/AI%20(artificial%20intelligence)/AI%20Infrastructure%20by%20FOTOGRIN%20via%20Shutterstock.jpg)

The race to build AI infrastructure is happening on an extraordinary scale right now. In 2026, the four largest tech companies alone are projected to spend a combined $650 billion or more on data centers and AI infrastructure, a huge jump in capital spending across the AI ecosystem.

At the same time, the market for managing those data centers is expected to grow from about $3.02 billion in 2024 to roughly $5.01 billion in 2029, reflecting a compound annual growth rate (CAGR) of 10.6%. Put together, these points urgently demand specialized hardware to hold it all together.

Celestica now sits squarely in that conversation, as the company has aligned itself tightly with the AI buildout by partnering with Advanced Micro Devices (AMD) on a new rack-scale platform. With that kind of momentum in both fundamentals and partnerships, the real question is whether this lesser-known AI infrastructure name still offers attractive upside from here. Let’s take a closer look.

Celestica’s Financial Numbers

Based in Toronto, Canada, Celestica (CLS) carries a market capitalization of around $31.4 billion and provides design, manufacturing, and supply-chain solutions for advanced technology and AI infrastructure. CLS stock trades near the $277 level as of this writing, with a year-to-date (YTD) decline of 6.5% and a 52‑week gain of 200%.

CLS stock carries a trailing price-to-earnings (P/E) ratio of 51.2 times and a price-to-sales (P/S) multiple of 2.6 rimes, compared with sector medians of 22.3 times and 3.2 times, respectively. That suggests that investors are paying a premium for earnings growth while still receiving a relative discount on sales.

Celestica’s most recent quarterly scorecard, released for the period ending December 2025, showed the sort of execution that helps explain this premium. Fourth‑quarter 2025 revenue came in at $3.65 billion, up 44% year-over-year (YOY) from about $2.55 billion in the same quarter of 2024.

The report also featured an earnings surprise, with Q4 adjusted EPS of $1.80 versus Wall Street expectations of $1.61, a positive surprise of 11.8% highlighting consistent outperformance. The company generated net income of $267.5 million for December 2025, representing a modest 0.11% YOY decline.

That operating backdrop supported full-year 2025 revenue of $12.39 billion, up 28% YOY, alongside GAAP EPS of $7.16 versus $3.61 for 2024. Over the same period, adjusted EPS rose from $3.88 in 2024 to $6.05, effectively doubling reported earnings in just one year. This earnings strength was complemented by shareholder returns, as the firm repurchased 100,000 shares for $35.7 million.

Growth Catalysts Behind Celestica’s AI Push

Celestica’s new Helios partnership with AMD is the clearest sign of its deepening role in AI infrastructure. This collaboration, announced on March 16, makes Celestica responsible for the R&D, design, and manufacturing of scale‑up networking switches inside the Helios rack‑scale AI platform, built on the Open Compute Project’s Open‑Rack‑Wide form factor. The hardware will use advanced networking silicon to interconnect next‑generation AMD Instinct MI450 GPUs with Ultra Accelerator Link over Ethernet, with systems slated to reach cloud, enterprise, and research customers in late 2026.

The growth story here is not just about one platform. Celestica has also outlined plans to invest about $1 billion in capital expenditures in 2026 to expand capacity for AI‑driven programs, with new capacity expected to come online through 2026 and 2027, funded from operating cash flow.

Extending beyond compute and networking into storage, Celestica has also rolled out its SD6300 platform targeting maximum storage density for enterprise and AI applications, further rounding out its rack‑scale offering for data‑intensive workloads.

What Does Wall Street See in Celestica Now?

Analysts are not exactly shy about where they stand on Celestica right now, and the numbers around the next print help explain why. The next earnings release is scheduled for April 23. For the March 2026 quarter, the average EPS estimate is $1.96, implying an impressive YOY growth rate of about 96% from $1.00 a year ago.

