Howdy market watchers!

Spring has sprung and it feels like summer! It has been one of the wildest weather March’s in recent memory with snow flurries and freezing temps to start the week only to be followed by highs in the mid-90s to finish the week. The transition between seasons can always bring volatility, but this year has been particularly so.

The ‘excursion’ in Iran is entering its fourth week and while political rhetoric from both the US and Israel suggests it is just about over, new threats emerge from the crippled Iranian regime. While such threats may indeed be empty, they warrant heeding with a military style ruling group that is literally fighting for their existence. Continued attacks on neighboring Middle East countries have caused greater unity in the cause of much of the region against the Iranian regime.

A major attack on a natural gas facility in Qatar this week, which represents four percent of global production and is said to potentially take 5 years to repair, brought about enhanced uncertainty for fertilizer production from the region and escalating global nitrogen prices, in particular. European natural gas prices have surged given its import dependence, but US natural gas prices have actually tamed with ample inventory from warmer temperatures and slow exports putting downward pressure on US prices.

And yet, US fertilizer prices continue to push higher. While natural gas is used globally, it is traded much less as a global commodity given the export markets are more fragmented than other oil, for example. This presents a huge opportunity for the US to become a much more meaningful exporter of natural gas to take advantage of the large price arbitrage to Europe especially, but only recently have US natural gas exports been emphasized and invested in and so it takes time to get export terminals to the scale that would impact domestic US prices.

There is probably more agreement in the US and around the world for eliminating the Iranian threat, but for now, it is owned by Presidents’ Trump and Israel’s Netanyahu. There is an inordinate level of political division in the US at the present time, which makes the upcoming mid-term elections all the more of a fight. Our allies know this as do our enemies and so the global chess match continues to play out. There is much worthy to fight for, but such uncertainty in the medium term is not welcome news by markets.

We’ve seen greater volatility enter the markets that can ignore fundamentals. Its been a tough four weeks for the equity markets, precious metals and somewhat for the cattle markets with increasing uncertainty from the launch of attacks on Iran. As I wrote last week, the crude oil market holds the key to the rest as it is the front-line barometer of the extent this conflict could escalate and cause broader global turmoil. The fact that WTI crude oil has managed to remain below $100 per barrel has been surprising, but this is not over yet despite many attempts to reassure and reopen the key, global trade artery. It seems every Friday we close strong as the Strait of Hormuz remains closed and represents 20 percent of global oil flows.

The crude-led rally in grains seemed to unwind a bit on Friday as wheat and corn weakened despite crude’s late session rally. I believe some of this was end-of-week profit taking that we’ve seen throughout the week followed by strong rebounds. There is talk of rains for Oklahoma and Texas wheat areas in the 10-day forecast, but there is a lot of heat between now and then and I believe it could be more east than needed for the main part of the wheat belt. There is also talk of another freeze at the end of March, which would be a market mover. Russia's SovECON also raised its forecast of this year's wheat harvest by nearly 2.0 million metric tons to 87.6 MMT versus USDA's estimated 89.5 MMT.

Key I-state corn areas remain dry ahead of planting. I’m sure the USDA is working to factor in all of these many items ahead of the release of the critical March 31st Planting Intentions Report. It is sure to be a market mover as it usually is.

Corn exports have continued to be strong and soybeans were this week while wheat was at the bottom of expectations. US NOPA soybean crush reports this week showed phenomenal domestic demand for soybeans, which comes at a pivotal time with China purchase commitments questionable after President Trump this week delayed his end of the month trip to Beijing.

The US dollar has been stubbornly elevated in recent weeks with the ongoing conflict. The Federal Reserve’s FOMC held rates steady this week given inflation concerns with more tongue-in-cheek comments of the word ‘transitory’ for the recent energy hike flowing through to the economy. The US Producer Price Index released this week measuring wholesale prices for February rose 0.7 percent versus 0.3 percent expected. Inflation in wholesale prices will begin to factor through to consumer price inflation in time and can cause demand issues especially with higher gas prices tightening monthly budgets.

Much depends on the price of oil and more importantly, the ‘duration’ of higher prices. If oil prices stay steady and begin to weaken, I think the markets could ‘absorb’ the risks from these ongoing tensions and get back to regular business. The opposite scenario of elevated energy prices for longer begins to concern me for the broader economy as well as the cattle market indirectly through consumers.

