Investing is about picking the right stocks and avoiding the wrong ones. While some companies are capitalizing on powerful trends, others continue to struggle despite industry tailwinds. Before I dive into the one stock I’d buy today, let’s talk about the one I would stay away from.

One I Wouldn’t Touch: Aurora Cannabis

I have always been supportive of the cannabis industry even though it suffers from tight regulations, inconsistent profitability, and evolving consumer demand. The long-term opportunity of the cannabis industry is undeniable. As legalization expands and social stigma fades, experts believe it has the potential to be worth $1.43 trillion by 2034. However, not every company in a promising industry is worth investing in. And when it comes to Aurora Cannabis (ACB), its long-term track record raises serious concerns.

Aurora once stood as one of the most promising players in the cannabis boom. Investors were drawn to its aggressive expansion strategy, global ambitions, and early-mover advantage. But what followed was a prolonged period of self-destruction.

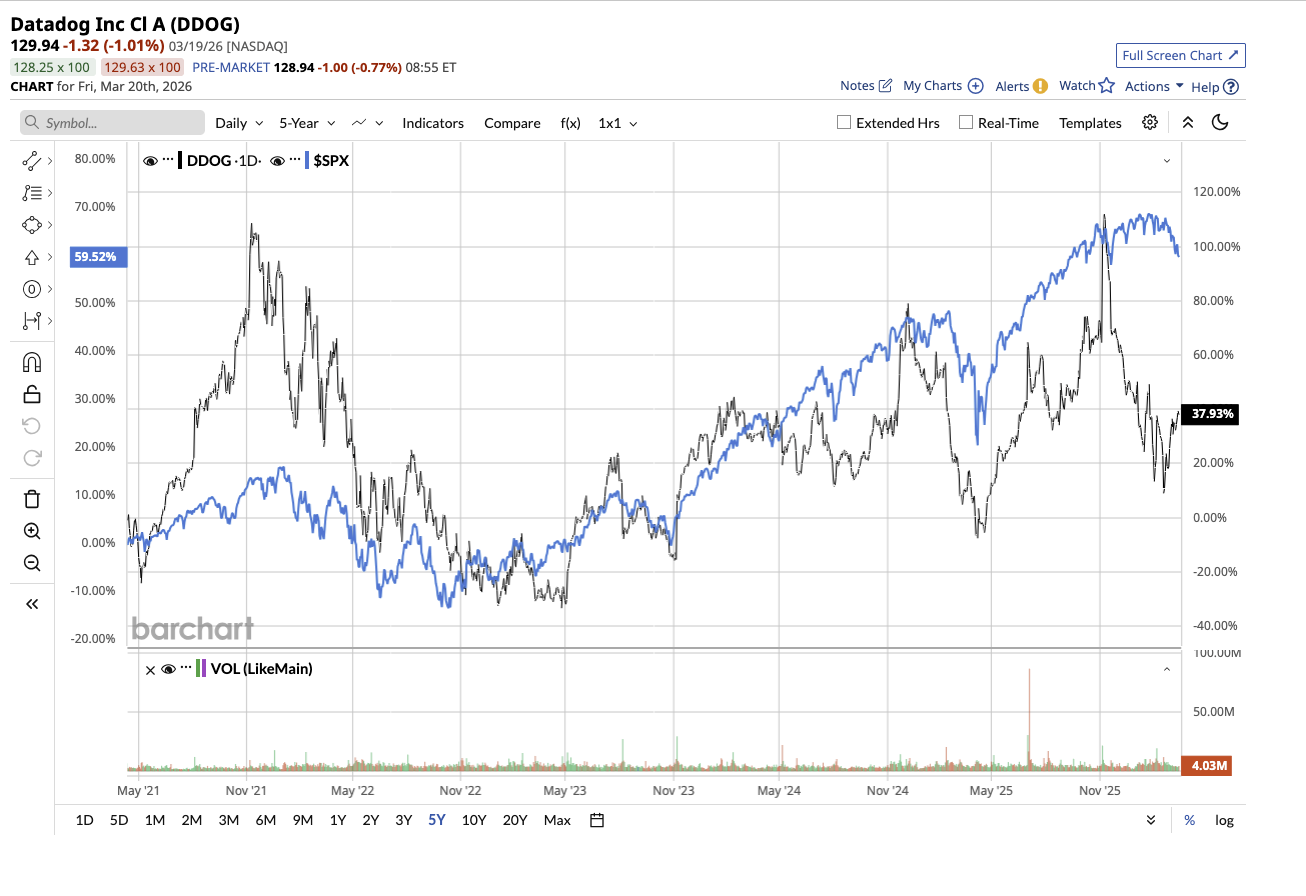

Over the past five years, ACB stock has collapsed 96.3%, dramatically underperforming the S&P 500 Index ($SPX), which has gained 66.2% over the same period. The decline became so severe that the company came dangerously close to being delisted from the Nasdaq after its share price fell below the $1 minimum requirement for an extended period. To remain listed, Aurora executed a reverse stock split, artificially increasing its share price. Aurora has been trying hard to bounce back. In the recent Q2 of fiscal 2026, net revenue grew 7% year-over-year (YOY) to $94.2 million. Global medical cannabis income increased by 12%, with a 17% growth in overseas markets.

