Over the past few years, the Magnificent Seven have dominated the market, with artificial intelligence becoming the biggest growth engine behind the group’s rally.

That debate now centers on Nvidia (NVDA) and Amazon (AMZN) after Nvidia just said it will sell 1 million AI chips and other products to Amazon Web Services (AWS) by the end of 2027, which tells how deeply the two companies are tied to the next phase of AI demand. For Nvidia, the deal reinforces its grip on the chip market. For Amazon, it highlights the scale of its cloud AI ambitions and the growing importance of AWS in the AI race.

Investors are now weighing which tech giant, NVDA or AMZN, has the more compelling growth story. Although both stocks carry consensus “Strong Buy” ratings on Wall Street.

The Bull Case for Nvidia

Nvidia is the pure-play AI compute leader. It dominates high-end GPUs for data centers, and its latest architectures, Blackwell and Vera Rubin, power generative AI models. In Q4, it hauled in $62.3 billion in data-center revenue, up 75% from a year earlier, and its fiscal 2026 data-center sales hit roughly $197.3 billion. CEO Jensen Huang says computing demand is “growing exponentially,” and enterprise adoption of AI agents is “skyrocketing,” as customers race to build AI factories. NVDA’s gross margins remain near 75%, reflecting its pricing power.

Nvidia’s financial momentum is stunning. Quarterly net income was $42.96 billion, showing an impressive 94% growth year-over-year (YoY), and full-year revenue of $215.9 billion was up 65% YoY. The company forecasts continued strength, and it guided Q1 FY2027 sales to about $78 billion, an all-time high. NVDA also returned $41 billion to shareholders in FY2026 through buybacks/dividends.

