Over the past six months, Icahn Enterprises’s stock price fell to $7.54. Shareholders have lost 9.8% of their capital, which is disappointing considering the S&P 500 has climbed by 3.1%. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Icahn Enterprises, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Icahn Enterprises Not Exciting?

Even though the stock has become cheaper, we're swiping left on Icahn Enterprises for now. Here are three reasons why IEP doesn't excite us and a stock we'd rather own.

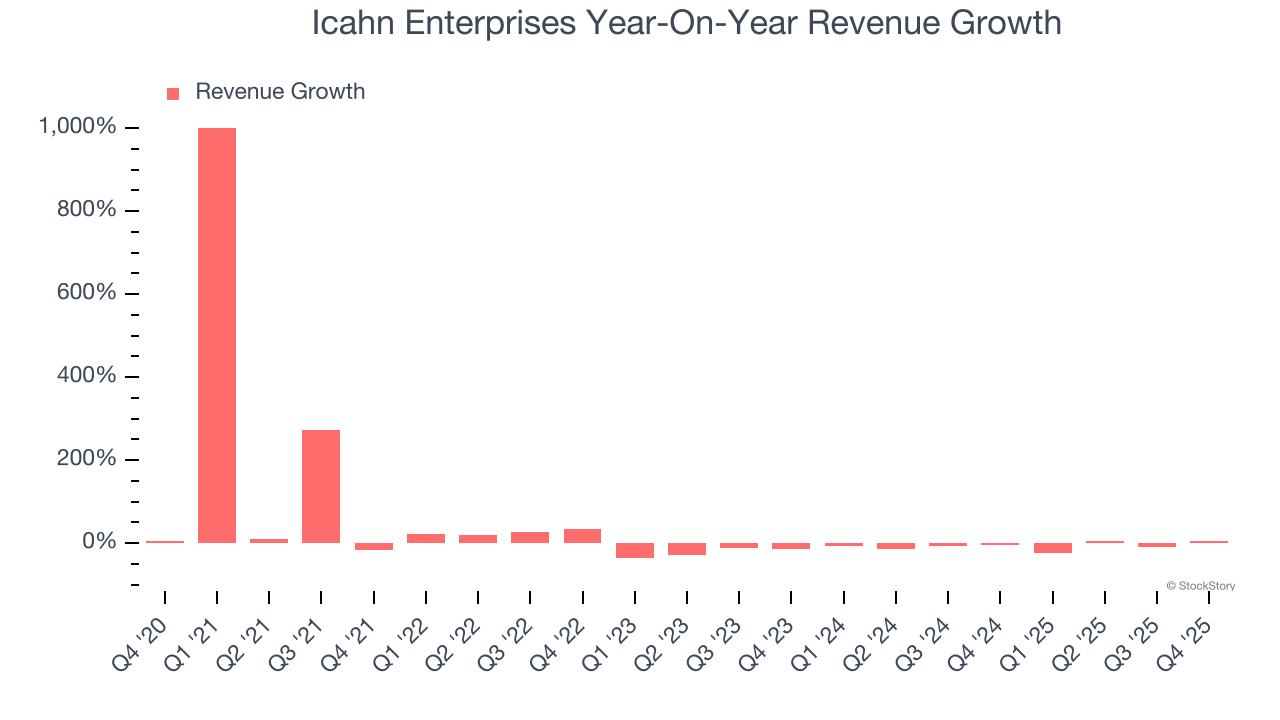

1. Revenue Tumbling Downwards

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Icahn Enterprises’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 7.1% over the last two years.

