/AI%20(artificial%20intelligence)/AI%20software%20engineering%20by%20Tapati%20Rinchumrus%20via%20Shutterstock.jpg)

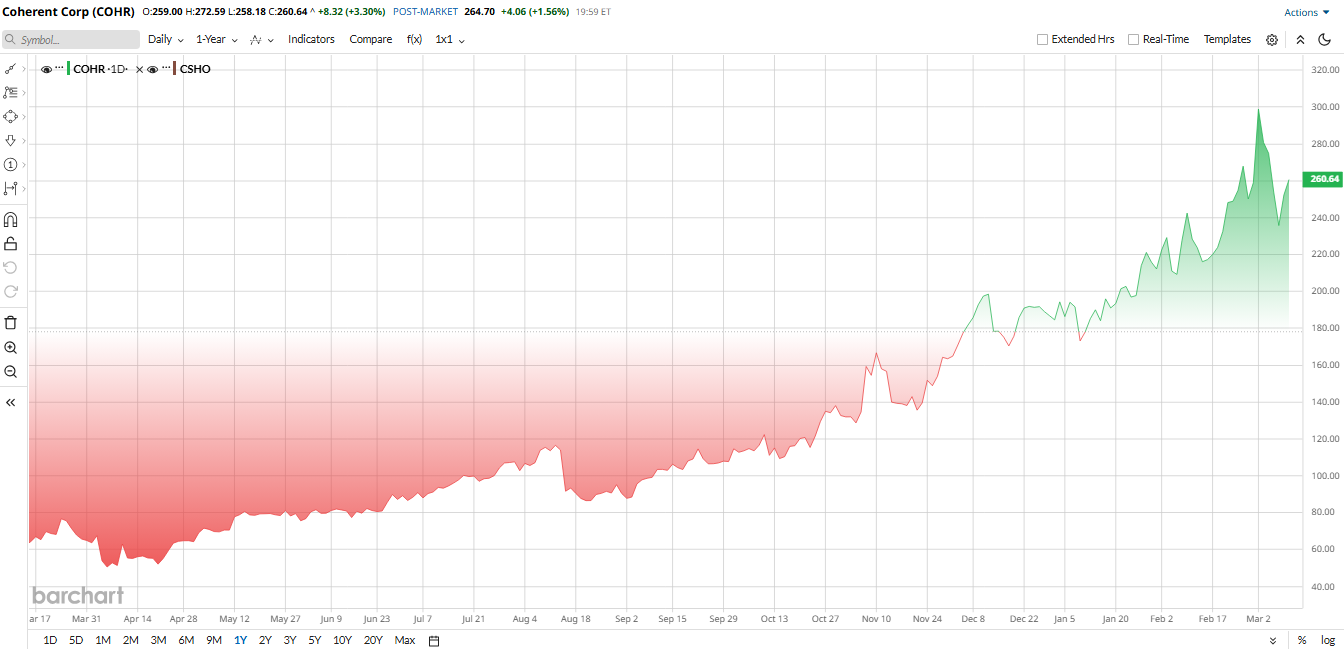

Photonics and optical connectivity stocks have been in the spotlight lately, riding the boom in AI and data-center spending. Companies building next-generation laser and optical switchgear, essential for hyperscale data centers and 5G networks, are seeing robust demand. For example, Nvidia’s (NVDA) recent $2 billion investment in both Lumentum (LUMN) and Coherent (COHR) signaled confidence in these technologies. Those announcements helped shares of Coherent surge, with the stock now up roughly 31% so far in 2026.

Now, Coherent is poised to join the S&P 500 ($SPX) on March 23, raising a key question: Should investors buy COHR stock ahead of the index inclusion? Let's take a closer look.

Rising Demand for AI Data Center Optics

Coherent’s recent momentum is largely tied to rising demand for 800G and 1.6T optical interconnects used in AI data centers. The company is also transitioning to six-inch indium phosphide wafers, which may produce over four times more chips at less than half the cost of three-inch wafers. Management expects about 50% of its internal capacity to shift to the larger wafers by 2026. In the latest quarter, data-center bookings were more than four times the book-to-bill ratio, reflecting strong demand for optical components.

At the same time, Coherent has been expanding its technology portfolio through partnerships and targeted acquisitions aimed at strengthening photonic connectivity and advanced packaging capabilities. These efforts could help the company capture more opportunities tied to AI infrastructure growth.

Still, the semiconductor industry remains cyclical, and demand can fluctuate. Sales in the optics segment can also vary depending on the timing of large data-center hardware deployments. For now, however, booking trends suggest continued demand from AI and cloud infrastructure customers.

Coherent Stock's Performance

Shares of Coherent have been on a tear lately. Over the past 52 weeks, COHR stock is up by more than 258% largely because demand for AI data-center optics has exploded, making the company a key supplier for high-speed networking used by AI clusters. The rally was further boosted by major AI partnerships and investments from companies like Nvidia, which strengthened expectations for long-term growth in optical networking infrastructure.

