/Tesla%20charging%20station%20black%20background%20by%20Blomst%20via%20Pixabay.jpg)

Since peaking near $498, Tesla (TSLA) slipped to a recent low of $364.46 on March 20 before the oversold stock started to pivot. Last trading at $386 per share, I’d like to see Tesla initially retest $420 thanks to what Morgan Stanley calls "the most important catalyst."

According to analyst Andrew Percoco, the company’s robotaxi rollout is that most important catalyst. Percoco believes that “superior robotaxi unit economics are supported by vertical integration and innovative Cybercab production” and that “Tesla is changing the way cars are made.” He added that each mile driven by the robotaxi fleet will also help improve the AI model for Full-Self Driving (FSD). Morgan Stanley has an ”Equal Weight" rating on TSLA stock with a price target of $415.

Robotaxis Could Create a $2 Trillion Market Opportunity

Expected to see substantial demand, the global robotaxi market is anticipated to grow from about $10.11 billion in 2025 to $18.27 billion this year and to $2 trillion by 2034. In addition, according to Boston Consulting Group, the global robotaxi fleet could grow to 3 million vehicles by 2035 in the best-case scenario, with China and the U.S. dominating a good deal of initial growth. That's all thanks to regulations and infrastructure advancements, with vehicle-to-infrastructure and vehicle-to-vehicle technologies.

Tesla could be one of the best-positioned to dominate the market, according to brokerage firm New Street Research, which has a “Buy” rating on TSLA stock with a $600 price target. New Street argues that Tesla has three unique advantages over the competition, including low unit costs, a flexible supply model, and an existing fleet. Investors also have to consider that Tesla has some 6 million cars in its training fleet, with FSD software collecting more than 8.8 billion miles of information. In addition, when under active supervision with minimal intervention, the vehicles are seeing seven times fewer major collisions, seven times fewer minor collisions, and five times fewer off-highway collisions.

Wedbush Foresees a Big Year for Tesla

With an “Outperform” rating and $600 price target on Tesla, Wedbush analyst Dan Ives noted the potential with Tesla. “We believe Tesla and Musk are heading into a very important chapter of their growth story as the AI Revolution takes hold and the Robotaxi opportunity is now a reality on the doorstep," Ives said.

“Investors are starting to see through the near-term demand issues for Tesla and recognize that Tesla is in a pole position to be a clear leader in the autonomous market opportunity with Robotaxis set to scale to 30 to 35 cities in the US over the next year,” Ives continued. “We expect over the coming months an easing of the federal framework for autonomous with more power going to the federal regulators with states having less authority on the autonomous rules framework."

Overall, Ives believes that "Tesla could reach a $2 trillion market cap by the middle of 2026 in a bull case scenario."

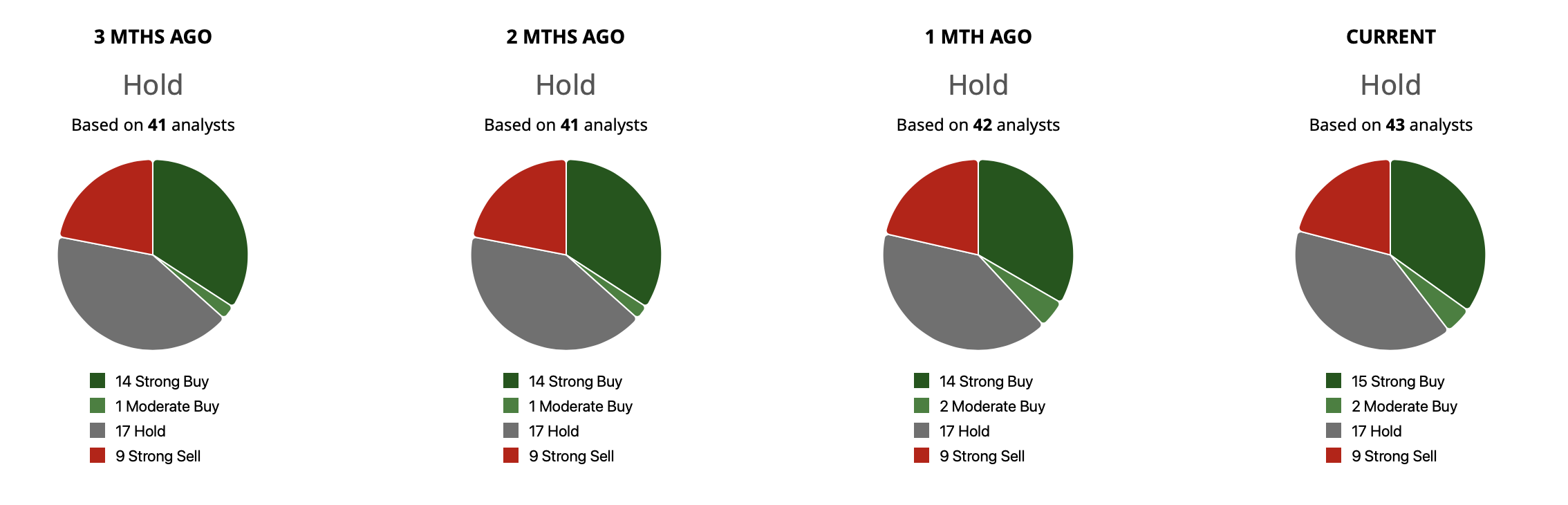

What Do Other Analysts Say About TSLA Stock?

Of the 43 analysts covering TSLA stock, 15 analysts have a “Strong Buy,” two have a “Moderate Buy,” 17 analysts offer a “Hold" rating, and nine have a “Strong Sell.” The mean target price of $408.42 implies roughly 6% potential upside from current levels. Meanwhile, the high-end target of $600 implies as much as 55% possible growth from here.

In short, the biggest thing investors should watch for Tesla in 2026 is whether it can successfully launch its robotaxi service. If the company delivers on this goal, it could open the door to a massive new market and significantly boost long-term growth. While analysts remain divided on TSLA stock, many agree that autonomous driving and robotaxis could be a game changer.

On the date of publication, Ian Cooper did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Intel%20Corp_%20logo%20on%20mobile%20phone-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

/Apple%20Inc%20logo%20on%20Apple%20store-by%20PhillDanze%20via%20iStock.jpg)

/Starbucks%20Corp_%20logo%20by-%20eyewave%20via%20iStock.jpg)