/First%20Solar%20Inc%20name%20on%20building-by%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)

With a market cap of $21.2 billion, First Solar, Inc. (FSLR) is a leading renewable energy company specializing in the design and manufacture of solar photovoltaic (PV) modules and utility-scale solar power solutions. Headquartered in Arizona, the company focuses primarily on large-scale solar projects developed by utilities, independent power producers, and commercial energy providers.

Companies worth $10 billion or more are generally described as "large-cap stocks," and First Solar fits right into that category, with its market cap exceeding this threshold, reflecting its substantial size, influence, and dominance in the solar industry. First Solar is best known for its thin-film solar module technology, which differs from conventional crystalline silicon panels used by most solar manufacturers. It benefits from growing demand for clean energy and energy security, particularly in the United States and Europe. The company has also expanded domestic manufacturing capacity to take advantage of incentives created under the Inflation Reduction Act, which supports U.S.-based solar manufacturing.

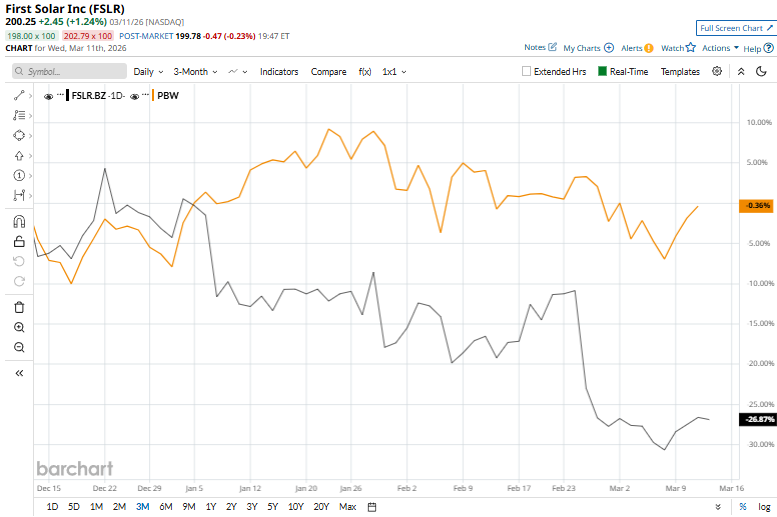

FSLR stock touched its 52-week high of $285.99 on Nov. 5 and is currently trading 30% below that peak. Meanwhile, FSLR stock has plunged 26.6% over the past three months, lagging behind the Invesco WilderHill Clean Energy ETF (PBW), which observed a marginal decline during the same time frame.

FSLR stock has tanked 1.5% over the past six months and soared 44% over the past 52 weeks, compared to PBW’s 30.5% gains on a six-month basis and 97.5% returns over the past year.

FSLR stock has been trading below its 50-day moving average since early January and slipped under the 200-day moving average since the end of February, underscoring its bearish trend.

On Feb. 25, shares of solar panel manufacturer First Solar fell about 15% in morning trading after the company reported mixed fourth-quarter results and issued a weaker-than-expected outlook for the year ahead the day before. It posted a revenue of about $1.68 billion, up roughly 11% year over year due to higher solar module shipments. While the company continued to benefit from strong demand for utility-scale solar projects and maintained a sizeable order backlog, its fourth-quarter earnings per share of $4.84 missed Wall Street estimates, dampening investor sentiment.

The disappointment was compounded by the company’s soft guidance for 2026, with management projecting net sales between $4.9 billion and $5.2 billion, significantly below analysts’ consensus estimate of roughly $6.1 billion. The outlook suggested potential project timing shifts, slower deployment expectations, or cautious customer spending, which weighed on growth expectations for the solar manufacturer. Despite the near-term setback, First Solar continues to expand its U.S. manufacturing capacity and thin-film solar module production, positioning itself to benefit from long-term demand for clean energy and domestic solar supply chains supported by incentives under the Inflation Reduction Act.

Additionally, FSLR stock has notably lagged behind its peer Nextpower Inc.’s (NXT) 72.9% surge over the past six months and 159.7% return over the past 52 weeks.

Among the 33 analysts covering the FSLR stock, the consensus rating is a “Moderate Buy.” As of writing, FSLR’s mean price target of $250.30 suggests a modest 25% upside potential.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Renewable%20Energy%20by%20Yuri%20Hoya%20via%20Shutterstock.jpg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)