/AI%20(artificial%20intelligence)/AI%20Infrastructure%20by%20FOTOGRIN%20via%20Shutterstock.jpg)

Nvidia (NVDA) remains one of the most sought-after stocks in the market today, dominating the artificial intelligence (AI) space with its powerful GPUs that train and run advanced AI models. But as AI systems grow more complex, the spotlight is moving beyond compute to how data is stored, accessed, and scaled. And as demand for AI explodes, so does the need for high-performance NAND storage. This is where SanDisk (SNDK) is starting to stand out.

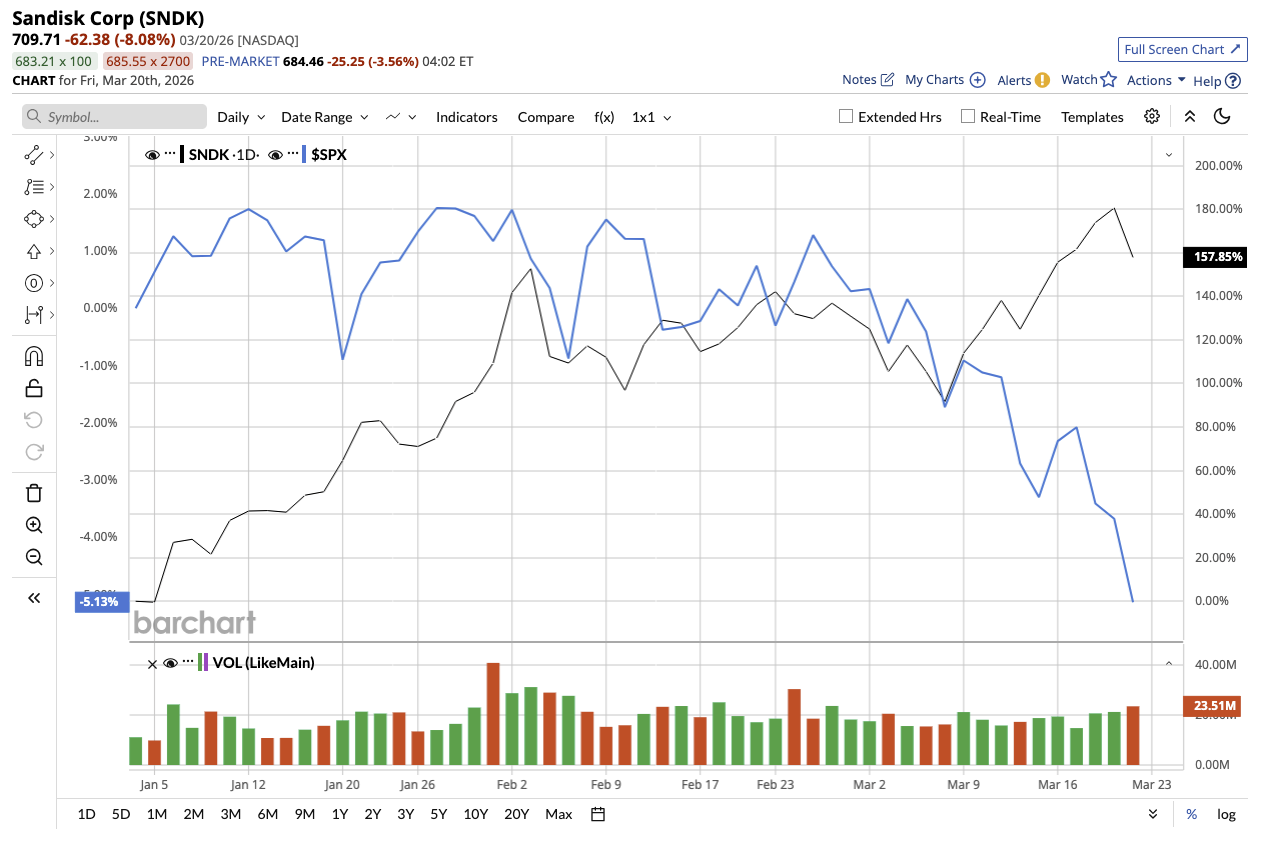

SNDK stock has surged an impressive 195% year-to-date (YTD), even as many AI and tech titans face pressure from market rotation. Could SanDisk become the next Nvidia?

AI Is Reshaping the NAND Industry

AI workloads significantly increase system complexity and storage requirements, making NAND critical to modern computing infrastructure. In the second quarter of fiscal 2026, revenue reached $3.02 billion, an increase of 61% year-over-year (YOY). Looking at segment revenue, edge revenue came in at $1.67 billion (up 21% sequentially), consumer revenue reached $907 million (up 39% sequentially), and data center revenue totaled $440 million (up 64% sequentially). Bits shipped increased 22% YOY, highlighting the strength of underlying demand.

Gross margins rose to 51.1%. Meanwhile, adjusted EPS increased significantly from $1.22 in the prior-year quarter to $6.20 in Q2. Management credited this strong quarter to higher pricing, disciplined cost management, and a strategic allocation of supply to the right opportunities.

