/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

Semiconductor behemoth NVIDIA Corporation (NVDA) is currently navigating a market that is influenced by both innovation and geopolitics. The escalating U.S.-Iran war has introduced a fresh layer of uncertainty, and the potential disruption in the Strait of Hormuz sits at the heart of the concern.

The narrow passage handles nearly 20% of global oil and gas flows, but the ripple effects stretch far beyond energy. Helium, a critical input in semiconductor manufacturing, moves through the same channels, and any prolonged disruption threatens to tighten supply across the chip ecosystem.

Additionally, bromine and other essential industrial chemicals sourced from the Middle East play a quiet yet indispensable role in chip fabrication. When these inputs face constraints, costs rise, production timelines stretch, and margins come under scrutiny. For Nvidia, whose growth engine depends on the rapid deployment of artificial intelligence (AI) infrastructure, even small disruptions can carry outsized consequences.

Markets have already begun to price in this risk. Semiconductor and AI-linked equities have drifted lower as oil prices climb. J.P. Morgan’s former chief strategist and co-head of Global Research, Marko Kolanovic, warns that semiconductor ETFs could face a sharp 30% correction.

Against this backdrop, Nvidia’s resilience will hinge on how well it balances structural demand with near-term supply shocks.

About Nvidia Stock

Headquartered in Santa Clara, California, NVIDIA is at the center of the global AI transformation. The company designs advanced GPUs and computing platforms that power gaming, data centers, and autonomous technologies. Its ecosystem extends well beyond hardware, with software frameworks that anchor developers and enterprises into its architecture.

With a market cap of approximately $4.4 trillion, Nvidia has built a commanding presence in high-performance computing and machine learning.

