5 chip features a 16-core Neural Engine and introduces dedicated Neural Accelerators within every core of its 10-core GPU. This architecture delivers over four times the peak GPU compute performance for AI workloads compared to the previous M4 generation.

Furthermore, the base M5 chip boasts a unified memory bandwidth of 153 gigabytes per second, while the M5 Max scales up to an impressive 614 gigabytes per second with up to 128 gigabytes of total unified memory capacity. These massive hardware specifications are critical because they allow Apple to run LLMs and advanced diffusion models entirely on the device, ensuring user privacy by eliminating the need for constant cloud processing.

Alongside iOS 20, developers anticipate new application programming interfaces that will allow them to weave these on-device capabilities into third-party applications. Ultimately, WWDC 2026 will demonstrate how Apple intends to leverage its tightly integrated hardware and software ecosystems, utilizing massive silicon upgrades to deliver a more seamless and intelligent user experience without compromising its strict privacy standards.

Analyst Opinion of AAPL Stock

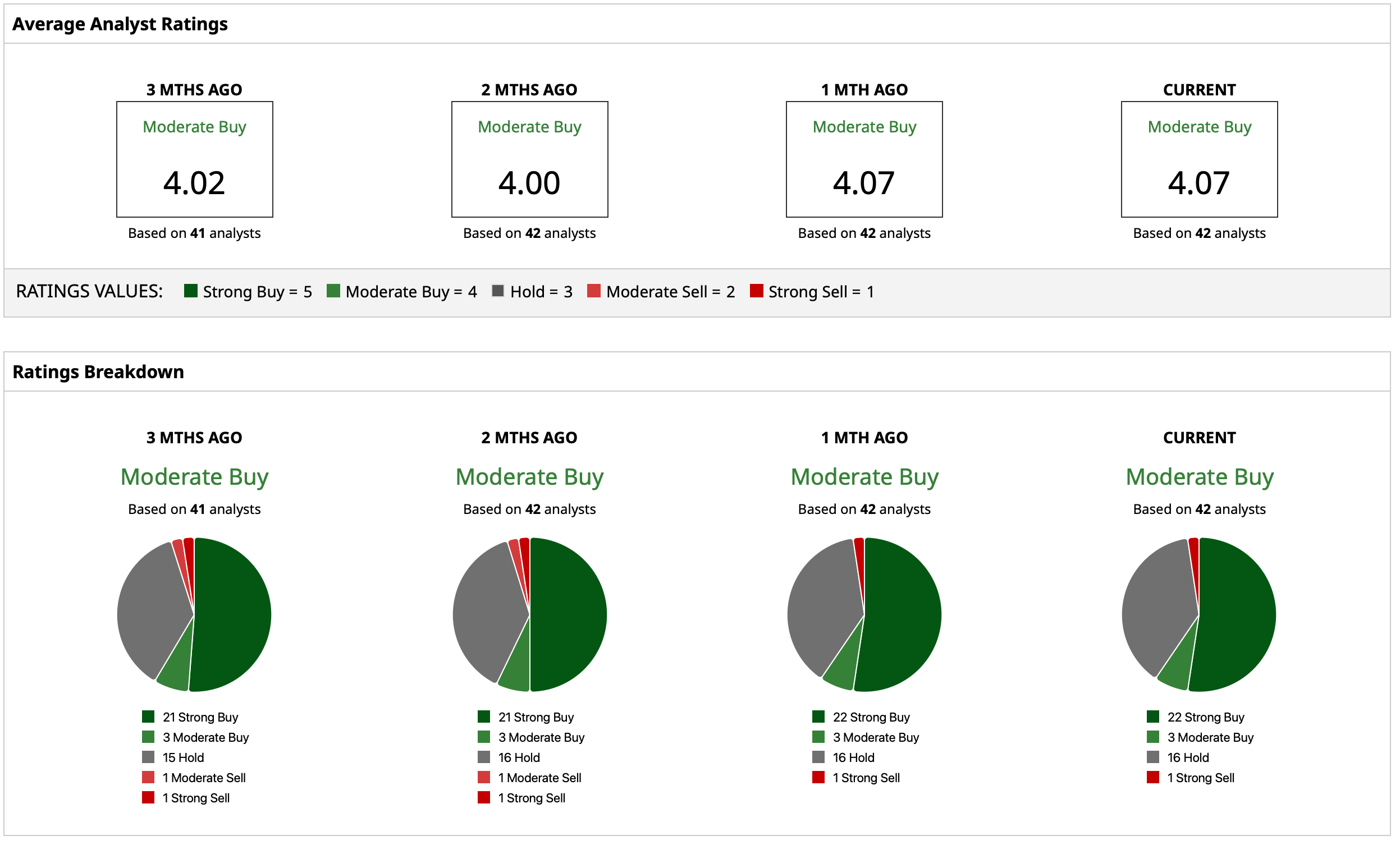

Thus, analysts remain moderately hopeful about AAPL stock, earmarking it a consensus rating of “Moderate Buy.” The mean target price of $295.76 denotes an upside potential of about 19% from current levels. Out of 42 analysts covering the stock, 22 have a “Strong Buy” rating, three have a “Moderate Buy” rating, 16 have a “Hold” rating, and one has a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launching%20into%20space%20by%20BEST%20BACKGROUNDS%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Close-up%20shot%20of%20Rivian%20R1T_%20Image%20by%20Trong%20Nguyen%20via%20%20Shutterstock_.jpg)