/Boston%20Scientific%20Corp_%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

Valued at a market cap of $102.8 billion, Boston Scientific Corporation (BSX) develops, manufactures, and markets medical devices for use in various interventional medical specialties. The Marlborough, Massachusetts-based company focuses on addressing unmet clinical needs across a wide spectrum of complex conditions, including cardiovascular, respiratory, digestive, oncological, neurological, and urological diseases. It is expected to announce its fiscal Q1 earnings for 2026 in the near future.

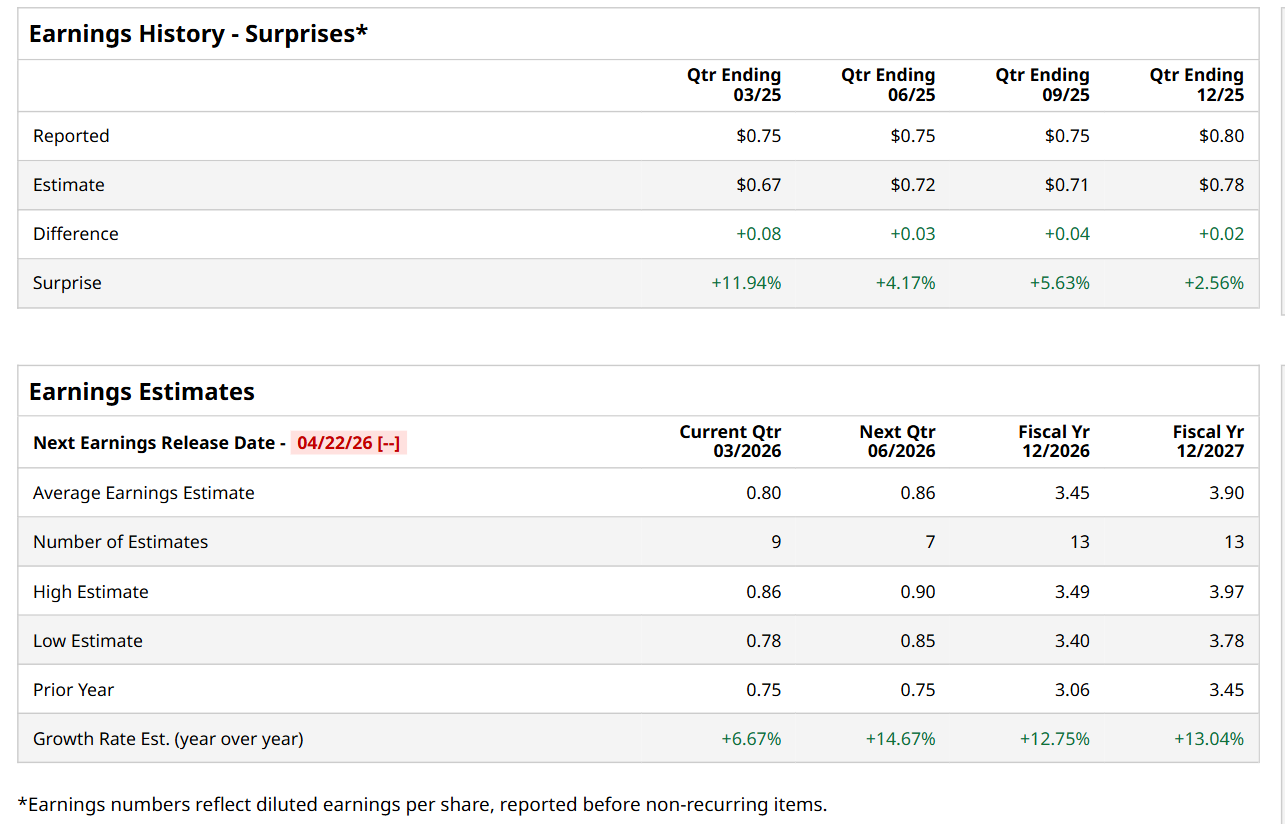

Before this event, analysts expect this healthcare company to report a profit of $0.80 per share, up 6.7% from $0.75 per share in the year-ago quarter. The company has topped Wall Street’s bottom-line estimates in each of the last four quarters. Its earnings of $0.80 per share in the previous quarter exceeded the forecasted figure by 2.6%.

For the current fiscal year, ending in December, analysts expect BSX to report a profit of $3.45 per share, up 12.8% from $3.06 per share in fiscal 2025. Furthermore, its EPS is expected to grow 13% year-over-year to $3.90 in fiscal 2027.