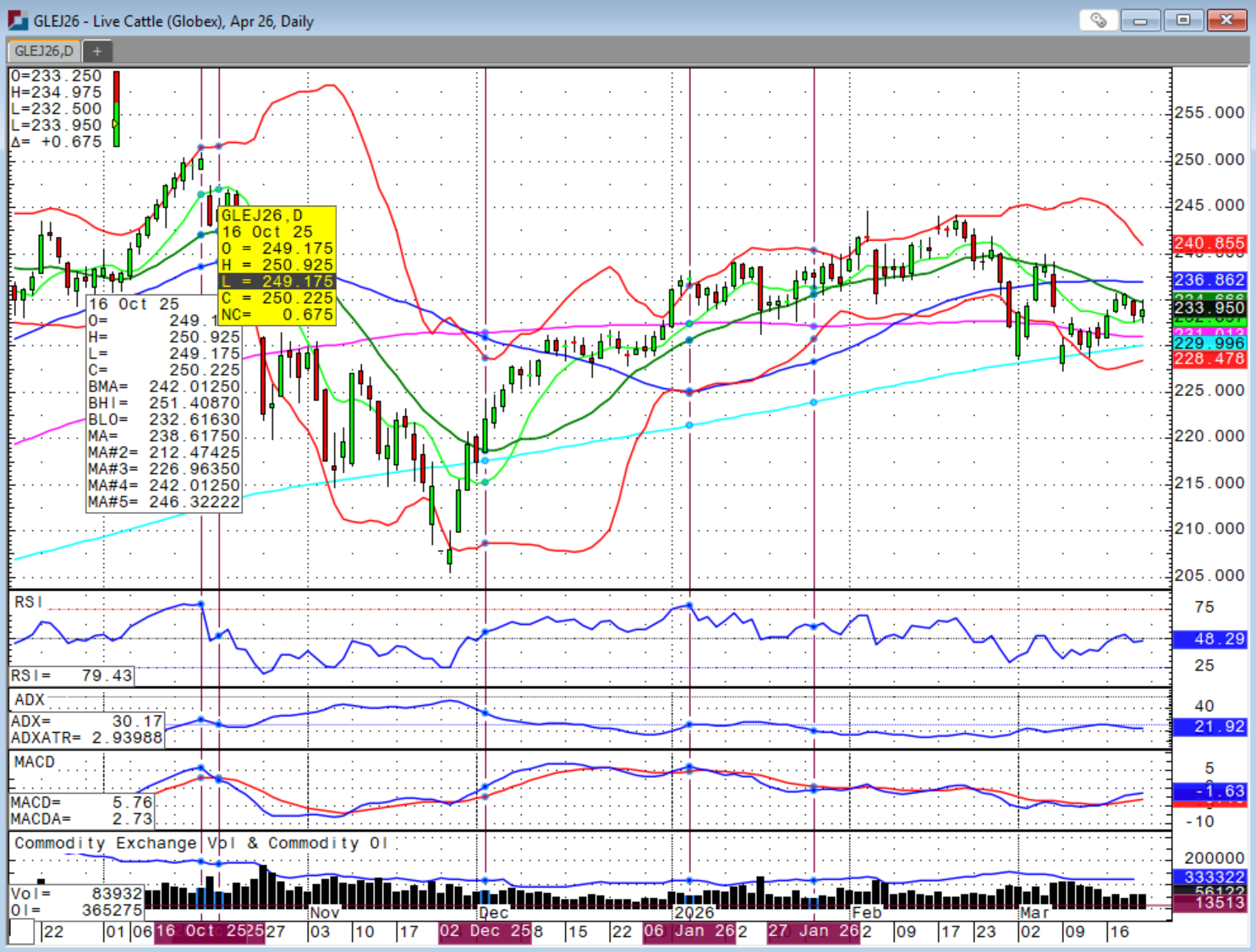

In the cattle markets, it does indeed seem that the JBS Greeley packing facility strike that officially began on Monday was already priced into the market. In fact, with all that is going on in the world and with the US equity market, cattle have held up relatively well. Fed cattle cash trade returned this week with large numbers, but still at the $235 level. However, it was not lower as we’ve seen in recent weeks, but we are looking for higher trade before calling this a bottom.

