Shares of General Mills (GIS) have fallen sharply amid weakening demand, margin pressure, and a broader slowdown across the packaged food sector, pushing the stock’s dividend yield up to an eye-catching 6.53% range. While that elevated yield may appeal to income investors, it is largely a byproduct of declining equity value rather than strengthening fundamentals, with the company guiding for a double-digit decline in earnings.

At the same time, a new macro risk is emerging. Analysts at Jefferies caution that consumer packaged goods companies like General Mills are particularly vulnerable to rising oil prices, as higher energy costs ripple through transportation, packaging, and supply chains, threatening to further squeeze margins at a time when pricing power is already under pressure.

The impact will vary based on companies’ operational efficiency and supply chain positioning, while broader risks are intensifying, including warnings from the World Food Program (WFP) about potential disruptions to global food distribution.

Amid this backdrop, is GIS stock, trading at deep valuation discounts, worth buying now? Also, does a 6.53% dividend yield provide enough compensation for these mounting risks? Let’s dig deeper.

About General Mills Stock

General Mills is a leading global packaged food company headquartered in Minneapolis, with a diversified portfolio spanning cereals, snacks, meals, baking products, and pet food under well-known brands such as Cheerios, Pillsbury, and Blue Buffalo. The company operates across North America, Europe, Asia, and Latin America, supplying products through retail, foodservice, and e-commerce channels. General Mills has a market cap of around $19.7 billion, reflecting its position as a large-cap consumer staples player, though its valuation has declined significantly over the past year amid softer demand and margin pressures.

Shares of General Mills have been under significant pressure, reflecting a combination of weakening demand trends, margin compression, and broader concerns across the packaged food sector. On a year-to-date (YTD) basis, the stock is down around 23%, driven by a sharp selloff as earnings expectations deteriorated.

Over the past 12 months, General Mills shares have fallen by 38%, and the stock is down 42% from its 52-week high of $62.61, reached in April 2025. GIS stock’s performance underscores a transition from a traditionally defensive consumer staples name to one increasingly exposed to cyclical and cost-driven headwinds.

General Mills currently trades at a compressed valuation, reflecting growing investor skepticism around its growth outlook. The stock is valued at 10.77x forward earnings, well below historical averages for the company and at a discount to the sector median.

On the other hand, General Mills’ dividend remains a key component of its investment appeal, particularly as the stock’s decline has pushed the yield to 6.53%, well above the consumer staples average. The company pays an annual dividend of about $2.44 per share, while its payout ratio is around 72.8%, raising concerns.

However, dividend growth has seen a relatively slow pace, and rising earnings pressure suggests that while the yield is attractive, future increases may remain limited unless underlying fundamentals improve.

Muted Financial Performance

General Mills reported its fiscal 2026 third-quarter results on March 18, delivering a mixed but broadly weak set of numbers that underscored ongoing operational and demand challenges.

Net sales declined 8% year-over-year (YoY) to $4.4 billion, reflecting the impact of divestitures, softer volumes, and pricing adjustments, while organic sales fell about 3% YoY, indicating underlying demand weakness across key categories. On the bottom line, adjusted EPS came in at $0.64, down 37% from the prior year, marking a significant YoY contraction driven by cost pressures. Net income also declined materially to about $303 million from $626 million a year earlier, highlighting the extent of margin compression.

Moreover, weakness was most pronounced in North American retail, the company’s largest division, where sales saw a steep decline, partially offset by more resilient international and pet food performance.

Furthermore, management reaffirmed its fiscal 2026 guidance, calling for organic net sales to decline 1.5% to 2% and adjusted operating profit and EPS to fall 16% to 20%, signaling that near-term pressures are expected to persist before a potential recovery in the fourth quarter.

Analysts predict EPS to be around $3.44 for fiscal 2026, a decline of around 18.3% YoY, and a decline of 2.3% to $3.36 in fiscal 2027.

What Do Analysts Expect for GIS Stock?

Recently, Barclays lowered its price target on GIS stock to $41 from $43 while maintaining an “Equalweight” stance. Barclays expects flat pricing and a modest YoY decline in category volumes in fiscal 2027.

Also, TD Cowen cut its price target on General Mills to $37 from $45 while maintaining a “Hold” rating, citing ongoing volume and margin pressures expected to persist into fiscal 2027.