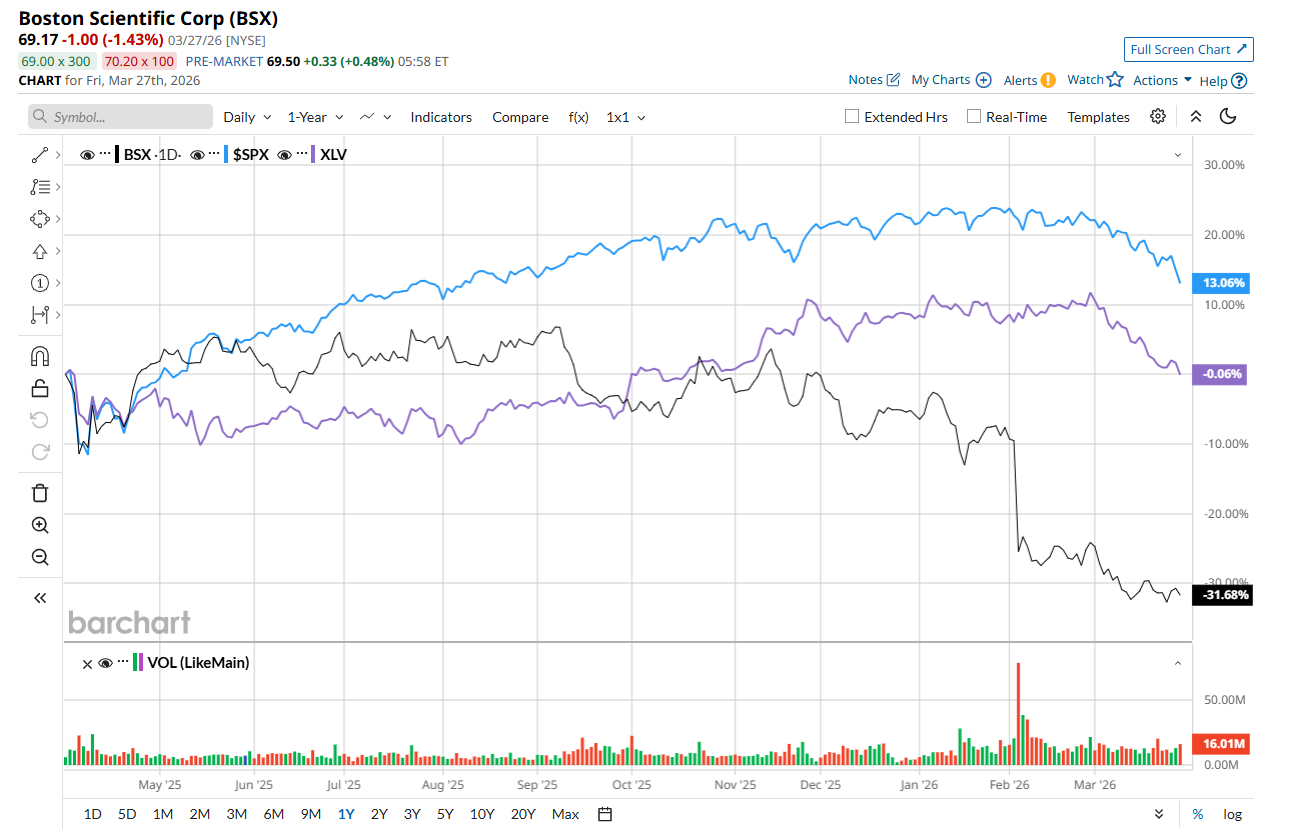

Shares of BSX have declined 31.4% over the past 52 weeks, notably underperforming both the S&P 500 Index's ($SPX) 11.9% return and the State Street Health Care Select Sector SPDR ETF’s (XLV) 1.2% drop over the same time period.

BSX has had a difficult start to the year, with its shares declining roughly 27.5% year-to-date. The downturn was triggered in part by its fourth-quarter results released on Feb. 4, after which the stock dropped 17.6%. On the surface, the results reflected solid operational performance. Its net sales increased 15.9% year-over-year to $5.3 billion, slightly ahead of analyst expectations of $5.27 billion. Its adjusted EPS rose 14.3% to $0.80, also beating the consensus estimate of $0.78.

However, markets tend to focus more on future outlook than past performance. Management’s guidance for the first quarter came in slightly below Wall Street expectations, shifting investor sentiment toward near-term uncertainty despite strong quarterly execution.

Further weighing on the stock, in March, The Law Offices of Frank R. Cruz announced a potential securities fraud class action lawsuit on behalf of investors who purchased shares between Jul. 23, 2025, and Feb. 3, 2026. The complaint alleges that the company overstated the sustainability of its U.S. electrophysiology (EP) segment growth, faced rising competition impacting market share, and made overly optimistic statements about its growth outlook that may have lacked a reasonable basis.

Wall Street analysts are highly optimistic about BSX’s stock, with an overall "Strong Buy" rating. Among 31 analysts covering the stock, 26 recommend "Strong Buy," three suggest "Moderate Buy,” and two indicate “Hold." The mean price target for BSX is $104.47, indicating a 51% potential upside from the current levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Quantum%20Computing/A%20concept%20image%20of%20a%20green%20and%20yellow%20motherboard_%20Image%20by%20Gorodenkoff%20via%20Shutterstock_.jpg)

/Tesla%20Inc%20logo%20by-%20baileystock%20via%20iStock.jpg)

/Intel%20Corp_%20badge%20holder-by%20hasrul_rais%20via%20Shutterstock.jpg)

/Advanced%20Micro%20Devices%20Inc_%20office%20sign-by%20Poetra_RH%20via%20Shutterstock.jpg)

/Super%20Micro%20Computer%20Inc%20logo%20on%20building-by%20Poetra_RH%20via%20Shutterstock.jpg)