One of the most strategic moves in the quarter was SanDisk’s extension of its joint venture with Kioxia (KXIAY) through 2034. This extension will allow continued access to large-scale, cost-efficient NAND production, supporting its long-term supply capabilities. As part of the agreement, Sandisk will pay $1.16 billion for manufacturing services between 2026 and 2029. Capital expenditures totaled $525 million in the quarter to support advanced manufacturing and future capacity. While Sandisk continues to invest in long-term growth, its balance sheet and cash flows remain healthy. SanDisk earned $843 million in adjusted free cash flow during the quarter, which enabled it to pay off $750 million in debt, leaving it with $1.54 billion in cash.

Outlook Points to Continued Upside

On the earnings call, management stressed that the NAND storage sector is becoming more predictable as a result of large investments in AI infrastructure. SanDisk is profiting on this demand by focusing on critical customers and multi-year agreements. SanDisk's forward guidance, which suggests that momentum is far from slowing down, is what uplifted investors' confidence in the stock.

For Q3, the company expects revenue between $4.4 billion and $4.8 billion, an increase of 170% YOY at the midpoint. Adjusted EPS is expected to reach between $12 and $14, which is a drastic improvement from a loss of $0.30 in the prior-year quarter. Gross margins are projected to expand further to range between 65% and 67%.

Analysts expect SanDisk to report exceptional numbers for the next two fiscal years. Revenue is expected to increase by 112% in fiscal 2026, followed by 72% growth in fiscal 2027. Earnings are expected to increase by 1,247% and 118% over the next two fiscal years. SNDK stock currently trades at 25.8 times forward earnings.

The Quiet Backbone of the AI Boom

Dethroning Nvidia might not look possible anytime soon, given its deep lead in AI chips, software ecosystems (like CUDA), and strong relationships with hyperscalers. Its dominance is built on an entire AI stack that competitors are still trying to match.

SanDisk doesn’t need to beat Nvidia at compute. It can grow alongside it by becoming essential to AI infrastructure. Over the next decade, if it continues securing long-term contracts and capitalizing on AI-driven data growth, it can become an equally strong AI stock.

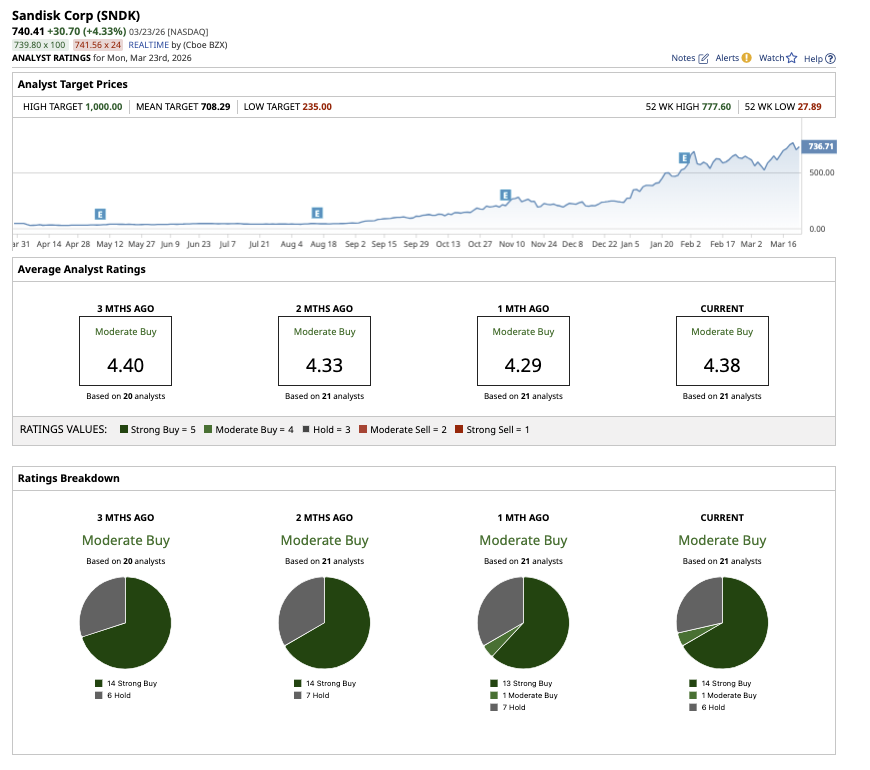

Overall, Wall Street seems moderately bullish about SNDK stock. Of the 21 analysts covering the stock, 14 recommend a “Strong Buy,” one rates it as a “Moderate Buy,” and six suggest a “Hold” rating. The stock is close to surpassing the average price target of $709.22. However, the Street-high estimate of $1,000 indicates that the stock could gain as much as 41% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

/Qualcomm%2C%20Inc_%20logo%20on%20phone-by%20viewimage%20via%20Shutterstock.jpg)

/Advanced%20Micro%20Devices%20Inc_%20logo%20and%20chart%20data-by%20Poetra_%20RH%20via%20Shutterstock.jpg)