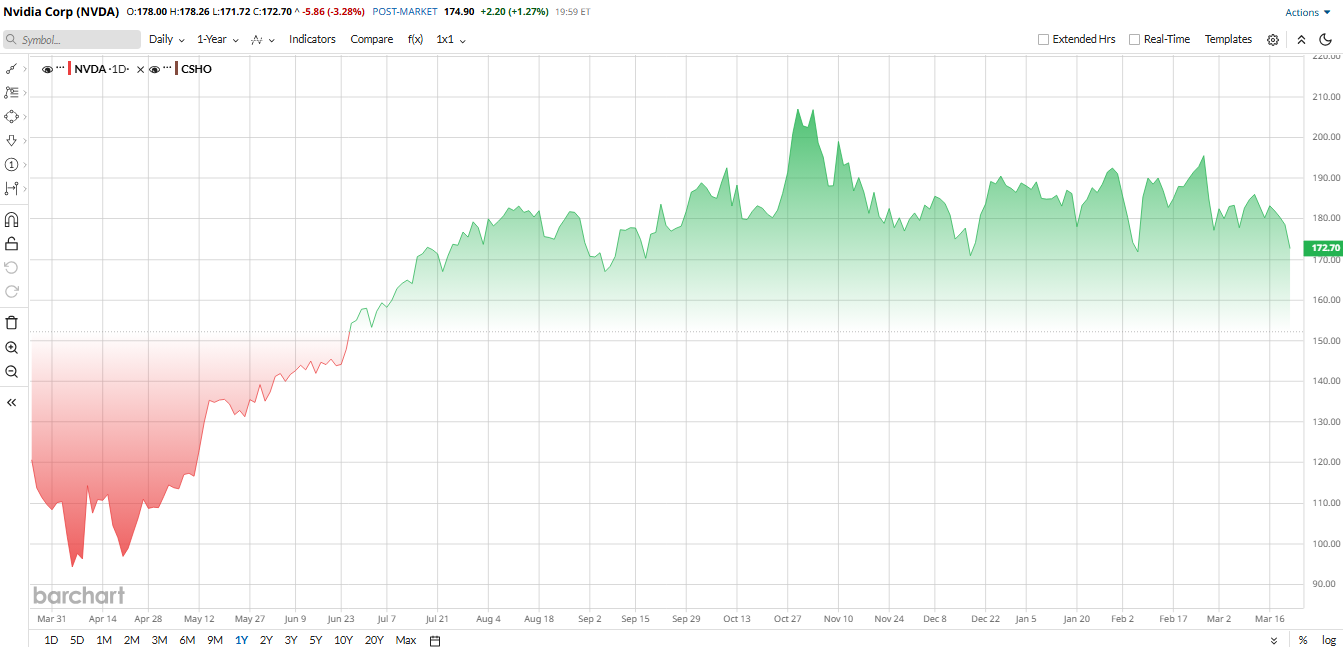

Valued at currently nearly $4.2 trillion by market cap, NVDA stock has roughly doubled over the past two years on this growth. At current prices, Nvidia trades in the early 20s of forward P/E, which is cheaper than its 5-year average, plus analysts note its opportunity is equally colossal. The AWS deal itself aligns with NVDA’s own $1 trillion addressable-market goal for next-gen GPUs by 2027.

From an AI perspective, Nvidia’s moat is clear. Its GPUs are the workhorses of modern AI training and inference. The AWS agreement deepens Nvidia’s partnership with the world’s largest cloud provider. AWS plans to use a mix of Nvidia chips, including the new Groq inference chips acquired in late 2025, along with Nvidia’s ConnectX and Spectrum networking cards. This shows that major customers still rely on Nvidia’s ecosystem; as one NVDA exec put it, “Inference is wickedly hard… to be the best at inference, it is not a one-chip pony.”

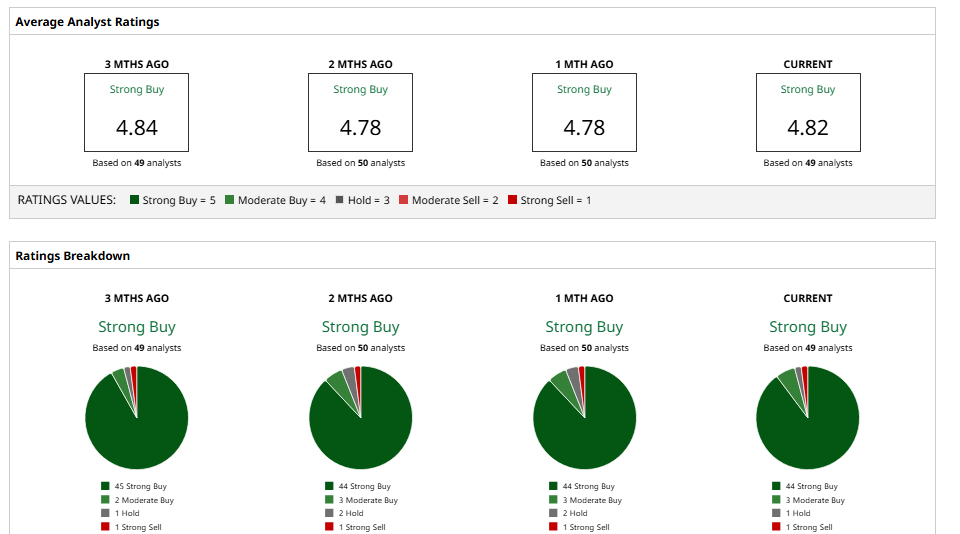

Wall Street looks highly bullish on NVDA stock. The group of 49 analysts has a consensus “Strong Buy” rating with a mean price target of roughly $269, which suggests almost 56% upside from here.

So it's like, NVDA looks set to capture a large share of the multi-year AI computing investment, cementing its role as a core AI platform for organizations.

The Bull Case for Amazon

Amazon offers a broader tech franchise anchored by cloud, e-commerce, ads, and AI. Its AWS unit, the key AI infrastructure play, is still growing at a healthy clip. In its latest quarterly results, AWS revenue rose 24% to $35.6 billion. AWS has also expanded partnerships with AI leaders, e.g., OpenAI and Anthropic, and is deploying its own chips. Amazon’s Trainium/Graviton custom processors now have a run rate of up to $10 billion and train over 500,000 AI chips in production. Amazon’s CEO Andy Jassy says this momentum, plus gains in advertising and store sales, will justify a staggering $200 billion of capital spending in 2026, aimed mainly at AI, chips, and next-gen services.