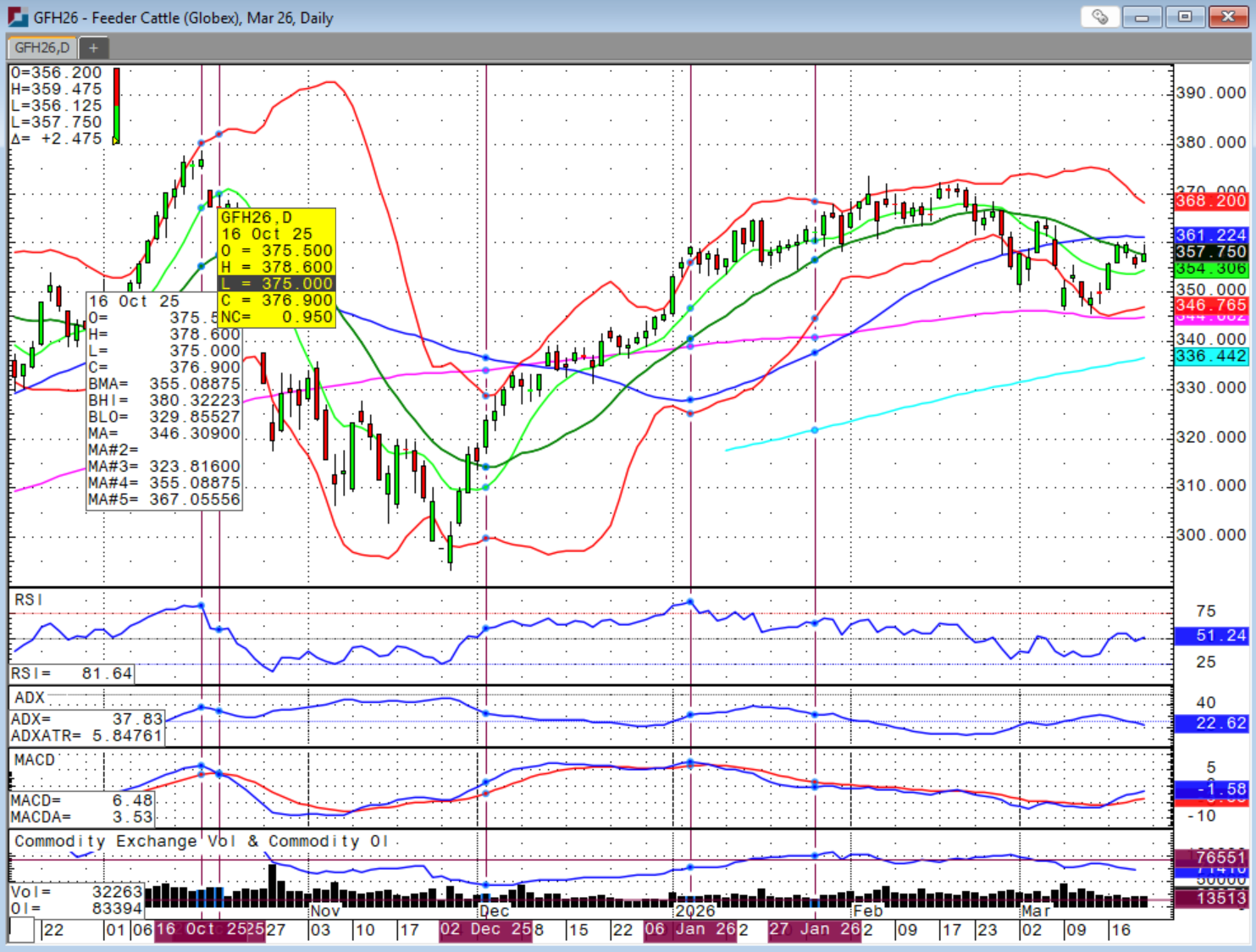

Sale barns continue to be on fire, especially for light weight calves for grass. The money being spent on cattle right now embeds optimism that prices are going higher, but also absolute fear of the amount of dollars on the table if it doesn’t. There are calves being purchased that cannot be protected at breakeven levels even if you choose the highest LRP or at-the-money put option. Frankly, I don’t like spending risk management money if you cannot protect at least a breakeven. Now, those could be famous last words I know, but markets will fluctuate.

However, if you’re buying at a level where breakevens cannot be protected, but then it can in a couple weeks if we extend this rally, be judicious and don’t watch it come and go. Do something at least on a portion of your total exposure. If you believe markets are going to go higher, you can always start with 10 percent or 20 percent and then continue to add or roll up protection if and when the market rallies further. However, if it doesn’t due to an unexpected, Black Swan event or headline or political rhetoric, which is absolutely possible in today’s environment, you will have some protection.

Today’s markets are different than when I started. Profit opportunities come and then immediately disappear, it seems. It is not fair and mostly, not justified given fundamentals, but it is how the markets work. As they say, “a bird in hand is better than two in the bush” and that seems truer these days than ever before.

USDA’s monthly Cattle on Feed report was released at 2 PM on Friday. March 1st on-feed numbers came in at 99.8 percent of last year versus 99.3 percent expected by the trade and so above expectations. Placements for February were reported at 103.7 percent versus 100.2 percent expected, which was noticeably higher than anticipated. However, marketings in February were higher than expected at 93.2 percent versus 92.6 percent expected by the analysts. While placements and total on-feed were both higher than expected, the return of fed cattle cash trade and spring and summer demand ahead could shift the market focus on the uptick in sales.

Fed cattle cash trade topped out at $236 in Kansas on Friday while $235 traded in Texas, Colorado and Nebraska. I believe we could see higher cash trade next week after this week’s steady pricing versus last week.

Much attention will be paid to headlines out of the Middle East this weekend and the impact on crude oil prices and the spillover to stocks and cattle. Futures had a decent week with all contracts holding above the respective 9-day moving averages and several closings at the 20-day moving average.

If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. He can be reached at (580) 232-2272 or at brady@sidwellstrategies.com. Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/The%20sign%20for%20Marvell%20Technology%20out%20front%20of%20a%20corporate%20office%20by%20Valeriya%20Zankovych%20via%20Shutterstock.jpg)

/Intel%20Corp_%20badge%20holder-by%20hasrul_rais%20via%20Shutterstock.jpg)