/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)

Memory-chip names have been the market’s standout performers as artificial intelligence (AI)-driven demand tightens supply and lifts contract pricing. Investors hunting for growth in semiconductors are watching capacity, pricing trends, and upcoming earnings closely.

Without any doubt, Micron Technology (MU) is on top of that list. The semiconductor giant continues to hit new highs, while the broader market is down due to the ongoing Iran war. Nevertheless, a fresh catalyst for Micron just came in as Wedbush Securities sharply raised its price target to $500 from $320, citing pricing that has come in well ahead of expectations.

Wedbush’s Matt Bryson points to stronger-than-expected contract pricing for DRAM and NAND, in some cases rising into triple-digits since late 2025, and tighter supply dynamics that appear to be lifting Micron’s near-term earnings outlook.

With Micron set to report on March 18, the Wedbush call frames a simple investor question: Are you buying into a memory rebound that may still have legs, or paying up for a rally that’s already priced in much of the upside?

DRAM Price Surge Lifts Micron’s Momentum

DRAM, the memory used in AI servers and data centers, is in a strong upcycle right now. Prices have jumped about 30% to 50%, and in some cases even more, as demand rises and supply stays tight. This is directly helping Micron by boosting its margins and making its earnings outlook stronger.

At the same time, Micron is moving fast. It is shipping next-gen HBM4 memory for AI chips, expanding its NAND and SSD lineup, and building more capacity around the world. With much of its HBM supply already locked in through long-term deals, Micron is in a good position to benefit from strong pricing, which is why analysts are turning more bullish on the stock.

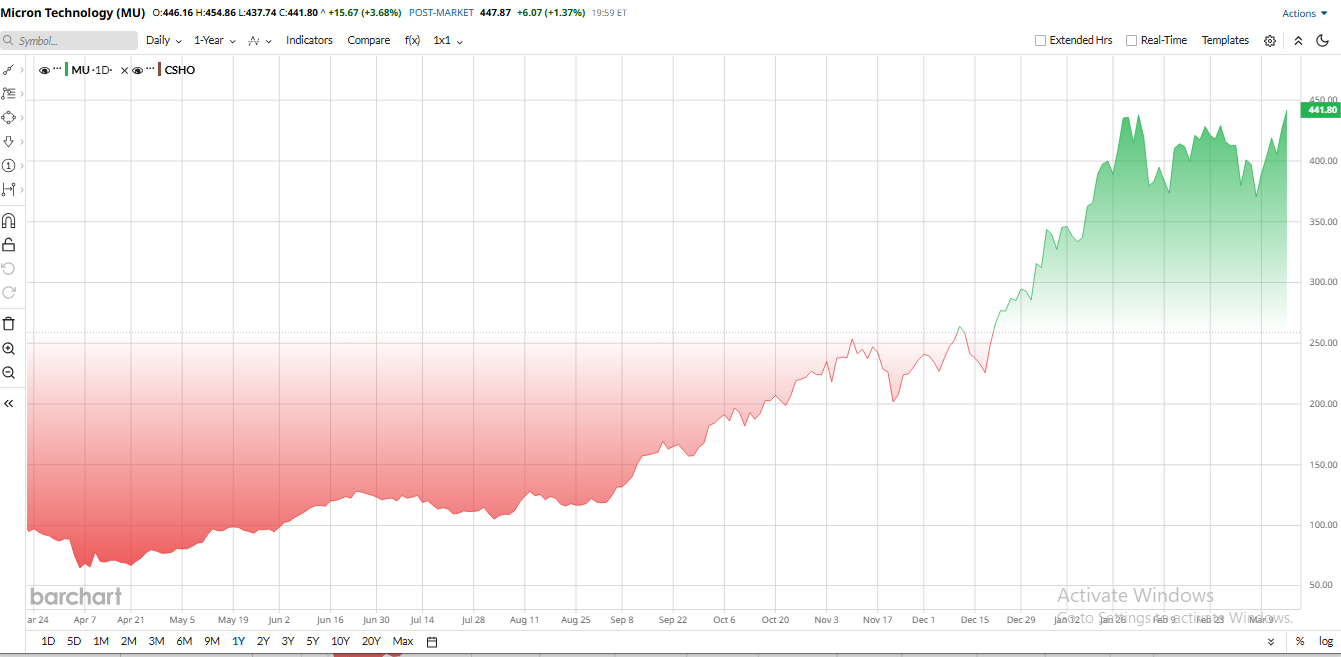

Micron’s stock has ripped higher in recent times. It's up roughly 340% over the past year and about 55% so far in 2026. Much of the gain tells the story of the AI-related memory boom and Micron’s record financial results, which propelled its stock to record highs.