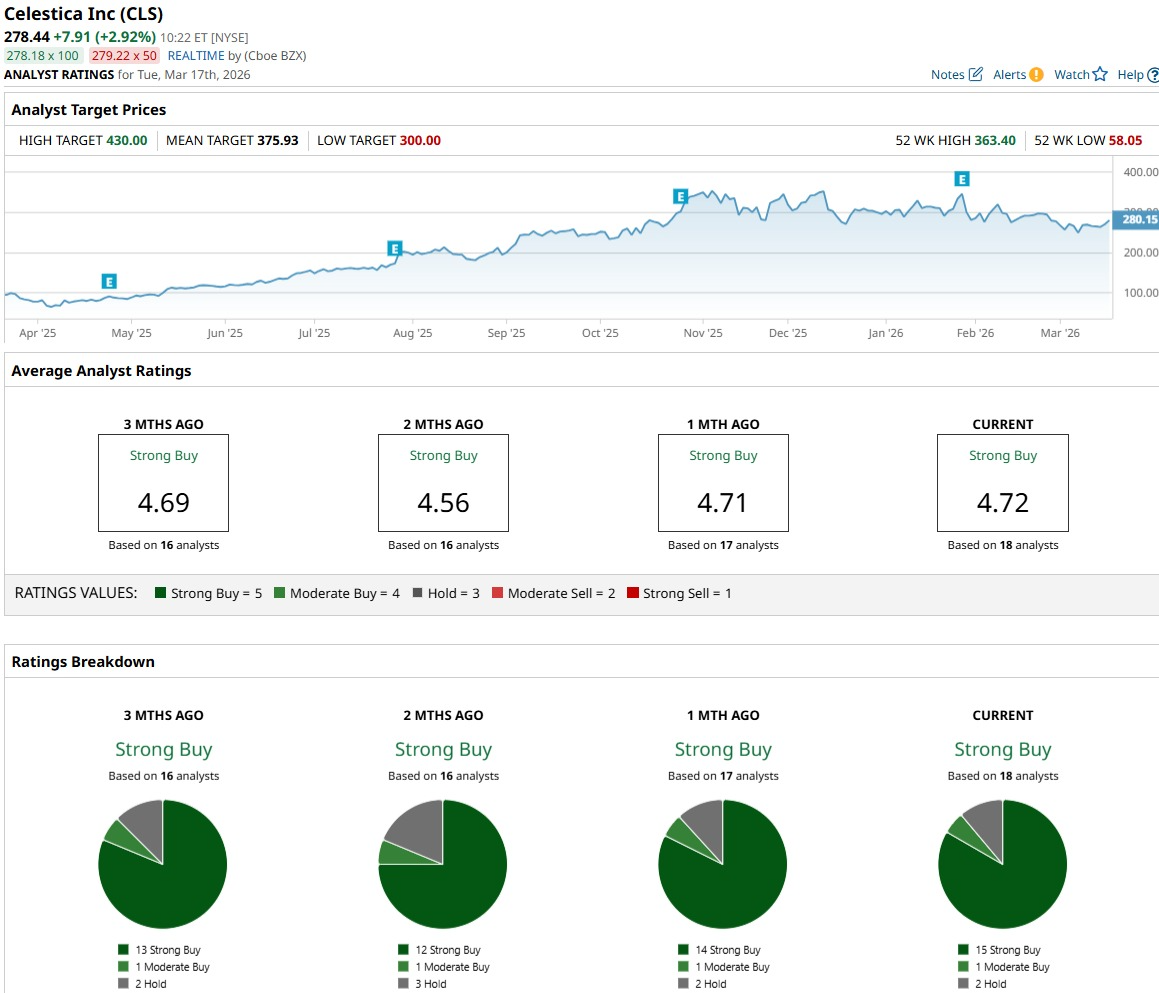

On the individual side, CLSA analyst Skye Chen offers a “Buy” rating and a $350 price target for CLS stock, implying potential upside of 26%.

That bullish view aligns neatly with how CLS stock is rated by 18 covering analysts, with shares earning a consensus “Strong Buy" rating. The broader price‑target picture is even more upbeat, with the average target of $375.93 implying roughly 36% potential upside if the consensus proves right. The Street is effectively betting that Celestica’s execution on AI‑linked infrastructure, including its rack‑scale collaboration with AMD, can keep pushing both earnings and CLS shares higher over the coming year.

Conclusion

Celestica looks like a reasonable buy for investors seeking targeted exposure to AI infrastructure and who can handle some bumps along the way. The fundamentals are moving in the right direction, and the AMD rack-scale partnership gives the story extra torque if execution remains solid. Wall Street’s “Strong Buy” stance and healthy upside targets suggest the path of least resistance is still higher over the next year, even if the pace cools from CLS stock's recent run. Over time, the odds favor this stock grinding upward rather than meaningfully retracing.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)