With a market cap of $13.1 billion, Host Hotels & Resorts, Inc. (HST) is a self-managed and self-administered real estate investment trust (REIT) that owns hotel properties and operates through its umbrella partnership structure. Its operations are conducted via Host Hotels & Resorts, L.P., where the company serves as the sole general partner, with a small portion of partnership interests held by outside partners as non-controlling interests.

Companies valued at $10 billion or more are generally labeled as “large-cap” stocks, and Host Hotels & Resorts fits this criterion perfectly. The company distinguishes between its corporate entity and operating partnership primarily based on this minority ownership stake.

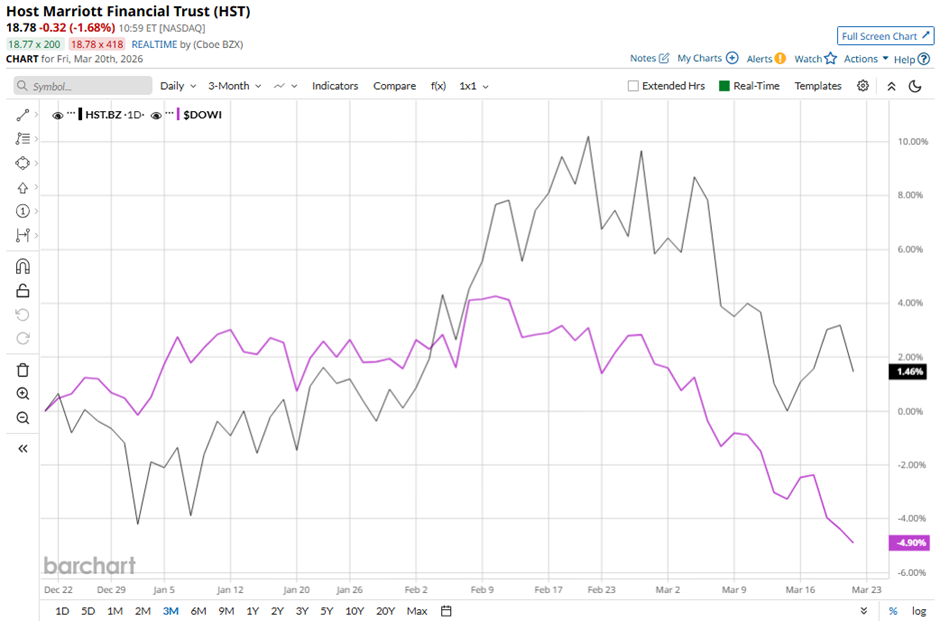

Shares of the Maryland, USA-based company have fallen 10.4% from its 52-week high of $21. HST stock has risen 2.1% over the past three months, exceeding the broader Dow Jones Industrials Average's ($DOWI) nearly 5% drop over the same time frame.

HST stock is up 6.5% on a YTD basis, outpacing Dow Jones' 4.9% decrease. Longer term, shares of the company have increased 26.3% over the past 52 weeks, compared to DOWI’s 9% return over the same time frame.

The stock has been trading above its 200-day moving average since late August 2025.

Host Hotels & Resorts reported strong Q4 2025 results on Feb. 18, including revenue growth of 12.3% to $1.6 billion, net income up 25.7% to $137 million, and adjusted EBITDAre increasing 12.6%. Investor sentiment was further supported by solid full-year 2025 growth, with comparable hotel Total RevPAR up 4.2%, net income rising 9.8% to $776 million. Additionally, optimistic 2026 guidance, projecting RevPAR growth of 2.5% - 4% and net income of $836 million - $891 million, reinforced confidence. However, the stock fell marginally the next day.

In comparison, rival Park Hotels & Resorts Inc. (PK) has lagged behind HST stock. PK stock has declined marginally on a YTD basis and 10.3% over the past 52 weeks.

Despite HST’s outperformance, analysts remain cautiously optimistic about its prospects. Among the 20 analysts covering the stock, there is a consensus rating of “Moderate Buy,” and the mean price target of $21.11 suggests a 12.3% premium to current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)