/Intel%20Corp_%20badge%20holder-by%20hasrul_rais%20via%20Shutterstock.jpg)

Something rather interesting is happening in the CPU segment, and this isn’t getting enough attention yet. Pricing power is back. Intel (INTC) and AMD (AMD) are both increasing CPU prices by around 10% to 15%, and sometimes even higher. That’s not noise; that’s a signal.

Furthermore, the increase in delivery times ranging from a few weeks to several months may be a signal of a more profound issue. This isn’t merely a cyclical issue; this is a structural issue. CPUs, which are normally ignored by the public in favor of GPUs, are becoming relevant once again.

However, the overall market isn’t convinced. Intel shares are currently below their highs by about 20% and are down from their peak, even after a robust performance over the past year. Therefore, the million-dollar question that everyone wants to answer is: Is this a turning point… or merely a temporary windfall?

About Intel Stock

Intel is a leading semiconductor company based out of Santa Clara, California. With a market cap of about $235 billion, Intel is one of the biggest semiconductor companies out there. The company operates across the client computing, data center, and foundry segments. All these are becoming increasingly relevant due to the rise of artificial intelligence.

From a stock performance standpoint, INTC has had a volatile performance. The stock has gained nearly 150% over its 52-week lows but has underperformed its highs. From a relative standpoint, Intel’s performance has been robust compared to the overall S&P 500 ($SPX).

But valuation is where things get interesting. The forward price-earnings ratio is close to 690x. Let’s be honest here; this is not really a “value turnaround story.” The profitability numbers are also fragile, as margins and return on equity continue to suffer. Even in terms of price-sales ratios of 4.16x, this is still not really cheap, particularly given the decline in sales.

The 1.4% dividend yield is certainly a positive; however, we must all admit that this is not really why we’re here. This is a turnaround story, after all.

Intel Misses on Earnings but Signals a Transition

Intel’s latest earnings were… interesting. Let’s just say that. For Q4 2025, Intel’s revenue was down 4% year-over-year (YoY) to $13.7 billion. Full-year revenue was flat YoY at $52.9 billion. EPS continued to suffer as well, as Intel posted a GAAP loss of $(0.12) in Q4.

On a non-GAAP basis, things were slightly better: $0.15 in EPS in Q4 and $0.42 in EPS for the full year. However, we must all admit that this is still not really all that impressive. However, there is something to consider here: forward guidance. Q1 2026 revenue is expected to come in between $11.7 billion and $12.7 billion, with EPS coming in breakeven to slightly negative.

But there is something interesting to consider here: supply constraints. These are affecting Intel’s business, as Q1 will be the toughest quarter before things improve in Q2. This is directly in line with the price increases we’re seeing in CPUs.

And then there is the bigger picture. Intel is aggressively ramping up its 18A process node. This is a bold and perhaps necessary move on Intel’s part to retake the technology crown. While the risk of success is still high, this is no longer just about demand; it’s about delivery.

What Do Analysts Expect for INTC Stock?

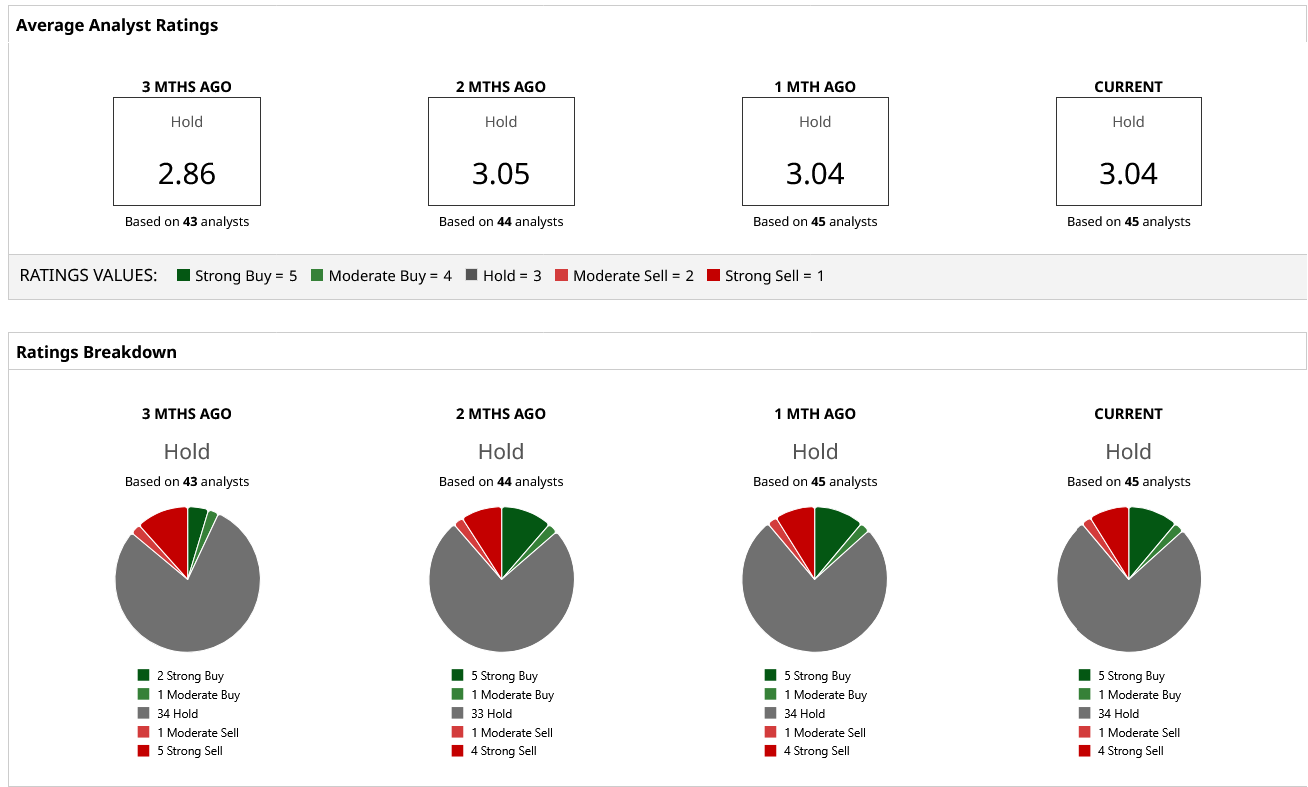

The sentiment on the Street is, shall we say, less than bullish for INTC stock with a “Hold” rating consensus, but the mean price target for the stock is a relatively flat $45.26, which is almost equivalent to its current price. This is interesting, as that mean price target implies a gain of only about 5%, which is a fairly low level of conviction among the analysts who cover the stock, especially considering the wide range from a low of $24 to a high of $66.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/Alibaba%20by%20Photo%20Agency%20via%20Shutterstock.jpg)