But the question remains, with the run-up, is MU now expensive? Here is the surprising thing: on many metrics, it still looks reasonable. For example, Micron’s forward price-to-earnings (P/E) ratio is only about 11.5x, well below the semiconductor sector median of 21x. Its forward price-to-cash-flow of 9.5x is roughly half the peer norm. Although its price-to-sales (P/S) is higher, at 5.8x vs. a 3.05x median, Micron’s revenue is projected to grow 60% next year, which is far above that of its peers. In short, MU’s valuation is not crazy rich given its torrid growth outlook and healthy margins.

Why Analysts Are Bullish on Micron Stock?

On March 13, Wedbush Research hiked its MU target to $500 and kept an “Outperform” rating. Wedbush said it calculated $500 by applying 5x its forecast of FY2027 earnings per share (EPS) plus net cash. In other words, it’s pricing in very strong future profits, yet still “below typical peak” memory multiples.

Wedbush isn’t alone bullish on Micron; other analysts have also lifted targets. For example, Morgan Stanley recently raised its MU target to $450, and Deutsche Bank lifted its target to $500. Wolfe, RBC, TD Cowen, and others have targets in the range of $500 to $550. These shops cite sky-high DRAM and NAND prices. As Micron itself notes, HBM4 (high-bandwidth memory shipments are ramping, and new products like 256GB LPDDR5X server modules are coming. If memory pricing stays on its torrid pace, companies like Wedbush expect MU to keep outperforming.

Analysts’ comments underline why they’re optimistic. For example, Morgan Stanley notes that DDR5 spot prices are 130% above January contract levels and expects DRAM shortages to persist into 2026. UBS highlights “strengthening pricing dynamics” in both DRAM and NAND. Citi’s Atif Malik says AI-driven demand and constrained fab capacity “could push Micron’s stock to new heights”.

What To Expect From the Upcoming Report

Investors’ eyes now turn to Micron’s Q2 report on March 18, with expectations running high. For context, Micron’s Q1 results in November 2025 were record-breaking, with revenue of $13.64 billion, up 56.7% year-over-year, and EPS of $4.78, well ahead of estimates.

Management guided Q2 revenue to around $18.7 billion, with a possible variation of about $0.40 billion, and EPS near $8.42. Analysts currently expect roughly $19.1 billion in revenue and about $8.64 in EPS, reflecting continued strength from AI-driven demand. Prediction markets suggest a high likelihood that Micron could exceed these estimates.

Micron has beaten the consensus in each of its last several quarters. The pattern has been two-sided. Lower near-term shipments by customers have tightened the supply, lifting spot prices 30% year-to-date, which in turn drove Micron’s last quarterly revenue up 45% over the prior 12 months. If the trend continues, we could see another blowout quarter. But any sign of demand slowing could trigger a big reversal given how far MU has run.

Is Micron Stock a Buy Now?

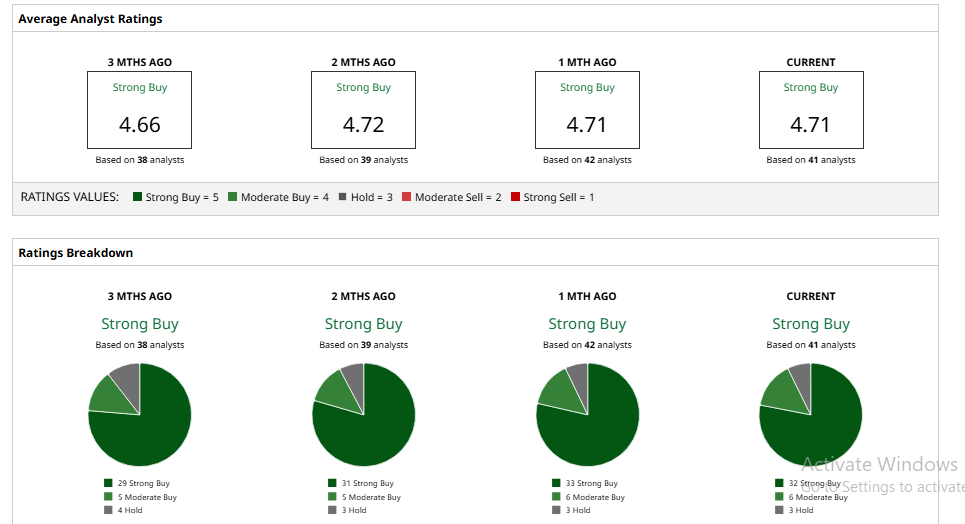

Wall Street’s consensus on Micron is overwhelmingly bullish, as Barchart still shows an average “Strong Buy” stance. Targets are all over the map. But the thing is, Micron stock has now reached well above the mean price target of $377. However, if we look at the street-high target of $550, it still offers more than 25% upside.

The bottom line is that Micron is arguably the “place to be” in memory right now, thanks to AI demand and pricing power. But whether MU is a “buy now” depends on your risk appetite. The company’s growth and cash generation are stellar; it’s been beating estimates quarter after quarter. If Micron’s March earnings and the AI boom keep surprising to the upside, the rally could continue. If not, there may be a sharp reset.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)