The artificial intelligence (AI) boom has created a new class of infrastructure winners, but the recent AI-driven market pullback has punished many of the companies positioned to benefit from the long-term expansion of data centers and power demand. Fluence Energy (FLNC) has been among the hardest-hit names in the AI infrastructure space this week, as investors rotated away from high-growth themes and questioned valuations across the sector.

However, the sell-off has also created a potential opportunity for investors who believe the AI revolution will require more than advanced chips and computing power. As AI data centers consume unprecedented amounts of electricity, companies that provide grid stability, energy storage, and power management solutions could become critical players in the next phase of the AI buildout.

Fluence has gained attention after its battery storage technology was included in AI data center infrastructure designs involving Siemens (SIEGY) and Nvidia Corporation (NVDA), highlighting its potential role in solving the power challenges behind next-generation AI facilities.

With shares sharply lower, is this a chance to buy a long-term growth company at a more attractive valuation?

About Fluence Stock

Fluence Energy is a global energy storage technology company focused on accelerating the transition to a more resilient and sustainable power grid. Headquartered in Arlington, Virginia, Fluence provides grid-scale battery energy storage systems, digital energy management software, and optimization services that help utilities, renewable energy developers, and commercial customers manage electricity demand and improve grid reliability.

The company’s solutions are increasingly gaining attention as rising electricity demand from AI data centers and electrification trends create greater demand for flexible power infrastructure. The company currently has a market cap of $3.64 billion.

Fluence Energy has delivered a strong performance over the past year as investors increasingly recognized the company’s role in the growing demand for energy storage infrastructure supporting renewable power, grid modernization, and the artificial intelligence data center boom.

Shares have benefited from improving investor sentiment around power infrastructure, reflecting renewed optimism around Fluence’s growth opportunity, supported by improving operating trends. The stock is up 204.68% over the past year.

However, after the strong run, Fluence shares have recently come under pressure as the broader AI infrastructure trade experienced a sharp pullback. The stock has declined 19.47% over the past five trading days, including a 15.8% drop on June 23 and an additional 6.9% decline on June 24, as investors rotated away from high-growth AI-related names and reassessed valuations.

The recent weakness has erased part of the stock’s gains but has also brought renewed attention to whether the sell-off represents a short-term sentiment-driven decline or a potential entry point for long-term investors who believe energy storage will be a critical component of the AI-powered electricity demand cycle.

The stock is trading at a discounted valuation of 1.00 times compared to its industry peers at 1.98 times sales (TTM).

Improving Financial Standing

Fluence Energy reported its fiscal second-quarter 2026 results on May 6. Revenue for the quarter reached $464.9 million, up 7.7% year-over-year (YOY), supported by higher deployment activity and continued demand for battery energy storage systems. Gross profit increased to $46.6 million from $42.6 million a year earlier, while gross margin improved slightly to 10% from 9.9%, reflecting better project execution and pricing discipline.

The company also made progress on the bottom line, although it remained unprofitable. Net loss narrowed significantly to $29.2 million, compared with a loss of $41.9 million in the same quarter last year. This translates to a loss of $0.16 per share compared to a loss of $0.24 per share in the prior year quarter. Adjusted EBITDA improved to a loss of $9.4 million from a loss of $30.4 million, showing meaningful improvement.

One of the biggest highlights from the quarter was Fluence’s expanding demand pipeline. The company reported a record backlog of $5.6 billion as of Mar. 31, 2026, while YTD (through May 6, 2026) order intake doubled to roughly $2.0 billion compared with $1.0 billion in the comparable period last year. Fluence also announced master supply agreements with two major hyperscalers and expects its first orders from these relationships during the third quarter, strengthening its exposure to the growing AI data center power demand theme.

Fluence reaffirmed its fiscal 2026 outlook, maintaining expectations for revenue of approximately $3.2 billion to $3.6 billion, with a midpoint of $3.4 billion, and adjusted EBITDA of $40 million to $60 million, with a midpoint of $50 million. The company also expects annual recurring revenue to reach approximately $180 million by the end of fiscal 2026. Management’s continued confidence is supported by a strong liquidity position, with total liquidity of around $900 million at the end of the quarter.