But dig deeper, and you see that most of this revenue is from medical cannabis, which accounted for 81% of total revenue. Meanwhile, the consumer cannabis business is collapsing, with revenue down 48% YOY, as the company deliberately exits lower-margin areas. Profitability looked better in the quarter for a company that has long struggled to achieve it. Adjusted EBITDA totaled $18.5 million, with net income of $7.2 million. Also, the company generated free cash flow of $15.5 million.

However, much of Aurora's profitability came from cost cuts, favorable sales mix in high-margin medical markets, and operational improvements. This profitability did not stem from strong demand across multiple segments. The other factor that concerns me is that Aurora’s growth is not in its control. Its future heavily depends on regulatory developments, particularly in markets like Germany, which is its biggest international growth driver.

Furthermore, Aurora ended the quarter with $154.4 million cash and investments and no debt. Nonetheless, it launched a new at-the-market (ATM) equity program to raise up to $100 million. It appears Aurora hasn’t learned from its mistakes, as it continues to follow its old pattern of raising capital through equity issuance. For investors, this increases the risk of dilution, something Aurora has always done.

I won’t deny that Aurora Cannabis is executing better than it has in years. Its recent quarters have shown a clear strategy of focusing on global medical cannabis, exiting lower-margin segments, and expanding in Europe and Australia. However, the company relies heavily on one growth engine, while still operating in a highly uncertain regulatory environment. And there is always the risk of dilution.

For me, this is one cannabis stock I simply wouldn’t touch.

