The Richardson, Texas-based Lennox International Inc. (LII) designs, manufactures, and sells heating, ventilation, air conditioning, and refrigeration products. It serves residential and commercial markets with climate-control systems, equipment, and services, reaching customers through direct sales, dealers, and company-operated stores.

With a market cap of nearly $16.3 billion, the company sits in the “large-cap” bracket, a space reserved for companies valued above $10 billion. The scale typically signals operational depth, steady demand patterns, and a well-entrenched competitive footing.

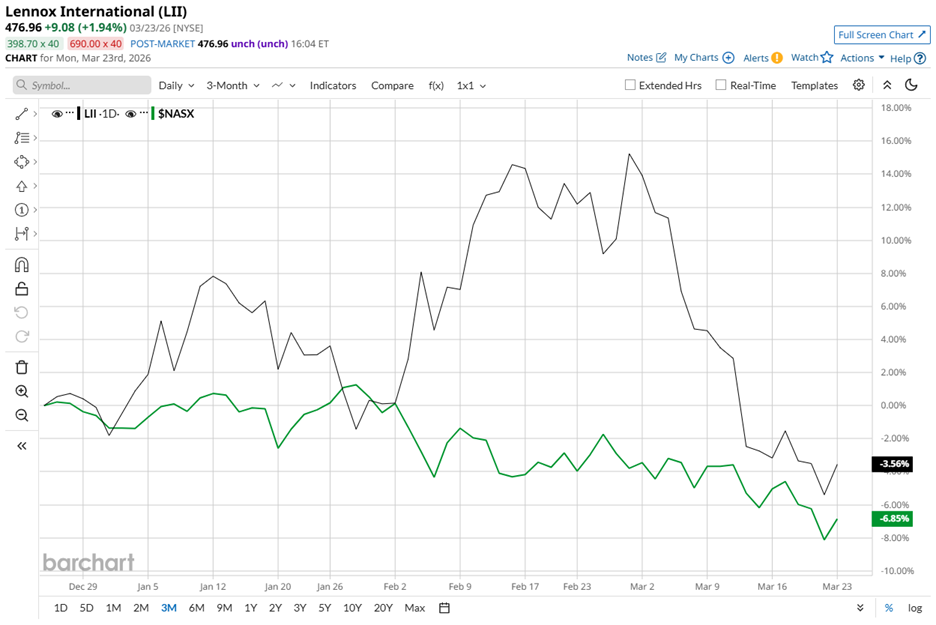

Shares currently trade 30.8% below their 52-week high of $689.44 reached in July 2025. Over the past three months, the stock has slipped 3.6%, yet it has held up better than the broader Nasdaq Composite ($NASX), which is down 6.9% over the same stretch.

Over the past 52 weeks, LII stock has declined 16.3%, sharply lagging the Nasdaq’s 23.4% gain and reflecting a clear loss of momentum. The tone has carried into 2026, with Lennox’s shares slipping 1.8% year-to-date (YTD), even as the broader index has dropped a steeper 5.6%.

From a technical standpoint, the stock has been trading below its 50-day moving average of $522.45 and its 200-day moving average of $537.69 since the start of the month, indicating that near-term sentiment remains defensive.

Fundamentals, too, have shown strain. On Jan. 28, Lennox reported Q4 fiscal 2025 revenue of $1.20 billion, down 11.2% year over year and below the $1.27 billion analyst estimate. Adjusted EPS came in at $4.45, missing Street's forecast of $4.72 and marking a 22.2% decline from the prior year’s period.

Weakness across both residential and commercial HVAC markets weighed on performance, pulling results below Wall Street’s bar. Yet the market did not turn its back. While the stock plunged 2.3% on the day of announcement, it edged up 1.8% in the following trading session, suggesting investors found something to hold onto.

The anchor came in the form of record profitability, as Lennox delivered annual margins above 20% for the first time in its history. Looking ahead, management projects fiscal year 2026 revenue to grow 6% to 7%, with acquisitions contributing roughly 4% of that lift. Adjusted EPS is guided to a range of $23.50 to $25.

Relative performance adds another layer of perspective. Lennox’s rival, Trane Technologies plc (TT), has gained 22.4% over the past year and is up 9.2% YTD, highlighting how peers have navigated the same environment with a stronger footing.

Even so, Wall Street appears willing to give Lennox the benefit of the doubt. Among 19 analysts, the consensus rating stands at “Moderate Buy.” The average price target of $562.60 signals potential upside of 18% from current levels, suggesting that while the road has been uneven, the broader narrative may still have room to turn.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)