With a market cap of $11.7 billion, The Trade Desk, Inc. (TTD) is a technology company that operates in the United States and internationally, specializing in digital advertising solutions. It enables advertisers and agencies to create, manage, and optimize data-driven campaigns across multiple formats such as connected TV (CTV), video, display, audio, and native ads on various devices.

Companies valued at $10 billion or more are generally labeled as “large-cap” stocks, and Trade Desk fits this criterion perfectly. Headquartered in Ventura, California, the company also provides data and value-added services to support effective advertising strategies.

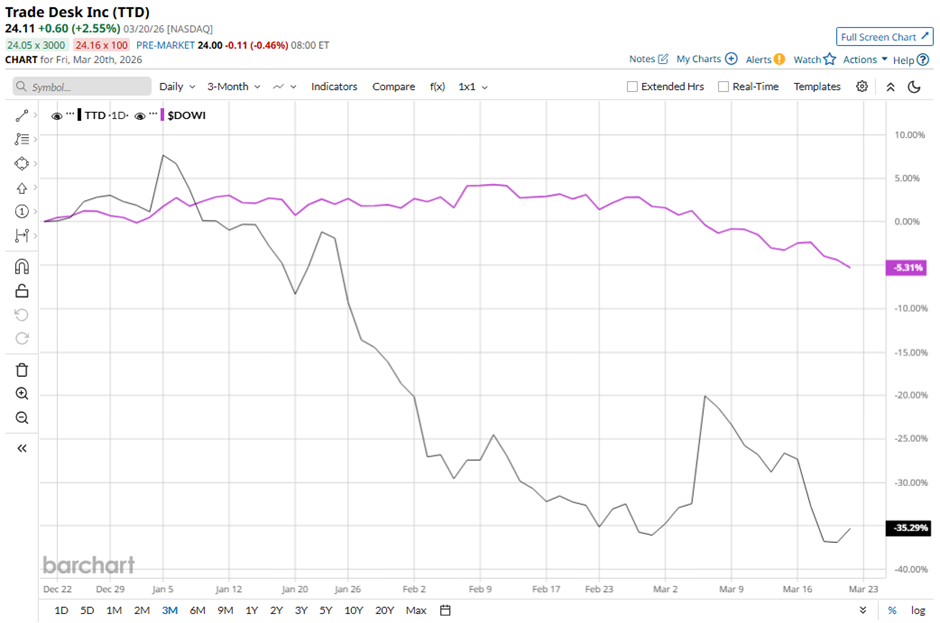

Shares of Trade Desk have plunged 73.6% from its 52-week high of $91.45. The stock has decreased 35.3% over the past three months, underperforming the broader Dow Jones Industrials Average's ($DOWI) 5.3% drop over the same time frame.

Longer term, shares of the adtech company have tumbled 56.8% over the past 52 weeks, lagging behind DOWI’s 8.6% return over the same time frame.

Despite a few fluctuations, the stock has been trading below its 50-day and 200-day moving averages since last year.

Trade Desk has underperformed due to intense competition from dominant digital ad platforms like Alphabet Inc. and Amazon, limiting its role as a primary advertising platform.

Additionally, Trade Desk shares fell 4.8% following its Q4 2025 results on Feb. 25 due to a weaker-than-expected Q1 2026 outlook, with projected revenue of at least $678 million and adjusted EBITDA of about $195 million. Despite beating estimates with Q4 revenue of $847 million (up 14% year-over-year) and adjusted EPS of $0.59, investors were concerned about margin compression, as net income margin dropped to 22% from 25% year-over-year.

In comparison, rival Omnicom Group Inc. (OMC) has shown less pronounced decline than TTD stock. OMC stock has fallen 7.1% on a YTD basis and nearly 7% over the past 52 weeks.

Despite TTD’s weak performance, analysts remain moderately optimistic about its prospects. Among the 38 analysts covering the stock, there is a consensus rating of “Moderate Buy,” and the mean price target of $31.94 suggests a premium of 32.5% to current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)