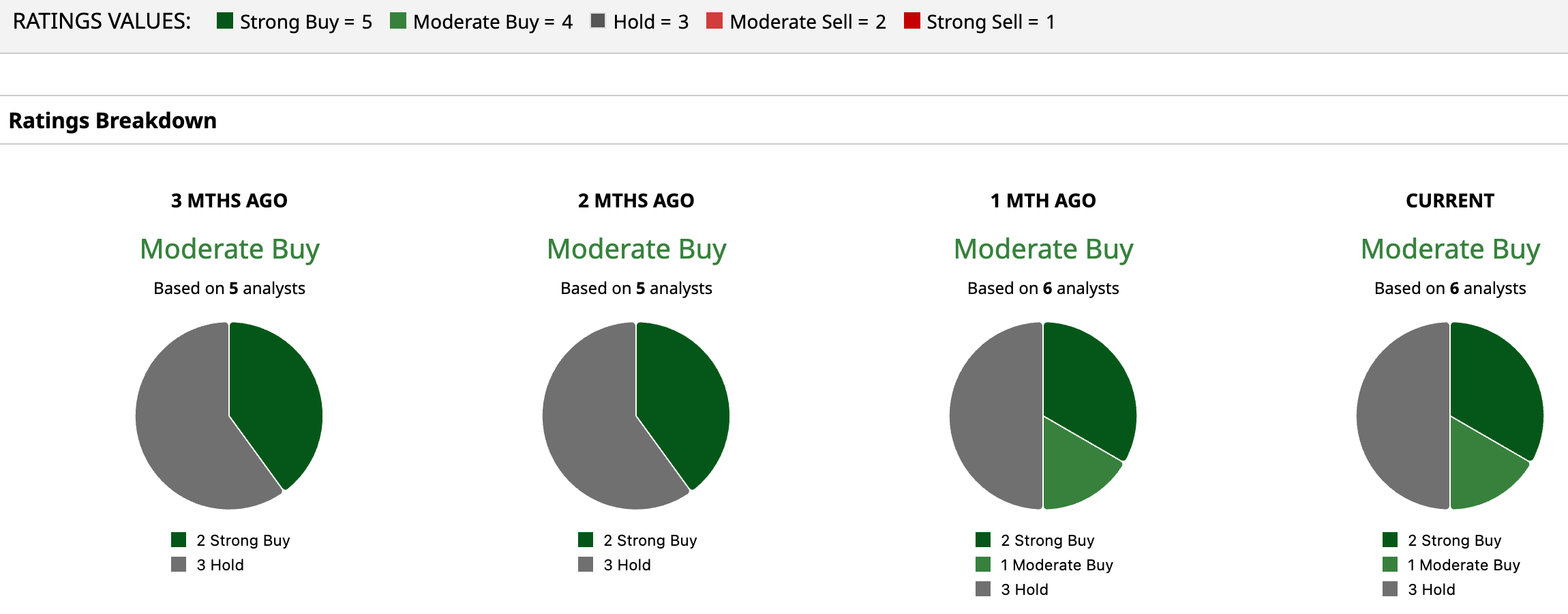

Nonetheless, Wall Street remains cautiously optimistic, rating Aurora Cannabis stock an overall “Moderate Buy.” Out of the six analysts covering the stock, two rate it a “Strong Buy,” while one rates it a “Moderate Buy,” and three say it is a “Hold.” Its average target price of $5.49 suggests the stock can climb 66.9% from current levels. Plus, its high target price of $6.99 implies a 112.5% upside potential over the next 12 months.

One Stock I’d Buy Today: Data Dog

The biggest winners in tech are often the ones powering the infrastructure behind them. As cloud computing and artificial intelligence (AI) continue to reshape the digital economy, companies that help businesses monitor, secure, and optimize their systems become increasingly important. That’s exactly where Datadog (DDOG) stands out and why this is one stock I’d buy today.

Datadog is a cloud monitoring and analytics platform that helps companies keep their software systems running smoothly. And the company is seeing real monetization from AI adoption. The firm now has over 650 AI-native customers. Over the past five years, Datadog stock has risen 61.84%, compared to the broader market gain of 66.2%.

In the fourth quarter, revenue increased by 29% YOY to $953 million, driven by a 37% increase in bookings. Gross margin stood at 81% in the quarter. And, most importantly, Datadog's growth is not being driven by a single segment. The company is enjoying success across industries, customer sizes, and product lines. The company recorded a net revenue retention rate of 120%, indicating that customers are sticking.

The good news is that Datadog's growth is accelerating, both from AI and non-AI customers. Enterprise adoption is still in its early stages. Notably, 84% of customers use two plus products, 55% use four or more, and 33% use six or more products. Management specified that many customers are not yet using the full platform, so there is a massive opportunity ahead. Datadog is no longer just a monitoring tool. It is becoming a full-stack platform. Its three core pillars of infrastructure monitoring, log management, and ARM all crossed $1 billion in ARR. Management noted that around half of customers do not utilize all three, indicating a major cross-selling opportunity ahead. In 2025, the company introduced over 400 new features and signed 18 deals worth more than $10 million.

Management expects 18% to 20% revenue growth in 2026. Analysts expect the company’s earnings to increase by 5.6% in 2026, followed by 22% in 2027.

