/Boston%20Scientific%20Corp_%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

Global markets have entered a period of recalibration as the war between the U.S. and Iran ripples through one of the world’s most critical energy arteries. The disruption of oil and gas shipments through the Strait of Hormuz has tightened supply expectations and stirred fresh volatility across energy markets.

Investors, as they often do in uncertain times, have turned to history for guidance. In the aftermath of major oil supply shocks, select sectors tend to rise above the noise. Energy, consumer staples, healthcare, and utilities have consistently delivered returns exceeding 5% in the 12 months following such disruptions.

These sectors draw strength from necessity. When energy costs climb and economic momentum softens, demand for essential goods and services rarely wavers. The resilience often translates into steadier earnings and, in turn, stronger stock performance.

Within this framework, healthcare stands out as a quiet stabilizer. Against this backdrop, Boston Scientific Corporation (BSX) has emerged as one of the highest-rated names to watch, offering a potential hedge as markets navigate the crosscurrents of rising energy risk and economic uncertainty.

About Boston Scientific Stock

Based in Marlborough, Massachusetts, Boston Scientific designs and delivers medical devices across a wide spectrum of interventional specialties. The company addresses gastrointestinal, urological, neurological, cardiac, and vascular conditions through diagnostic tools, implants, and minimally invasive systems.

Holding a market cap of approximately $105.7 billion, it also extends its reach into cancer care and remote patient monitoring, reinforcing its role in critical healthcare delivery. BSX firmly sits in large-cap territory.

The stock has not escaped broader market pressure. Over the past 52 weeks, BSX stock has declined 28.19%, with a 27.47% drop over the last six months. Yet, recent momentum hints at a shift in tone, with the stock gaining 2.32% in the past five trading sessions.

From a valuation standpoint, BSX stock is trading at 20.20 times forward adjusted earnings and 4.74 times sales. The multiples exceed industry averages, yet they sit below the company’s own five-year average multiples, suggesting a favorable entry point for long-term investors.

Boston Scientific Surpasses Q4 Earnings

On Feb. 4, Boston Scientific unveiled its Q4 fiscal 2025 earnings results, which met Street’s expectations. During the quarter, revenue rose 15.9% year-over-year (YOY) to $5.29 billion, narrowly edging past expectations of $5.27 billion. Adjusted EPS grew 14.3% from the year-ago value to $0.80, surpassing the Street’s estimates of $0.78

Profitability advanced in tandem with revenue. Adjusted operating income grew 15.4% to $1.4 billion, while adjusted net income advanced 15.1% to $1.2 billion. These increases were supported by broad-based strength across electrophysiology (EP), WATCHMAN (a left atrial appendage closure device used to reduce stroke risk in patients with atrial fibrillation), interventional oncology, and neuromodulation.

Nevertheless, some cracks appeared. U.S. EP sales showed sequential stagnation, and WATCHMAN modestly underperformed expectations, both critical growth drivers. CEO Michael Mahoney noted anticipated share pressure in EP amid new competition but reaffirmed confidence in sustaining above-market growth.

Looking ahead, management maintains a cautiously optimistic outlook. Management’s forward guidance carries a similar tone of measured confidence. For full-year 2026, the company expects net sales growth of 10.5% to 11.5% on a reported basis and 10% to 11% organically. Adjusted EPS is projected between $3.43 and $3.49.

Meanwhile, for the Q1 fiscal year 2026, sales are expected to grow 10.5% to 12.0%, with EPS in the range of $0.78 to $0.80. Analysts, on the other hand, expect Q1 fiscal 2026 EPS to rise 6.7% YOY to $0.80. For full-year 2026, projections point to 12.8% growth to $3.45, followed by another 13.3% increase to $3.91 in fiscal year 2027.

