Even during a down period for the markets, Trinity has gone against the grain, climbing to $31.46. Its shares have yielded a 13% return over the last six months, beating the S&P 500 by 14%. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Trinity, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Trinity Not Exciting?

We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons we avoid TRN and a stock we'd rather own.

1. Backlog Declines as Orders Drop

We can better understand Heavy Transportation Equipment companies by analyzing their backlog. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into Trinity’s future revenue streams.

Trinity’s backlog came in at $1.7 billion in the latest quarter, and it averaged 27.8% year-on-year declines over the last two years. This performance was underwhelming and shows the company is not winning new orders. It also suggests there may be increasing competition or market saturation.

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Trinity’s revenue to stall. While this projection indicates its newer products and services will spur better top-line performance, it is still below the sector average.

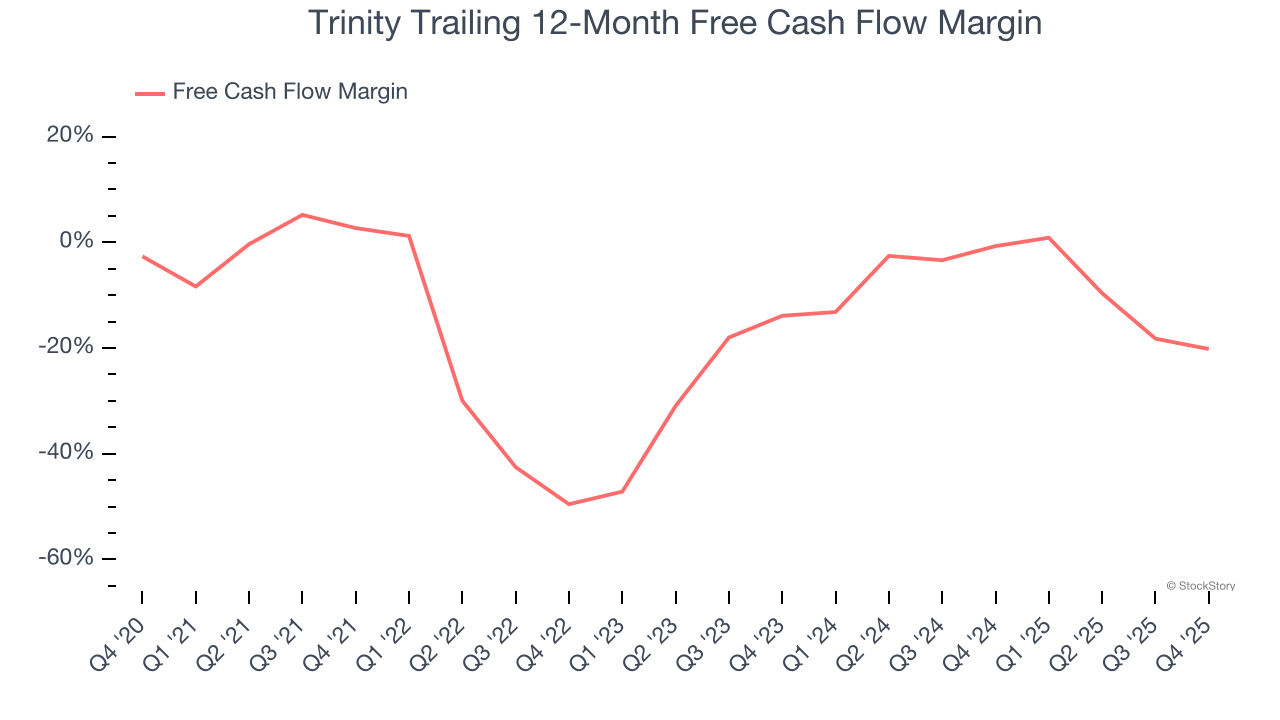

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Trinity’s margin dropped by 22.9 percentage points over the last five years. Almost any movement in the wrong direction is undesirable because it is already burning cash. If the trend continues, it could signal it’s becoming a more capital-intensive business. Trinity’s free cash flow margin for the trailing 12 months was negative 20.2%.

Final Judgment

Trinity isn’t a terrible business, but it doesn’t pass our bar. With its shares outperforming the market lately, the stock trades at $31.46 per share (or a trailing 12-month price-to-sales ratio of 1.2×). The market typically values companies like Trinity based on their anticipated profits for the next 12 months, but there aren’t enough published estimates to arrive at a reliable number. You should avoid this stock for now - better opportunities lie elsewhere. We’d suggest looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

/Super%20Micro%20Computer%20Inc%20HQ%20photo-by%20Tada%20Images%20via%20Shutterstock.jpg)

/Microsoft%20logo%20on%20building%20by%20franz12%20via%20iStock.jpg)

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)