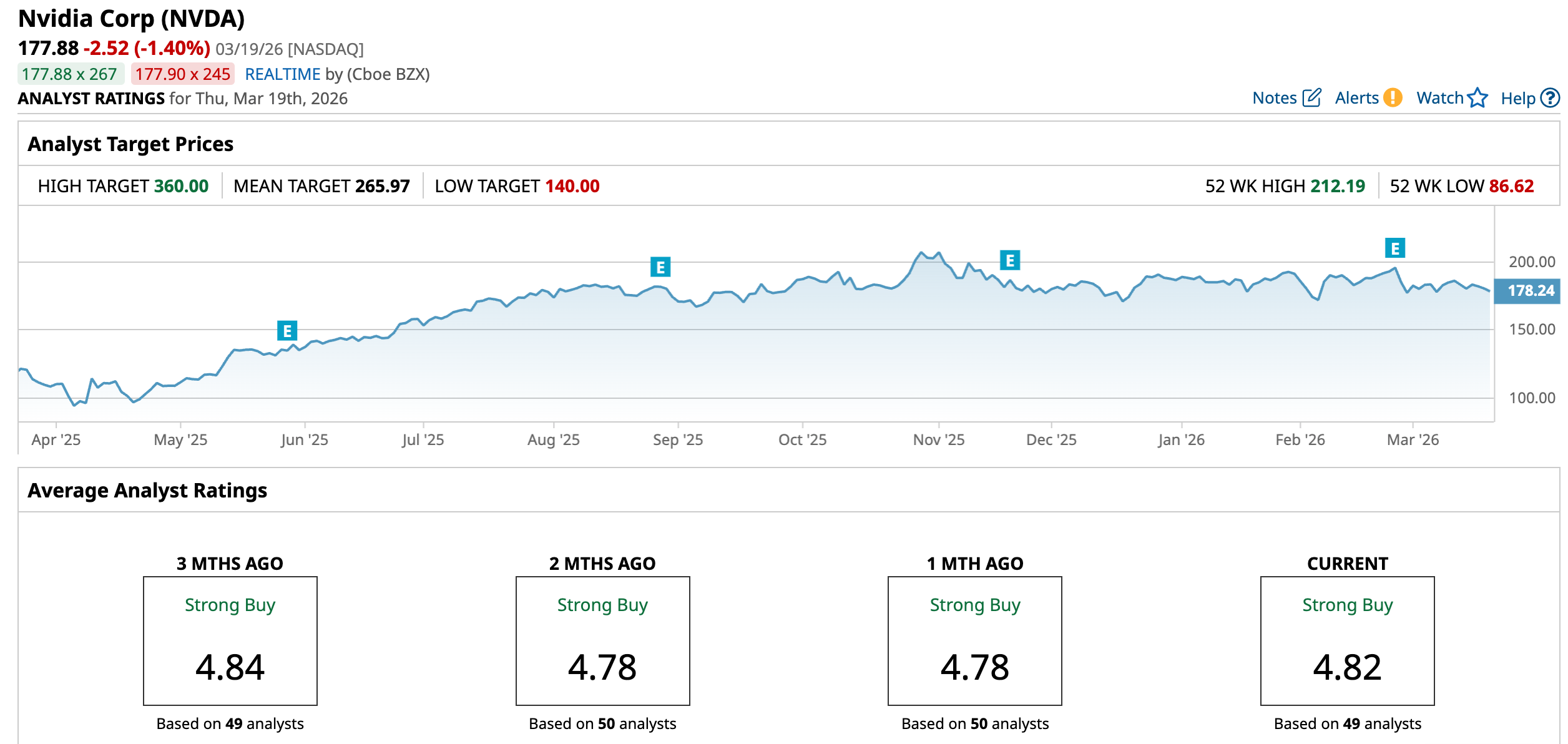

The stock’s recent trajectory reflects both strength and caution. Year-to-date (YTD), shares are down 4.24%, signaling some cooling amid macro pressures. Yet the broader trend remains intact, with gains of 1.09% over the past six months and a 51.97% surge over the last 52 weeks.

Coming to valuation, the stock trades at 24.19 times forward adjusted earnings and 11.88 times sales. The multiples sit above industry averages, yet they come in below Nvidia’s own five-year historical norms.

Also, Nvidia pays a modest dividend of $0.04 per share annually, translating to a yield of 0.02%. The next quarterly payment of $0.01 per share is scheduled for April 1 to shareholders of record as of March 11.

Nvidia Surpasses Q4 Earnings

On Feb. 25, the chipmaker reported fourth-quarter fiscal 2026 results that topped analyst expectations on both top and bottom lines. Total revenue grew 73.2% year-over-year (YOY) to $68.13 billion, surpassing the Street’s forecast of $65.42 billion. Adjusted EPS followed the same trajectory, climbing 82% YOY to $1.62 and beating estimates of $1.52.

The data center segment continues to carry the torch. Its revenue surged to $62.3 billion, rising nearly 75% YOY as hyperscale cloud providers and enterprises accelerated investments in AI infrastructure.

Other segments added meaningful depth. Gaming revenue came in at $3.7 billion, up roughly 47% from a year ago, supported by strong adoption of the Blackwell architecture across high-performance systems.

Professional Visualization stood out with revenue of $1.3 billion, marking a striking 159% increase, again driven by Blackwell demand. Automotive revenue reached $604 million, growing 6% YOY as adoption of Nvidia’s self-driving platforms continued to expand.

Moreover, non-GAAP gross margin held firm at 75.2%, underscoring pricing power and operating leverage. Management highlighted that enterprise adoption of AI agents is accelerating rapidly, with customers investing aggressively in AI compute infrastructure that underpins future growth.

Looking ahead, Nvidia expects Q1 fiscal 2027 revenue of $78 billion, plus or minus 2%, with growth led primarily by the data center business. Non-GAAP gross margin is projected at 75%, plus or minus 50 basis points, while full-year margins are expected to remain in the mid-70s.

Analysts continue to track the momentum closely. They project Q1 fiscal 2027 EPS to rise 116.9% YOY to $1.67. For the full fiscal year 2027, the bottom line is expected to increase 65% to $7.54, followed by a further 26% rise to $9.50 in fiscal year 2028.

What Do Analysts Expect for Nvidia Stock?

Analyst sentiment around Nvidia remains firmly constructive, even as near-term risks linger beneath the surface. Truist Securities analyst William Stein has reiterated a “Buy” rating while lifting the price target to $287 from $283.