Analysts expect the company’s loss per share to improve 40.5% YOY to $0.22 in fiscal 2026 and again rise 177.3% to an EPS of $0.17 in fiscal 2027.

What Do Analysts Expect for Fluence Stock?

This month, Mizuho maintained an “Underperform” rating and $15 price target on Fluence Energy, despite acknowledging the company’s potential upside from AI data center demand.

On the other hand, last month, Roth/MKM upgraded Fluence Energy to “Buy” from “Neutral” and raised its price target to $26 from $13, citing improving profitability, stronger order momentum, and expanding opportunities in AI data center power infrastructure.

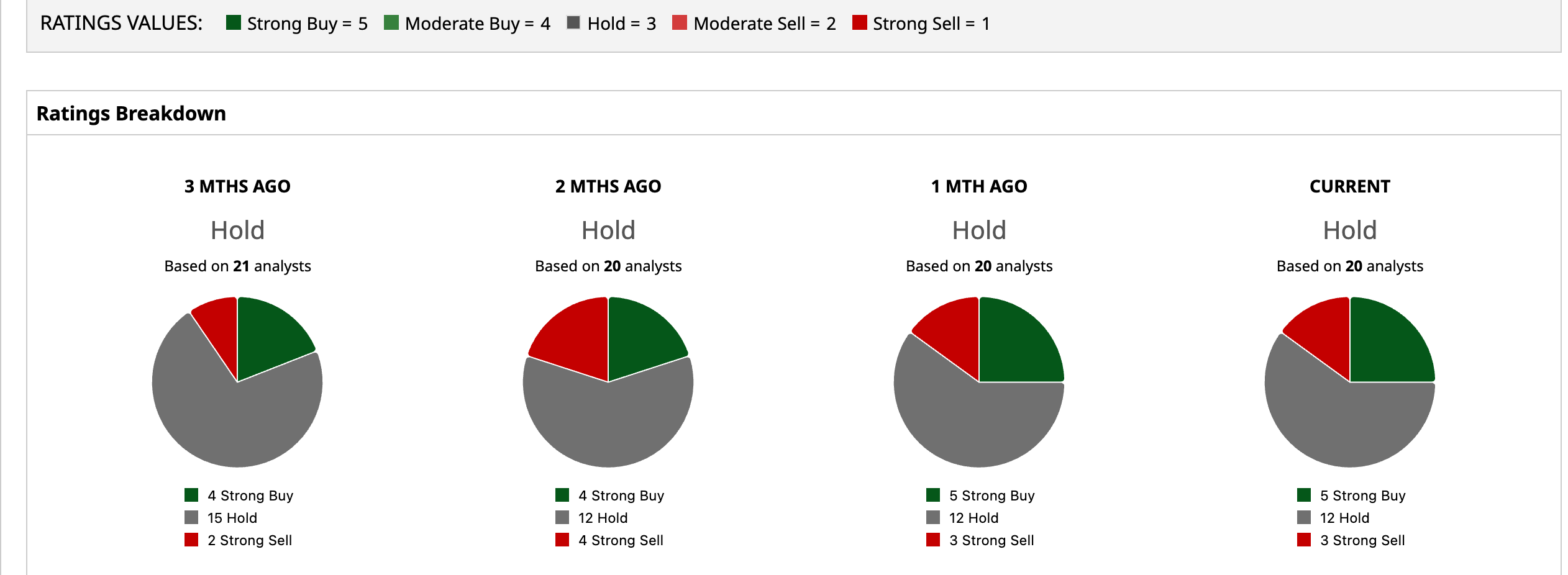

Overall, FLNC has a consensus “Hold” rating. Of the 20 analysts covering the stock, five advise a “Strong Buy,” 12 analysts give a “Hold” rating, and three offer a “Strong Sell.”

While the stock is trading at a premium to the average analyst price target of $18.47, the Street-high target price of $28 suggests that the stock could rally as much as 43.9%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)