/Alibaba%20by%20Photo%20Agency%20via%20Shutterstock.jpg)

Alibaba (BABA) released its earnings for the fiscal Q3 2026 yesterday, March 19, before U.S. markets opened. The results fell short of expectations, and the company missed on both the top line and the bottom line. It was incidentally the third consecutive quarter where Alibaba missed estimates, and while the stock had risen after fiscal Q1 2026 earnings on optimism about its artificial intelligence (AI) business, markets seem to have finally had it with the earnings misses.

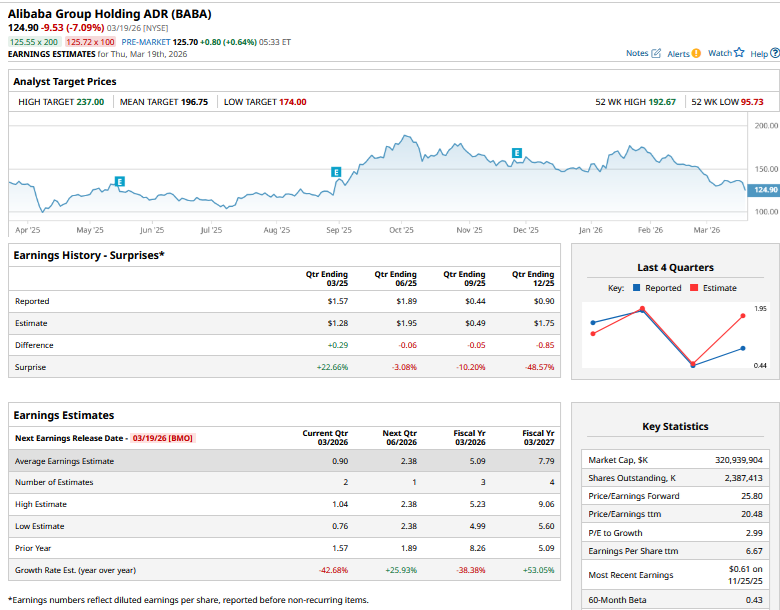

Talking of fiscal Q3, its revenues (after adjusting for disposed assets) rose 9% year-over-year (YoY) to $40.7 billion, which was slightly below estimates. The real miss, meanwhile, came on profit metrics, and its per-share earnings came in at $0.85, which was less than half what analysts were expecting. Notably, markets did not expect much from Alibaba in the December quarter, but the company failed to clear even the low bar, with operating income falling 74% YoY. The company’s profits also plunged in the previous quarter due to growing investments in AI and continued losses in the instant commerce business.

One bright spot in Alibaba’s Q4 report was the 36% YoY rise in cloud revenues, with AI-related revenues rising in triple digits for the tenth consecutive quarter. However, while markets overlooked the dip in profits in the previous two quarters, this time the “AI story” failed to cut ice with investors, who sent the stock south by over 7% yesterday. After the post-earnings slump, BABA stock has extended its year-to-date (YTD) drawdown to over 31%.

While AI-related announcements helped tech stocks rally in the previous three years, markets now want to see adequate earnings growth to justify the massive investments they are making. The story has been playing out in U.S. tech stocks for the last couple of quarters, and it was about time it manifested in China.