Operationally, Amazon’s numbers are equally solid. Q4 net sales were $213.4 billion, with North America up 10% and international up 17%. Operating income jumped to $25 billion, and net income was $21.2 billion. For the full year 2025, Amazon’s revenue hit a record $716.9 billion, up 12%. AWS's operating profit grew to $45.6 billion compared to $39.8 billion in 2024, clearly showing improved scale. Although heavy AI capex cut free cash flow to $11.2 billion vs. $38.2 billion prior year, Amazon has ample cash and a $2.3 trillion market value.

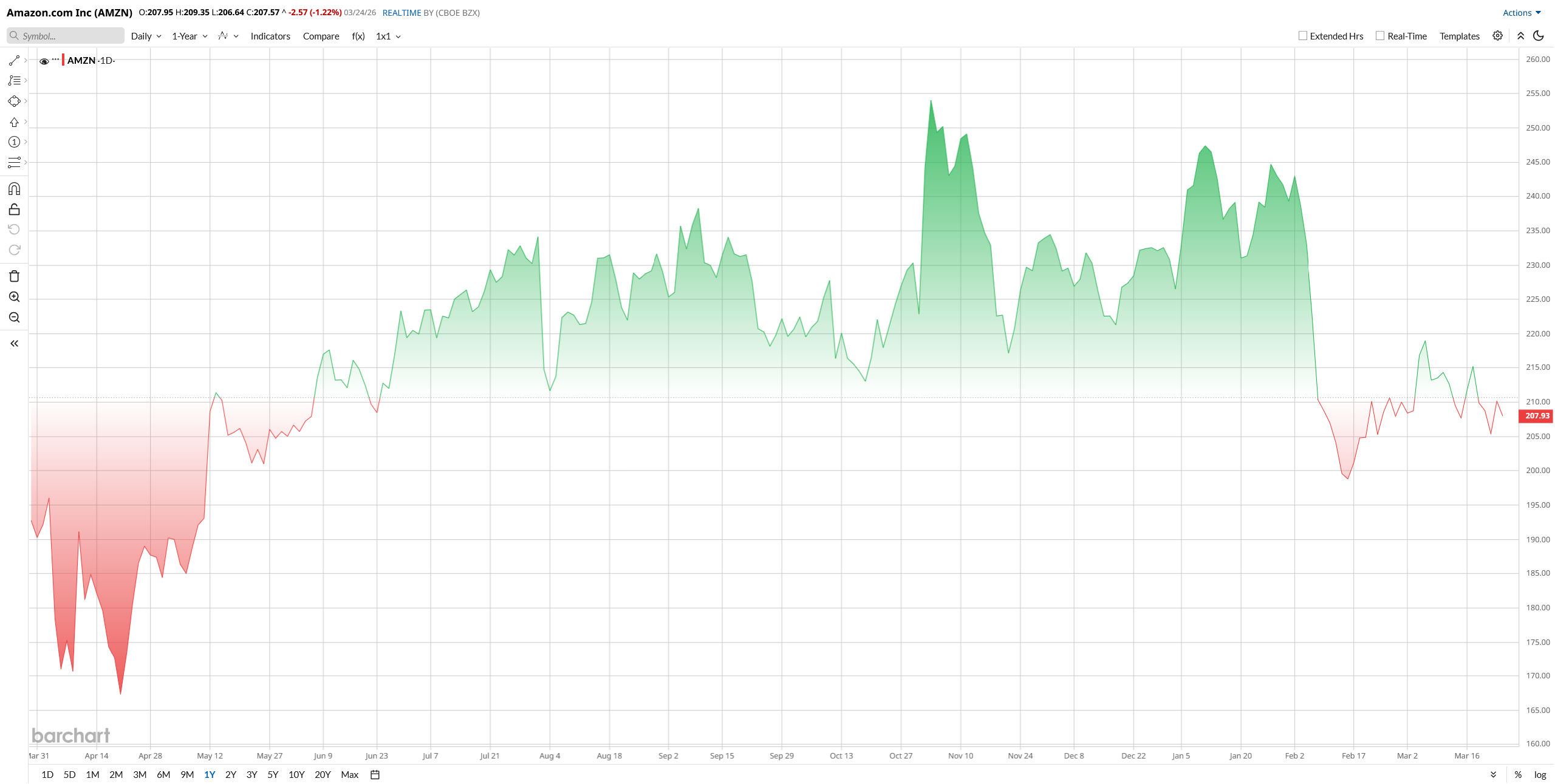

In terms of stock performance, Amazon looks like a slow ride here. After gaining some decent gains in 2025, shares of AMZN gave up in 2026, now down 10% year to date (YTD). Despite this, they are trading more expensively than Nvidia at 26 forward earnings and at a price/sales near 3x. Its growth outlook is slower, like in mid-teens revenue CAGR, but steadier. Amazon’s advantages lie in its diversification, e.g., its retail and Prime generate huge cash flows, and AWS is becoming the backbone of AI services.

Some investors view AMZN as a safer “growth at scale” stock, as it may not double as fast as NVDA, but its broad businesses offer a different risk profile. If AI spending grows as expected, AWS’s share should rise, but even if AI spending plateaus, Amazon’s dominant retail/ads and improving margins could sustain its stock.