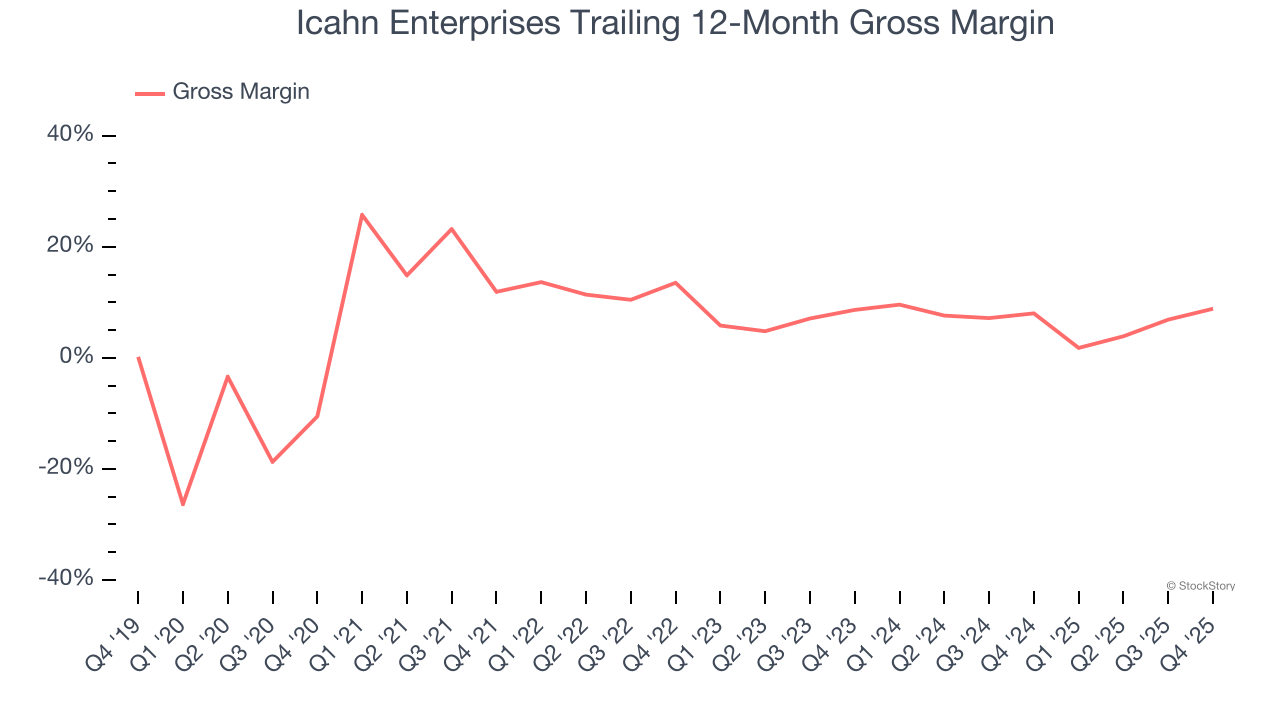

2. Low Gross Margin Reveals Weak Structural Profitability

At StockStory, we prefer high gross margin businesses because they indicate the company has pricing power or differentiated products, giving it a chance to generate higher operating profits.

Icahn Enterprises has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 10.5% gross margin over the last five years. Said differently, Icahn Enterprises had to pay a chunky $89.54 to its suppliers for every $100 in revenue.

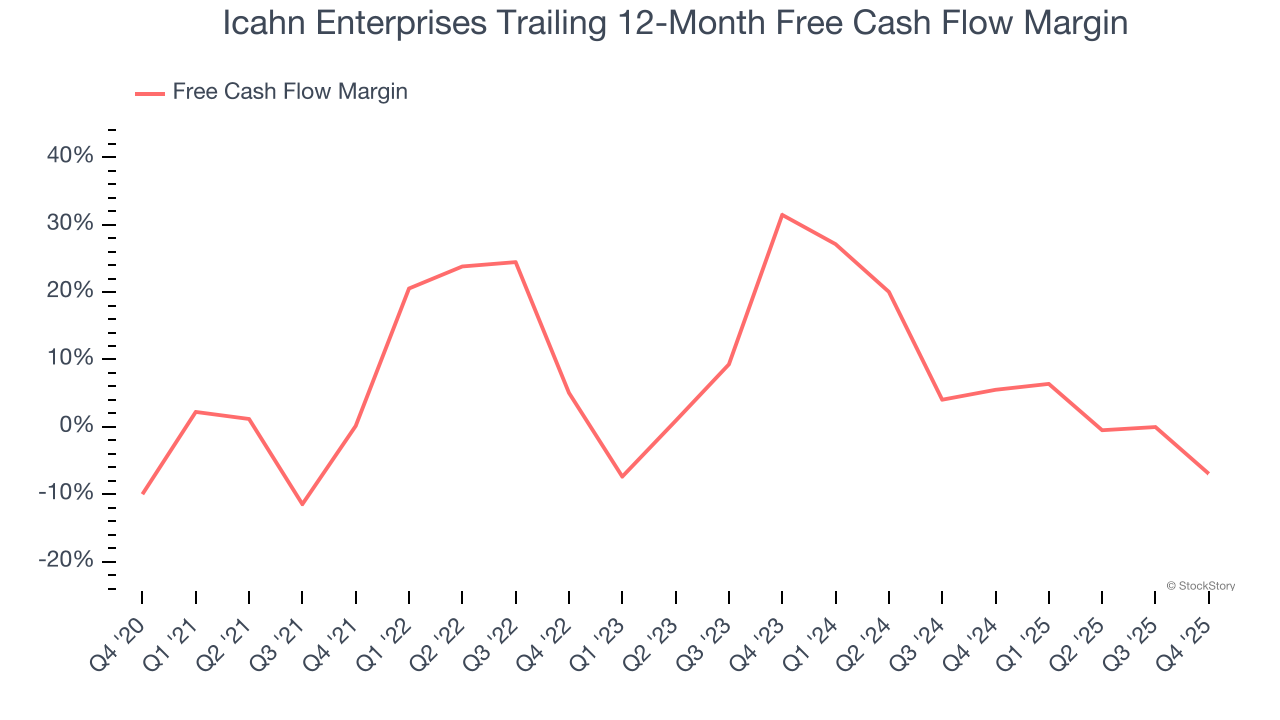

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Icahn Enterprises’s margin dropped by 7.1 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Icahn Enterprises’s free cash flow margin for the trailing 12 months was negative 7%.

Final Judgment

Icahn Enterprises isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at $7.54 per share (or a forward price-to-sales ratio of 0.5×). The market typically values companies like Icahn Enterprises based on their anticipated profits for the next 12 months, but there aren’t enough published estimates to arrive at a reliable number. You should avoid this stock for now - better opportunities lie elsewhere. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

Stocks We Would Buy Instead of Icahn Enterprises

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

/Super%20Micro%20Computer%20Inc%20logo%20on%20building-by%20Poetra_RH%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_logo%20and%20website-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)