/NVIDIA%20Corp%20logo%20on%20phone-by%20Evolf%20via%20Shutterstock.jpg)

After a strong rally, Nvidia (NVDA) stock has cooled off and has seen a period of consolidation. However, recent commentary from CEO Jensen Huang suggests that underlying business momentum remains robust.

At the company’s recent GTC (GPU Technology Conference), its big AI-centric conference for developers, Huang emphasized that demand for Nvidia’s GPUs is “off the charts.” As enterprises and governments accelerate their adoption of AI capabilities, the need for high-performance computing continues to expand, strengthening Nvidia’s dominant position within this ecosystem.

Nvidia has significantly raised its projections for its next-generation chip platforms, Blackwell and Rubin. After estimating roughly $500 billion in GPU demand tied to these platforms last year, the company now expects cumulative demand and purchase commitments to exceed $1 trillion through 2027.

With demand remaining strong and growth expected to continue over the coming quarters, Nvidia could deliver strong financials in fiscal 2027 and beyond, which could support upward movement in its stock.

Explosive Demand for Nvidia AI Chips Supports Long-Term Growth Outlook

Nvidia’s growth outlook remains strong, supported by sustained demand for its AI chips, particularly within its data center segment. In fiscal 2026, the company’s data center business generated $194 billion in revenue, representing a 68% year-over-year (YoY) increase. Management anticipates continued momentum and projects sequential revenue growth throughout calendar year 2026. Nvidia has also secured sufficient inventory and supply commitments to meet future demand, with shipment visibility extending into calendar year 2027.

Next-gen products continue to play a key role in Nvidia’s growth. Ongoing strength in Nvidia’s Blackwell and Blackwell Ultra platforms is expected to drive future growth. At the same time, robust demand for Nvidia’s AI infrastructure could continue to support demand for its Hopper-based products, reflecting broad-based adoption across multiple product generations.

Networking has emerged as another key growth driver within the data center segment. In fiscal 2026, Nvidia’s networking business exceeded $31 billion in revenue. Adoption of solutions such as NVLink, Spectrum-X Ethernet, and InfiniBand remains strong, strengthening the company’s position in high-performance computing and AI networking infrastructure.

A significant contributor to Nvidia’s long-term opportunity is the rise of sovereign AI initiatives. In fiscal 2026, revenue from this segment more than tripled YoY, surpassing $30 billion and benefiting from a diverse and expanding customer base. Management expects sovereign AI demand to grow significantly, as governments increasingly invest in domestic AI capabilities.

Looking ahead, Nvidia has projected first-quarter revenue of $78 billion, a substantial increase from $44.1 billion in the same period of the prior year. This growth is expected to be driven primarily by continued strength in the data center segment.

Is NVDA Stock Undervalued? Nvidia’s Valuation Signals Strong Buy Opportunity

Nvidia’s valuation appears attractive amid accelerating demand for AI computing. Strong adoption of its next-generation AI chips is driving significant revenue momentum and is likely to boost its bottom line in the coming years.

Nvidia trades at approximately 23.96 times forward earnings. This multiple is relatively modest when compared with its historical averages. Moreover, its valuation looks compelling relative to its projected earnings growth, which is expected to exceed 64% in fiscal 2027, followed by another year of solid double-digit growth.

Nvidia’s strong growth and compelling valuation suggest that it is undervalued and has upside potential. In addition, projections of cumulative revenue of over $1 trillion from its AI chips through fiscal 2027 suggest that Nvidia’s growth may surpass current analyst expectations. Even under conservative assumptions, these forecasts imply meaningful upside that does not yet appear to be fully reflected in NVDA’s current share price.

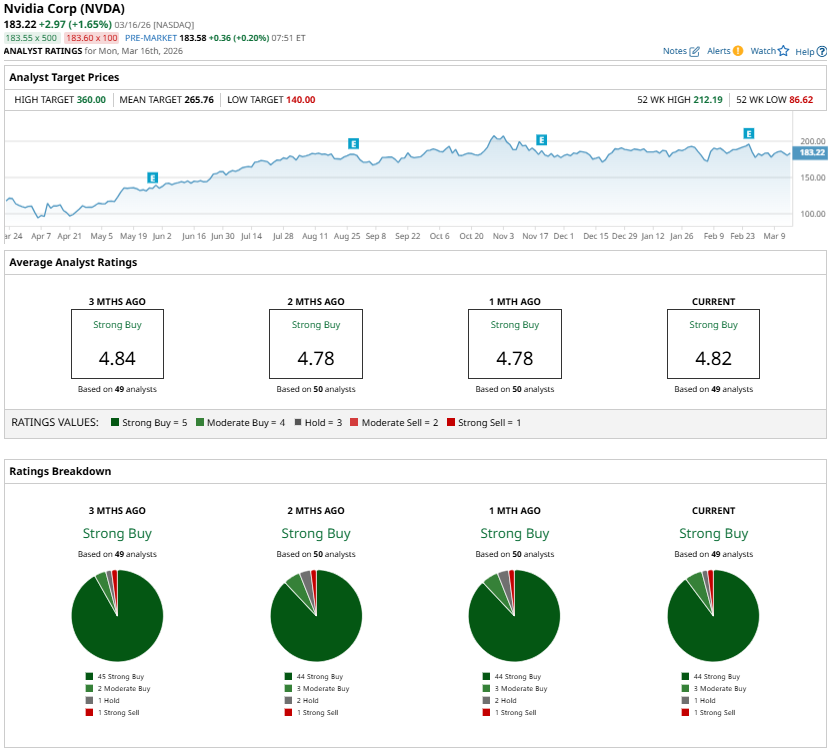

Overall, Nvidia’s leadership in AI computing, expanding market opportunity, and strong visibility into future demand position it as a highly compelling long-term investment. Analysts collectively rate NVDA stock as a “Strong Buy,” and the average price target of $265.76 implies 45% upside from its recent closing price of $183.22.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)