Raymond James analyst Srini Pajjuri has taken an even more optimistic stance, maintaining a “Strong Buy” rating and raising the target to $323 from $291. Furthermore, Rosenblatt’s Kevin Cassidy has followed suit, keeping a “Buy” rating and increasing his price target to $325 from $300.

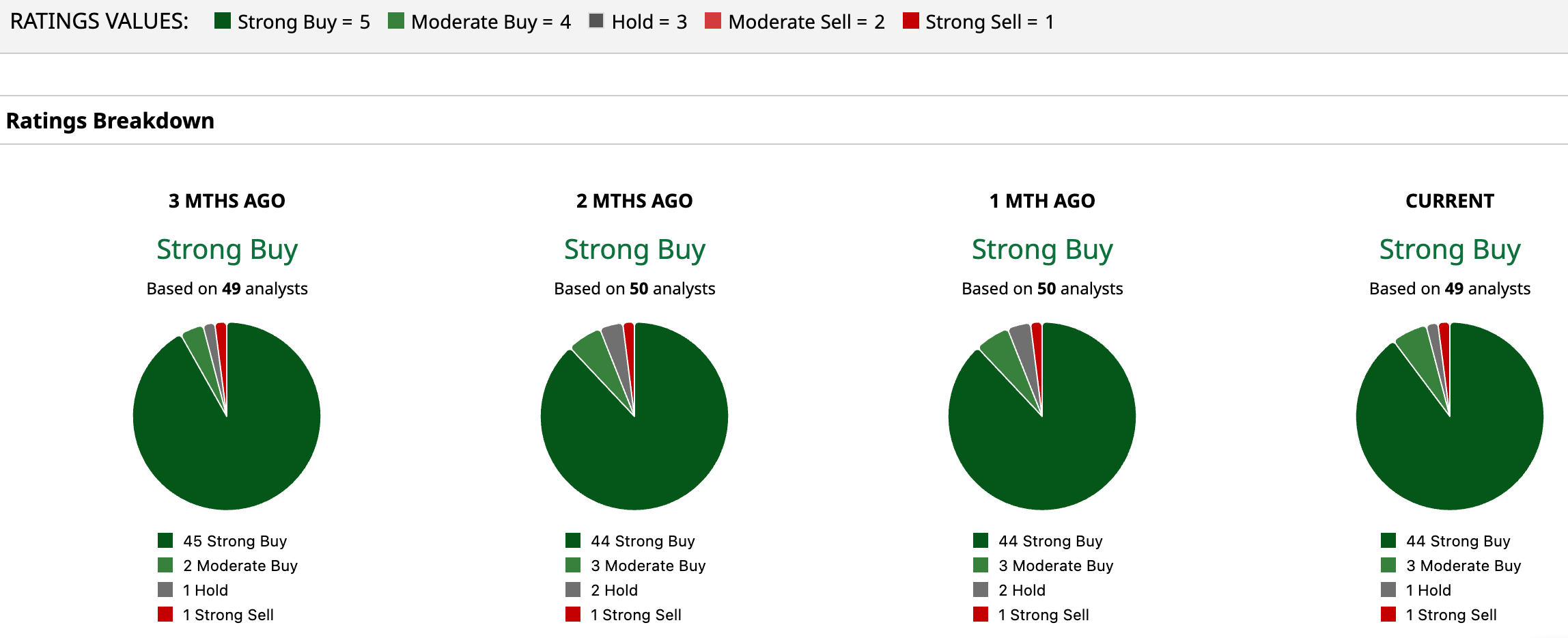

Broadly speaking, analyst sentiment remains overwhelmingly positive with an overall rating of “Strong Buy.” Among the 49 analysts currently covering the stock, 44 assign a “Strong Buy” rating, three maintain a “Moderate Buy,” one recommends “Hold,” and one analyst has issued a “Strong Sell.”

Based on current projections, the average price target of $265.97 implies potential upside of 49.5%. Meanwhile, the Street-high target of $360 set by Tigress Financial analyst Ivan Feinseth suggests an even stronger rally of 102.4% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Eli%20Lilly%20%26%20Co_%20by%20Tada%20Images%20via%20Shutterstock.jpg)