/Alibaba%20by%20Photo%20Agency%20via%20Shutterstock.jpg)

Alibaba (BABA) isn’t having a great start to the year. Down about 15% on earnings, competition, and its recent failure to reassure markets that AI progress is outweighing weakness in other parts of its business, investors are turning away from BABA stock.

Granted, management just iterated a goal to generate more than $100 billion in annual revenue from its cloud and AI business over the next few years. Alibaba also reported cloud revenue growth of about 36% year-over-year (YOY) to $6.2 billion, thanks to AI workloads. Management even noted that AI revenue has been growing at triple-digit rates for about 10 quarters.

Unfortunately, though, the risk may outweigh the reward at the moment. For one, investors have to consider heavy competition from Tencent (TCEHY), Amazon (AMZN), and Microsoft (MSFT), which are also investing substantially in AI growth. There are concerns about the company’s declining profits as well, partly because of its heavier spending on cloud and AI. Lastly, as the company attempts to shift from e-commerce to a cloud and AI platform, it will need more investments — and take on more risk.

Recent Earnings Are Nothing to Write Home About

In its most recent quarter, Alibaba saw a 2% increase in revenue, a drop of 74% YOY in operating income, a 49% dip in operating cash flow, and a 71% decrease in free cash flow. Adjusted EBITA was down 57% to $3.34 billion, while adjusted EPS was down 67% to 13 cents.

As noted by Seeking Alpha, the company's investments in AI “come at the detriment of net income,” with Alibaba's cloud revenue growth appearing insufficient compared to Microsoft Azure's 39% growth "from a much larger base." What's more, Alibaba faces further headwinds, such as "limitations in accessing top-of-the-line microchips.”

Alibaba CEO Eddie Wu believes that AI will continue to be a major growth engine. "Our Cloud Intelligence Group’s revenue is up 36% with AI-related product revenue delivering triple-digit growth for the tenth consecutive quarter,” noted Wu. In addition, Alibaba's Qwen AI app notably surpassed 300 million users.

Unfortunately, red flags remain even with the triple-digit growth, given that the top-line numbers were severely underwhelming. Plus, Alibaba saw a significant drop in earnings with poor operational results, while sales and marketing costs more than doubled. With the risks outweighing the rewards, investors may want to avoid BABA stock for now, waiting and seeing before putting capital to work.

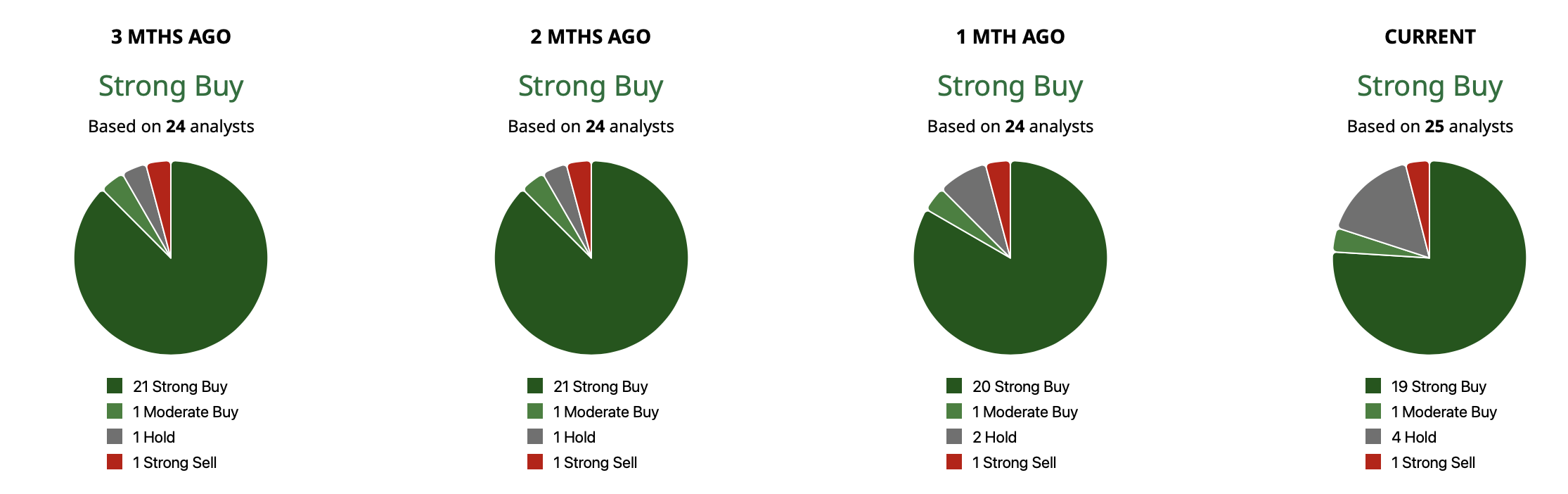

What Do Analysts Say About BABA Stock?

Of the 25 analysts covering BABA stock, 19 have a “Strong Buy" rating, one has a “Moderate buy,” and five analysts have a “Hold" rating. The mean target price of $186.50 implies 49% potential upside from current levels. Meanwhile, the high-end target of $212 implies as much as 70% possible growth from here.

At the moment, there are too many red flags to jump into BABA stock. On one hand, the company’s pivot to AI and cloud shows impressive growth potential, with massive AI revenue expansion and over 300 million users on its AI app. However, poor earnings and collapsing profits, competition, and a failure to reassure markets that its AI progress is outweighing weakness in other parts of the business are all turning off investors.

For investors with a very long-term horizon and appetite for intense volatility, dipping a toe into Alibaba could pay off if the company successfully executes its AI and cloud strategy. For those seeking stability and clear growth, wait on the sidelines until earnings recover.

On the date of publication, Ian Cooper did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)