With strong revenue growth, massive enterprise opportunity, real AI-driven demand, strong margins, and cash flows, Datadog is emerging as a strong player in the AI space. For me, this is one stock I’d buy today.

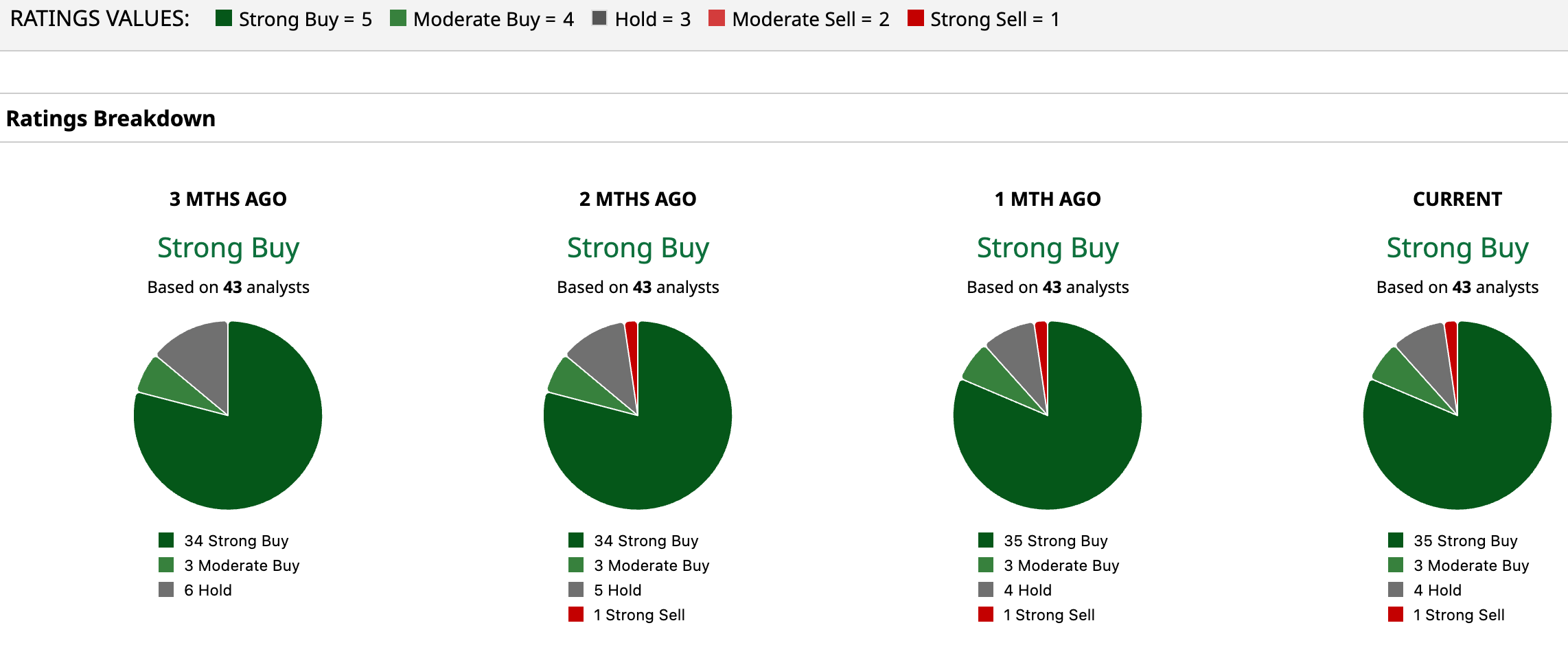

Overall, analysts see Datadog stock as a “Strong Buy.” Among the 43 analysts that cover the stock, 35 rate it a “Strong Buy,” three say it is a “Moderate Buy,” four say it is a “Hold,” and one recommends a “Strong Sell.” Based on its average target price of $183.89, the stock has upside potential of 44.4% from current levels. Plus, its Street-high estimate of $260 implies the stock has upside potential of 104% from current levels.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)