Despite the rally, Coherent now trades at relatively elevated valuation levels. The company’s price-to-sales (P/S) ratio is now about 8.4 times, compared with roughly 4 times to 5 times for many industrial tech peers. The EV/EBITDA multiple is also high, near 46 times, suggesting investors are pricing in strong long-term growth. As a result, much of the optimism tied to AI infrastructure, data-center optics, and next-generation connectivity appears already reflected in COHR stock’s valuation.

S&P 500 Inclusion: What Does It Mean?

On March 9, Coherent confirmed that it will be added to the S&P 500 effective March 23. The S&P 500 is the go-to benchmark for large-cap U.S. stocks, so inclusion often triggers a wave of purchases by index funds and exchange-traded funds (ETFs). In any case, being added to the index is a concrete boost to Coherent’s profile.

"Joining the S&P 500 is a testament to the strength of our team, the power of our technology portfolio, and the trust our customers have placed in us,” said CEO Jim Anderson. That aligns with the broader narrative that Coherent’s optical interconnects are central to scaling next-generation AI data centers.

At the same time, some market watchers caution that much of the AI “premium” may already be priced in. COHR stock has already climbed dramatically over the past 12 months, so expectations are high. Investors will see whether Coherent can deliver on the big growth baked into its share price.

Coherent Beats Q2 Earnings Estimates

Coherent reported stronger-than-expected results for its fiscal second quarter, helped by continued demand from data center and communications customers. Revenue for the quarter reached $1.69 billion, rising about 17% from a year earlier, or roughly 22% on a pro forma basis excluding its previously spun-off aerospace and defense business.

Net income totaled $248 million, or $1.29 per share, up about 35% year-over-year (YOY). Additionally, gross margin edged higher to 39%. The company also generated solid free cash flow during the quarter and ended the period with about $863.7 million in cash.

Management said the data center and communications segment accounted for much of the growth, as demand for high-speed optical components continued to rise alongside expanding AI and cloud infrastructure investments. “We delivered strong [YOY] revenue growth […] driven by another quarter of strong demand in our datacenter and communications segment. We expect continued strong growth in the second-half of fiscal 2026 and throughout fiscal 2027," said Anderson. CFO Sherri Luther added that ramping capacity will be needed to meet demand.

Looking ahead, Coherent did not guide for the next quarter, but reiterated that strong AI/datacenter spending should keep growth robust. Analysts have raised their projections accordingly. Consensus now foresees fiscal 2026 EPS at roughly $4.64, representing 73% YOY growth.

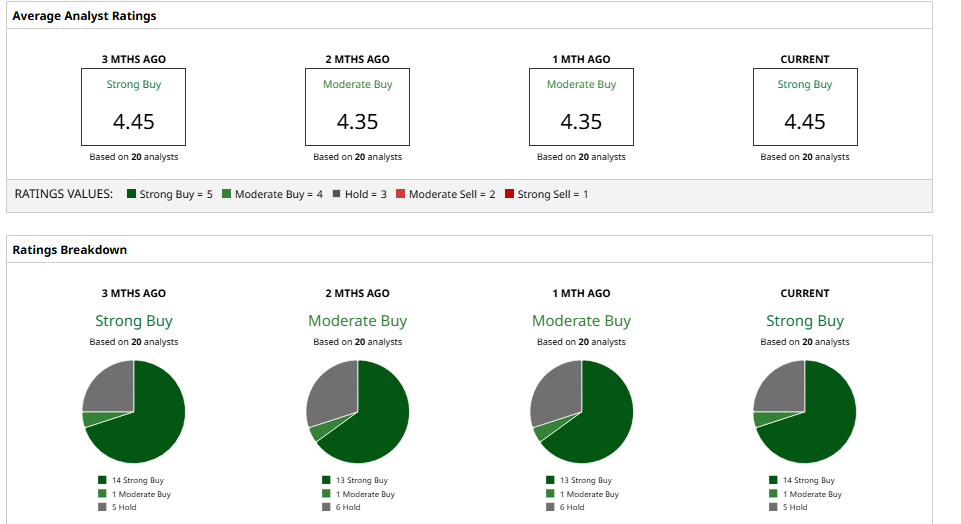

What Do Analysts Think About COHR Stock?

Wall Street is mostly bullish on Coherent. Based on 20 analysts with coverage, COHR stock has a consensus “Strong Buy” rating. However, the mean price target of $265.35 implies very little upside, while the Street-high target of $375 implies a possible 42% increase from current levels.

Following the Q2 report, multiple firms raised their price targets on Coherent. Morgan Stanley analyst Meta Marshall lifted the target to $250, while JPMorgan analyst Samik Chatterjee set a $245 target. Barclays analyst Tom O’Malley also put his target at $235. Finally, Rosenblatt analyst Mike Genovese was more optimistic with a $300 target. Analysts cite Coherent’s leadership in AI optics, record backlog, and now its inclusion in the S&P 500 as reasons for confidence.

In short, many on Wall Street see the current pullback as a buying opportunity for a long-term AI play, while a few analysts warn that the lofty valuation leaves limited room for error.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)