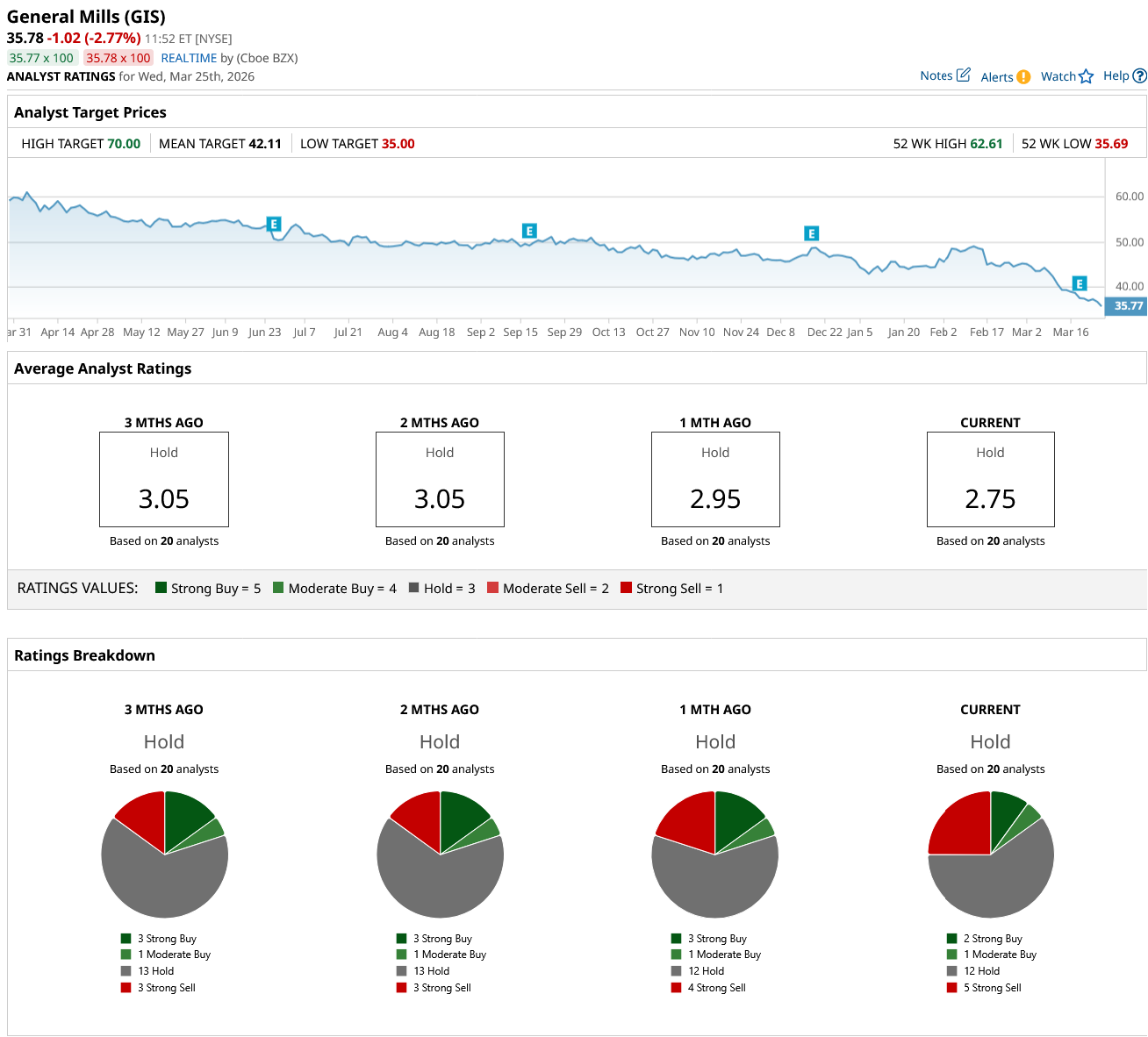

GIS stock has a consensus “Hold” rating overall. Out of 20 analysts covering the stock, two recommend a “Strong Buy,” one gives a “Moderate Buy,” 12 analysts stay cautious with a “Hold” rating, and five have a “Strong Sell” rating.

GIS stock's average analyst price target of $42.11 indicates an 18% upside potential, while the Street-high target price of $70 suggests a 96% upside ahead.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)