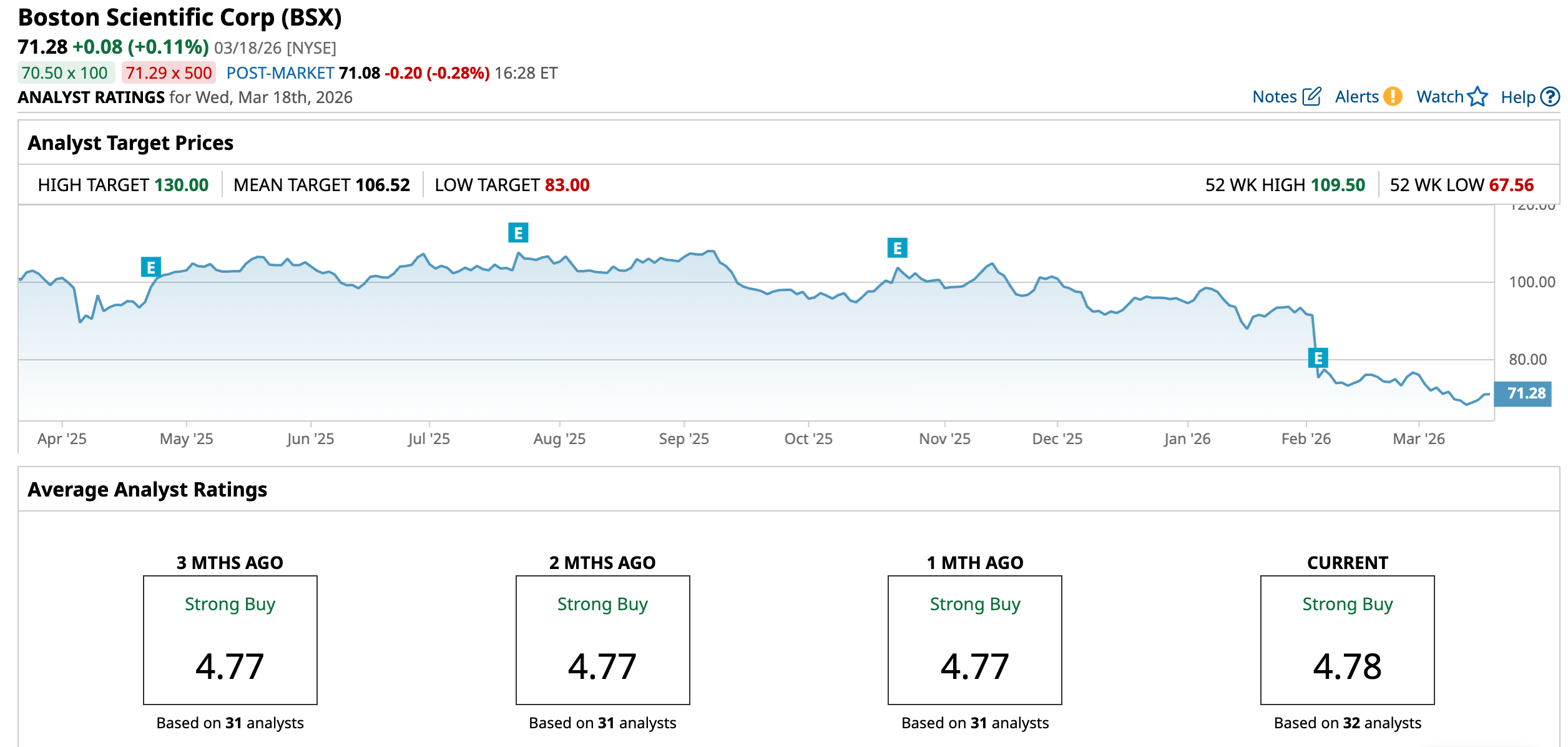

What Do Analysts Expect for Boston Scientific Stock?

Analysts have trimmed price targets, yet they have not abandoned conviction. UBS analyst Danielle Antalffy maintained a “Buy” rating while trimming the price target from $120 to $105. Similarly, William Plovanic at Canaccord Genuity reiterated a “Buy” rating, lowering the target slightly from $112 to $109.

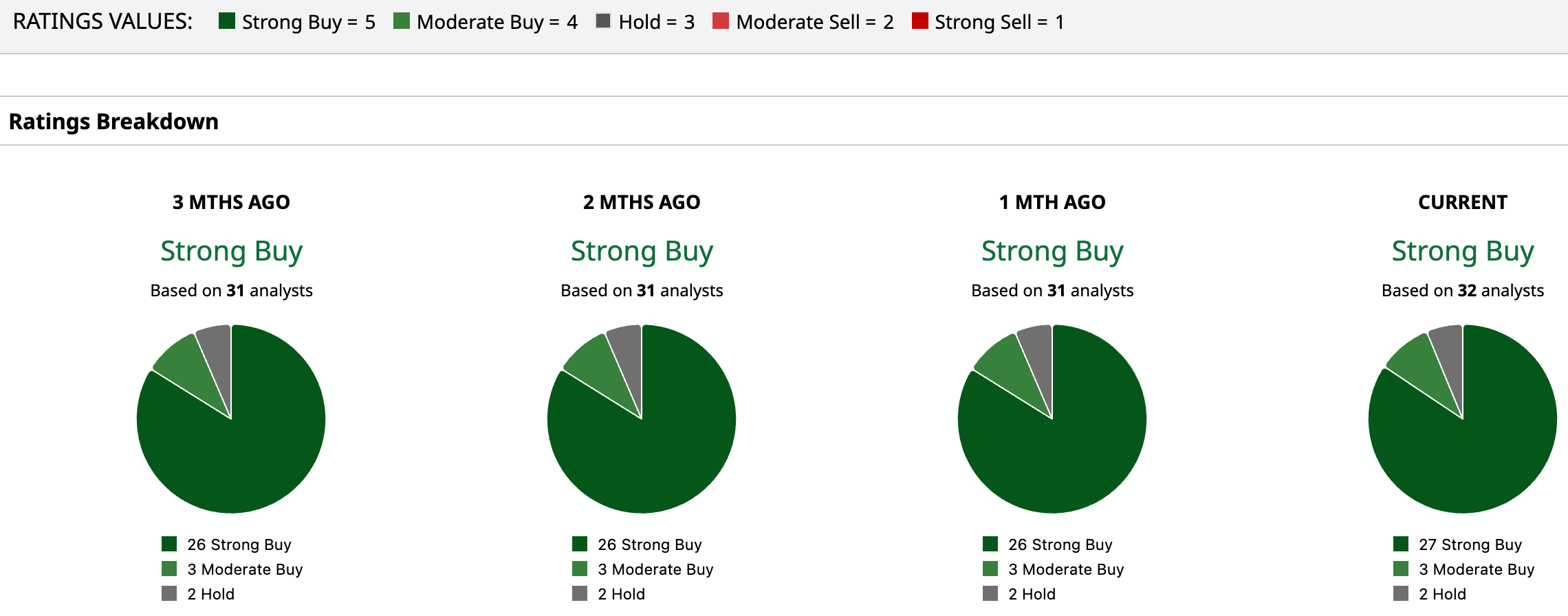

Wall Street’s consensus continues to lean decisively positive with an overall “Strong Buy” rating. Among 32 analysts, 27 rate the stock a “Strong Buy,” three assign a “Moderate Buy,” and only two suggest “Hold.”

To that end, the average price target of $106.52 implies potential upside of 49.4%. Meanwhile, the Street-high target of $130 points to a gain of 82.4% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Broadcom%20Inc%20HQ%20photo-by%20Sundry%20Photogrpahy%20via%20iStock.jpg)