BABA Stock Forecast

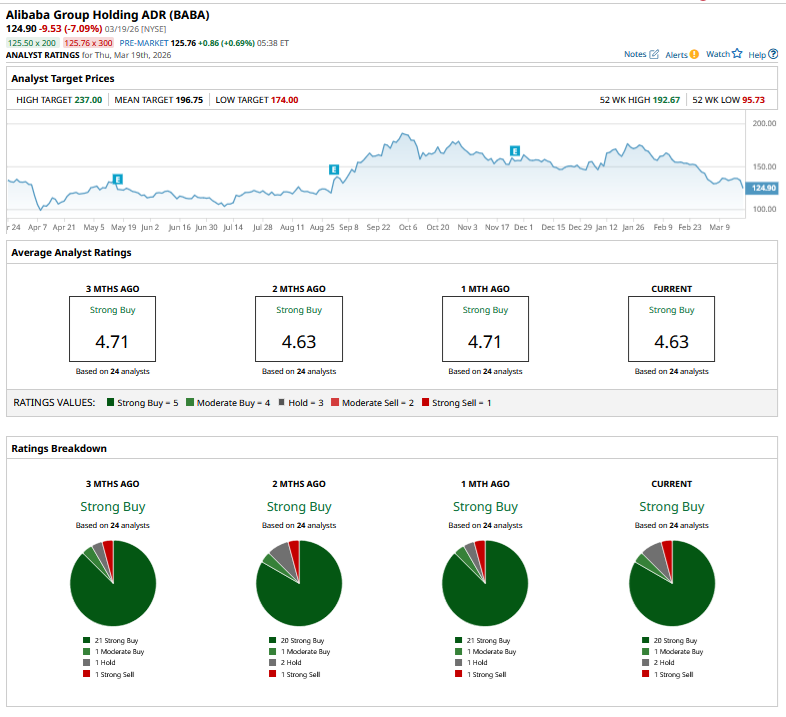

Meanwhile, even as Alibaba’s fiscal Q3 earnings spooked investors, sell-side analysts don’t seem too perturbed. Jefferies lowered the stock’s target price from $225 to $212 but maintained its “Buy” rating, while Bank of America maintained its “Buy” rating and $180 target price on the stock even as it talked about the negative earnings surprise in the quarter. US Tiger Securities upgraded the stock from a “Hold” to “Buy” while cutting the target price by $5 to $175. J.P. Morgan is also bullish on BABA and sees the stock as a “global AI” winner.

Should You Buy BABA Stock?

In my previous article, I had noted that BABA stock looked attractive ahead of the “two sessions” in China. While the outcome of the two sessions was broadly in line with my expectations, the stock failed to move higher, among others, due to escalating tensions in the Middle East.

I am usually wary of stocks that keep going up on announcements and then failing to match the hype with earnings, something Alibaba has done for the last couple of quarters. However, the earnings slump has largely been driven by losses in the quick commerce business and higher AI investments. Both quick commerce and AI are fast-growing businesses, though, and are a priority for Alibaba.

Alibaba expects its instant commerce gross merchandise value (GMV) to rise to 1 trillion yuan (around $145 billion) by fiscal year 2028, which would end in March 2028. The company expects the business to generate positive free cash flow when that target is met, while projecting full-year profitability in fiscal year 2029.

In AI, Alibaba has full-stack operations and offers models, cloud services, and chips. During the earnings call, Alibaba said that as of February 2026, T-head, which is its chip unit, has shipped 470,000 chips cumulatively. The management, however, said that it does not have immediate listing plans for that business, as some reports had suggested, even as it said it “won't rule out” an IPO in the future.

The management expects the combined cloud and AI revenues over the next five years to reach $100 billion. AI, particularly chips, is a high-focus area for the Chinese government as it pushes for domestic production of AI chips and reduces reliance on imports from U.S. giants like Nvidia (NVDA).

Since Alibaba’s earnings have been subdued in recent quarters, its valuation multiples have appeared elevated. Analysts expect the company’s earnings per share to rise 53% YoY to $7.79 in the next fiscal year, which gives us a fiscal year 2027 price-to-earnings (P/E) multiple of just over 16x. Alibaba’s earnings should increase meaningfully in the coming years as the unit economics in the instant commerce business improve, and its AI investments start paying off.

There are also value-unlocking opportunities as the company plans to list its different business units, including one that houses its cloud and AI business. A possible listing of Ant Financial would also help unlock value, even as that IPO, which was stalled by Chinese authorities in 2020, might take some more time. While there are genuine concerns over the slowdown in China and the Iran war is putting pressure on risk assets, I remain constructive on BABA shares and see it delivering strong returns over the next couple of years.

On the date of publication, Mohit Oberoi had a position in: BABA, NVDA. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)