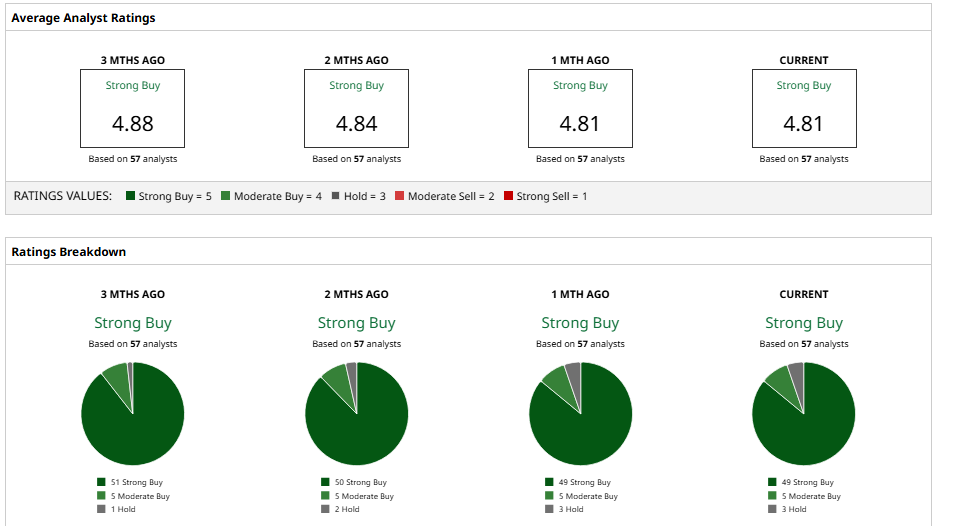

Like Nvidia, AMZN also has a full vote of confidence from Wall Street and has a consensus “Strong Buy” rating. The bullish group has set a mean price target of $284.75, which suggests 39% upside potential.

The Verdict

In my opinion, both companies are deeply tied to AI. NVDA is the pure-play enabler with sky-high growth, while AMZN is a sprawling tech giant building AI infrastructure alongside its other businesses. I think investors must weigh Nvidia’s high-octane expansion against Amazon’s diversified but steady model.

Each is “magnificent” in its own right; the better buy depends on whether you prioritize maximal AI upside or broad-based resilience.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Quantum%20Computing/A%20concept%20image%20showing%20a%20ray%20of%20light%20passing%20through%20cyberspace_%20Image%20by%20metamorworks%20via%20Shutterstock_.jpg)

/International%20Business%20Machines%20Corp_%20logo%20on%20storage%20rack-by%20Nick%20N%20A%20via%20Shutterstock.jpg)

/Palo%20Alto%20Networks%20Inc%20HQ%20sign-by%20Sundry%20Photography%20via%20Shutterstock.jpg)